ABSTRACT

We aim to analyze the perception of Brazilian auditors regarding differences in career development for women and black people. Methodologically, we conducted a web survey totaling 329 answers from professionals with diverse profiles regarding the length of service, job position, age, sex, and race. The results show that even men perceive the career as being harder for women. An important finding is that the main difficulties are found in medium and small-sized auditing companies. We contribute to the literature on three fronts: (i) by expanding the theme to cover medium and small-sized companies; (ii) by bringing to the Brazilian scenario the discussion on the perception of differences in the careers of external auditing professionals; and (iii) by contrasting perceptions about the career and the environment for professionals from diverse groups in terms of sex and race. As a practical implication, we conclude that if there is an interest in turning audit into a more just and equitable profession, much has to be changed in auditing careers, even in companies situated to the South of the Equator, so that the sins from elsewhere would not be the same here, sins that were imposed by a colonial conceptualisation of gender and race.

1. Introduction

In the Brazilian scenario, women represent more than half of the students in undergraduate accounting courses (Nganga, Gouveia, and Casa Nova Citation2018) and almost half of all registered accounting professionals in Brazil, reaching 42,81% in June 2021 (CFC Citation2022). Despite the growing representation and inclusivity, women still face multiple barriers, remaining underrepresented in managerial roles in Brazilian society and worldwide (Cohen et al. Citation2020; Lima et al. Citation2021).

Traditionally dominated by white men, audit firms worldwide have been developing and adopting policies to become more inclusive workplaces. However, previous research shows that there are still large differences between the career paths for different social groups (see Anderson-Gough et al. Citation2022; Egan and Voss Citation2023; Lima et al. Citation2021). Considering Western countries, previous research questions whether audit firms are truly changing the inequality regime or just using it to constitute a business case (Egan and Voss Citation2023). Furthermore, there is evidence that some of the developed policies reinforce some gender barriers and stereotypes (Edgley, Sharma, and Anderson-Gough Citation2016; Kornberger, Carter, and Ross-Smith Citation2010), therefore reproducing the inequality regime instead of challenging it.

Overall, the existing literature points to the gender-based pay gap (Ittonen and Peni Citation2012), different types of violence suffered by women (Bitbol-Saba and Dambrin Citation2019; Tremblay, Gendron, and Malsch Citation2016), and the barriers to women’s career progression (Castro Citation2012; Kokot-Blamey Citation2021; Lupu Citation2012). A common trait of most of the research in this area is the focus on the Big Four firms due to their market representativity. In this sense, non-Big Four firms and their practices represent a research gap. Additionally, we highlight that this kind of mapping has not yet been conducted comprehensively in Brazil, a post-colonial context marked by multiple structural inequalities (Lima et al. Citation2022). Thus, we question whether there is no sin to the South of the Equator.

The presence of a significant number of registered auditing firms beyond the Big Four marks the Brazilian audit context. According to the Brazilian Securities and Exchange Commission (Comissão de Valores Mobiliários), 341 registered auditing companies are allowed to audit publicly traded companies (CVM Citation2018). Therefore, we observe that many medium and small companies remain under-researched, representing an empirical and theoretical gap that we aim to address in this work.

In addition to the significant number of non-big Four companies, Brazil is an interesting case in which to analyze diversity policies because of its social and historical constitution. Since the colonisation, Brazil has been marked by sexism and racism established by Eurocentric thinking that divides people into two groups: people whose lives are worthy and are considered humans and those considered unworthy of living, seen as disqualified, indecent, non-human (Lima et al. Citation2022; Oliveira Citation2018). In this context, black and indigenous people were enslaved and exploited for centuries (Silva, Vasconcelos and Lira Citation2021) and remain marginalised until the current day.

Given this historical context, the Brazilian case proves interesting due to Latin American racism and its sophistication that keeps black and indigenous people in a subordinate condition (Gonzalez, Citation1984), in addition to the low representativeness of black people in socially privileged places – which refutes the widely accepted myth of racial democracy (Silva, Nova, and Carter Citation2016). We also highlight the Iberian heritage of a rigid hierarchy associated with a process of social classification that privileges men over women and whites over blacks (Gonzalez Citation2020). In this context, Brazilian society's constitution regarding the socio-sexual and racial division of labour (Hirata Citation2004, Citation2010; Saffioti Citation1976) – and, therefore, the women's role – differs from Western countries.Footnote1

Regarding sexism, Brazil remains one of the most violent countries. Data shows that violence against women (called feminicide and characterised by Law) is high and keeps growing. It is perpetrated mainly by men who live or have lived with the victims (8 in every 10 cases) and estimates accounting that nearly 10% are reported. According to a report by the Public Security Forum, in the first half of 2022, 699 women were victims of femicide, i.e. an average of four women were killed every day. The report also points out that this figure is 3.2 percent higher than the total number of deaths recorded in the same period last year, when 677 women were murdered.

Alongside sexism and patriarchy, the country is still the heir of a colonial past where women's bodies were objects of exploitation. This is even reinforced in the case of black women who were enslaved. This is why Lelia Gonzalez, one of the most recognised Brazilian Black feminist theorists, said that were only three positions that a black woman could occupy in the Brazilian social imaginary: mucama, ama de leite and mulata (Gonzalez Citation1984), someone who has the body put at service, being in the domestic chores (mucama), in nurturing and caring for children (ama de leite) or for pleasure (mulata).

These intricacies and complexities of the identity avenues conformed by gender, race and social class, among other social markers, later were consolidated as the intersectionality as proposed by Crenshaw (Citation2002). In the case of Brazil, the colonial past reinforces internally and externally an image of second-class humanity that still haunts us. Instead of being a paradise, created and exported as a racial democracy, it daily confirms that the sins below the Equator are even greater or more numerous. For Lélia Gonzalez (Citation1984, p. 228),

Like any myth, that of racial democracy hides something beyond what it shows. At first glance, we realize that it exerts its symbolic violence, particularly on black women. Because the other side of the carnivalesque deification [mulata] occurs in this woman's daily life, when she is transformed into a domestic servant [mucama or ama de leite].

Considering the above, we aim to analyze the perception of Brazilian auditors regarding differences in career development for women and black people. We conducted a survey with Brazilian audit firms of different sizes. The research sample is based on 329 respondents, of which 196 work in Big Four firms and 133 in non-big four firms. Our results reinforce the findings of the existing literature conducted in Western countries, which may indicate that diversity policies designed and adopted by audit firms disregard local context and particularities. Regarding the respondents’ perceptions, we highlight that gender-based differences are so blatant that even men perceive the career as being harder for women. Lastly, our data indicate that medium and small audit firms are perceived as the firms with the main difficulties for non-hegemonic groups to construct their careers. We conclude that Big Four firms have the advantage of acting as globalised companies that (re)produce standardised diversity practices and policies, while medium and small firms have more difficulty developing and implementing diversity policies and actions.

We hope this research contributes to the literature on three fronts: (i) by expanding the theme to cover medium and small-sized companies; (ii) by bringing to the Brazilian scenario the discussion on the perception of differences in the careers of external auditing professionals; and (iii) by contrasting perceptions about the career and the environment for professionals from diverse groups in terms of sex and race/ethnicity. As a practical implication, we conclude that if there is an interest in turning audit into a more just and equitable profession, much has to be changed in auditing careers, even in companies situated to the South of the Equator, so that the sins from elsewhere would not be the same here, sins that were imposed by a conceptualization of races and difference, built based on the colonialism.

2. Literature Review

The sexual and racial division of labour is a key discussion when addressing gendered and racialized dynamics. Previous research claims that the difference between men and women exists due to the physical (biological) differences, while other researchers discard that deterministic, biologistic view and affirm that this division has been historically and socially constructed (Lehman Citation1992). Based on the different social roles, men and women exercise different tasks and occupy different social places (Haynes Citation2017; Lehman Citation1992). In this paper, we adopt the understanding of ‘gender’ as something not determined in biology but rather in a structure of arbitrary designation of positions in a relational field’ (Segato Citation2018, 24). In sum, the socially constructed differences between men and women relate to the understanding of what it means ‘to be a man/woman’ (Haynes Citation2017) and is the founding belief of sexism, that is, the social structure that argues men are superior to women and should be responsible for making decisions (hooks Citation2018).

From a racial perspective, the labour division ‘is a fundamental category for analysing structural racism in the labour market’ (Alves Citation2022, 213). In this paper, we consider that race ‘refers to a group of people socially defined on the basis of physical characteristics. Race is ‘made’ through a socially creative process’ (Annisette Citation2020, 532). In sum, race and gender are social constructions that deeply influence our social lives, positioning what is expected from people based on them.

Importantly, both race and gender influence ‘conditions of access and permanence in the job market’ (Kerner and Tavolari Citation2012, 57). In this sense, workplaces may lead women to feel that their femininity is inferior to masculinity, mainly due to the privileges that men hold over them (Carmona and Ezzamel Citation2016). In terms of race, Ahmed (Citation2012, 4) argues that organisations, in general, (re)produce whiteness and racism in their everyday practices, making non-white people recognise themselves as strangers and diversity tokens. ‘Whiteness can be a situation we have or are in; when we can name that situation (and even make jokes about it) we recognise each other as strangers to the institution […] We also want there to be more than one; we want not to be the one. Becoming the race person means you are the one who is turned to when race turns up. The very fact of your existence can allow others not to turn up’.

Importantly, racism and sexism have their individual effects but also intersect, producing a matrix of domination (Cho, Crenshaw, and McCall Citation2013) and providing different accounts challenging ‘woman’ as a universal analytical category. To provide an intersectional look into diversity in the auditing profession, we must recognise ‘the ways in which racism, sexism, and other inequalities work in tandem to corrode everyone’ (Silva Citation2016, 41). This is especially true for the Brazilian scenario, given the historical and social constitution (Gonzalez Citation2020). Adopting a feminist theoretical perspective, we argue that audit firms, despite developing and adopting diversity policies, still (re)produce gendered and racialized workplace dynamics, raising the need to adopt an intersectional approach for a deeper understanding of the issue.

2.1. Entrance of Women into the Accounting Professional Market

The accounting profession is considered gendered not only because it is a male-dominated field but also because of its values, practices, and beliefs (Haynes Citation2017). To analyze the accounting – and auditing – profession as gendered is necessary to understand its history as ‘to conceive the issue of gender [and race] is one of the most complex tasks, and to think about it historically’ (Segato Citation2018, 20). Accordingly, in this section, we present some historical facts that illustrate some of the accounting profession's gendered practices and values that are sometimes presented subtly.

Lehman (Citation1992) accounts for the ‘herstory’ of women entering the accounting profession. The historical account demonstrates how subtle sexism can sometimes be – when, for example, the Institute of Chartered Accountants (ICA) declared that it supported the entrance of women into the accounting profession but denied them the possibility of achieving adequate professional qualifications. Moreover, there is evidence of how different social labels impacted this process. In 1911, the associations that collectively represented the accounting class in the United Kingdom discussed the matter. In this first debate, gender was considered alongside class – therefore, from an intersectional perspective – and the argument was made that the entrance into regulated professions should only happen for the middle class and that since middle-class women did not need to work to secure the family's livelihood, the women who would enter would-be lower-class women, which was even less desired. After being put to vote, the motion was rejected by most members (Lehman Citation1992).

In the period between 1920 and 1980, Lehman (Citation1992) highlights the resistance of businessmen in hiring women, the difficulty of obtaining certifications due to the lack of experience, and the impossibility of working outside of offices as a Certified Public Accountant (CPA). In the period between 1940 and 1960, the low representation of women in accounting jobs and the wage gaps were the main challenges to be overcome by women. We highlight, furthermore, that women were still occupying lower positions and that even when they had higher qualifications, they still received lower wages and faced various stereotypes that hindered their entrance into the career.

The historical account provided by Lehman (Citation1992) helps us understand the current scenario of Western countries. In the USA, the Association of International Certified Professional Accountants (AICPA, Citation2017) reports that only 23% of the associates in accounting companies are women. Regarding ethnicity, the report states that 95% of the associates are white, 2% are Asian, 2% are Latinos, 0.3% are black, and 0.7% belong to other ethnicities. These data illustrate the everlasting effects of racism and sexism in the accounting profession. In sum, the existing gendered and racialized accounting profession is the result of a historical and social construction.

2.2. The Audit Professional Path: Symbols, Practices, and Dynamics

The auditing profession presents a striking discourse on professional ascension being based purely on meritocracy and sells the idea of a ‘clear path to the top of the career’ with the possibility of becoming not only a manager but also a partner and leader in the company (Empson Citation2007; Lupu Citation2012). However, previous research indicates that this discourse is a way of disguising a male worldview, or as proposed by Lima, Casa Nova, and Vendramin (Citation2023): a me(n)ritocraci worldview. In this sense, there is extensive literature (see Egan and Voss Citation2023) signalling the barriers constructed in the audit firms to prevent professionals pertaining to non-hegemonic groups – like women, black people, and LGBTQIA + individuals – from reaching partnership and managerial positions.

A way of maintaining the ‘male, pale, stale’ image of the audit profession (Egan and Voss Citation2023) is using symbols to legitimize a specific profile as ‘the true auditor’. Carmona and Ezzamel (Citation2016) affirm that the construction of symbols and images representing certain professions may reinforce or deconstruct some gender barriers. As an example, the authors use the images of accountants on the Internet and assert that men are providers and rational decision-makers, while women are seen as their supporters. Similarly, Duff (Citation2011) analysed the pictures used by UK audit firms in their reports. The findings show that of the 654 pictures analysed, 81% showed a single white person, 6% showed a black person, 11% showed a mixture of black and white people, and 3% did not allow for the identification of the ethnicity of the people shown. In detailing these percentiles, Duff (Citation2011) shows that most pictures of black people are pictures in which white people are also present, while pictures of white people are mainly pictures of lone individuals or pictures of a group of white individuals. Lastly, most pictures of black professionals showed them dressed in more casual outfits and less professional environments. The findings of Duff (Citation2011) and Carmona and Ezzamel (Citation2016) illustrate how audit firms have been working symbolically to maintain the gendered and racialized dynamics of the audit profession.

A key issue discussed in the existing literature is maternity’s impact on women’s professional development and career progression. Haynes (Citation2008a, 344) argues that:

When women accountants are pregnant or in early motherhood, they stand outside the system of legitimation, outside the accounting habitus, as a different socio-political category. The two embodied identities and subjectivities of professional accountant and mother have the potential to clash. Pregnancy can be characterized as an unwelcome intrusion of the fertile body into the professional environment. The female body itself has been seen as the ‘other’ […] Pregnancy marks the cultural and physical undoing of the socialized identity of the accountant and the gender transformation into the identity of mother. Women may be subjected to subtle practices of power questioning their commitment, belonging, and immersion in the accounting context.

The construction of maternal bodies as abject and unwelcomed is part of a greater social structure (re)produced by audit firms: sexism. The existing sexism in audit firms shapes the careers and experiences of everyone involved in the profession. It differentiates maternity from paternity (Kokot Citation2015), establishes an ‘ideal worker’ figure (Castro Citation2012), and makes auditors from non-hegemonic groups aim for greater performances as a way of compensating for being unwelcomed, strange, and unfit to the male, pale stale image of the profession (Egan and Voss Citation2023; Lima et al. Citation2021)

Another strand of research that helps explain women's scarcity in audit firms is understanding the violent and hostile workplace (Lima et al. Citation2021). Bitbol-Saba and Dambrin (Citation2019) illustrate how the audit-client relationship relies on the sexualization and instrumentalization of women’s bodies, reinforcing stereotypes, masculinity, and sexism. Based on their findings, the authors propose that the relationship between auditor and client should also be under the scope of sexual harassment as a way of holding these social actors accountable for their contribution to the sexist culture of the audit profession.

Considering this scenario, audit firms have been developing and adopting diversity policies. However, previous research questions whether these firms are truly adopting diversity policies or simply capitalising on their rhetoric. Kornberger, Carter, and Ross-Smith (Citation2010) show that even though the practices of flexibilization of work hours aim to overcome the barriers found in women's paths to parenthood, they, in truth, reinforce those barriers because the women who adopted the flexibilization of work hours were seen as not committed enough to their jobs.

Edgley, Sharma, and Anderson-Gough (Citation2016) concluded that despite these companies divulging their diversity practices, they break very little with the power structures because these practices are seen as financial strategies, therefore being tied to the commercial aspect. The authors highlight the importance of the Big Four adopting diversity practices because these companies have enough representativity to shape and change the image and the profile that is expected of auditing professionals, mainly via the companies’ selection processes. Finally, the authors highlight that these companies have historically preferred homogeneity in their professionals’ profiles, with factors such as the ability to ‘fit in’, to work many hours, and ethical commitment to their clients being determinant factors for success.

In sum, based on Kornberger, Carter, and Ross-Smith (Citation2010) and Edgley, Sharma, and Anderson-Gough (Citation2016) studies, we sustain that companies are using diversity policies as business cases instruments and not challenging the social injustice that (re)produces the gendered and racialized dynamics. Aligned with this argument, previous research indicates that firms with more women among their personnel receive higher fees (Ittonen and Peni Citation2012) and provide audit services with higher quality (Cameran, Ditillo, and Pettinicchio Citation2018), providing meaningful justifications for audit firms to use diversity policies as business cases. Therefore, policies of inclusion seem to pertain more to economic and commercial interests than to social interests or the promotion of organisational justice and equity of opportunities (Edgley, Sharma, and Anderson-Gough Citation2016; Kornberger, Carter, and Ross-Smith Citation2010). In this manner, ‘accounting firms have therefore embraced diversity agenda but still presents challenges in implementation’ (Paisey et al. Citation2020, 70).

2.3. The Brazilian Scenario

The historical account Lehman (Citation1992) provided illustrates the gendered accounting professional constitution for Western countries. Despite the Brazilian scenario not having an extensive historical mapping similar to Lehman (Citation1992), there is some evidence regarding the gendered/sexist practices (Casa Nova Citation2022; Lima, Casa Nova, and Vendramin Citation2023).

According to the Federal Council of Accounting ([Conselho Federal de ContabilidadeFootnote2] CFC, Citation2022), there are 527,404 accounting professionals registered in the CFC, of which 42.8% are women and 57.2% are men. There is no information on the distribution of professionals according to race/ethnicity. Data from the Brazilian Auditors Institute (Ibracon Citation2017) accounts for 1441 associates, 931 of which are auditors. The report also registers 117 auditing firms associated with the Institute. The report has no information on the distribution of associates by gender or race/ethnicity.

Specifically, in the audit context, data from PwC shows that in 2015, only 10% of the partners were female, while 54% of the associates were women. Compared to data from 2020, there are some advances regarding women’s presence at the top of the audit career (directors and partners), but it is clear that there is a gender pipeline. The data relative to the participation of women in the hierarchical levels of PwC Brazil are presented in .

Table 1. Participation of women in the hierarchical levels of PwC Brasil.

In terms of race, black people in Brazil remain underrepresented despite being the numerical majority in the Brazilian population (Silva, Nova, and Carter Citation2016). In Brazilian accounting, Silva (Citation2016) asserts that the accounting discourse denies black women their professional identity as licensed professionals through three kinds of discrimination: for being women, for being black and, in numerous cases, for being a black woman; in other words, for the intersection of prejudices relative to gender, race, and social stratum. Regarding the audit accounting and audit context, the silence about racism and racialized practices/exclusion still persists (Annisette Citation2003): there is no official data neither from the audit firms or the accounting regulatory bodies.

Lopes and Lima (Citation2022) use the per capita income to materialise and account for the intersectional differences in the Brazilian context. The data used by the authors demonstrate that the difference between the incomes of the white and black populations is about 45%. Comparing the income of men and women, the difference is about 7.40%. Lastly, observing the intersectional difference between white men and black women is about 103.2%. In conclusion, the Brazilian context provides a meaningful site to discuss diversity and inclusion policies because of its structural oppressions.

3. Methodological Trajectory

To analyze the perception of Brazilian auditors about their professional paths, we have adopted a quantitative approach, using a survey questionnaire as the research instrument for data collection. Paradigmatically, we position the paper into the critical accounting realm (Gendron Citation2018; Richardson Citation2015) as we deal with issues related to power dynamics – mainly gender and racial discrimination.

3.1. Research Strategy and Data Collection

Our methodological strategy was conducting a web survey. We chose this strategy because of its advantages and possibilities, mainly because it enables access to individual Brazilian auditors’ perceptions and guarantees their anonymity. Conducting web surveys does have some negative points, such as the self-selection bias of the respondents (Smith Citation2022). To mitigate that risk, we contacted the research participants via LinkedIn, therefore ensuring their professional role as auditors. We note that in Brazilian accounting research, previous studies have adopted a similar strategy (Marcos, Vogt, and Cunha Citation2017), highlighting the potential to increase the sample size. We manually searched LinkedIn using the audit firms’ names to map the possible respondents, that is, based on the person’s affiliation to an audit firm they were invited to engage with the questionnaire. During this phase, we targeted a large and diverse audience to guarantee perceptions from different profiles.

After this initial mapping, we utilised the LimeSurvey platform for data collection, sending an invitation to the research to the contacts collected from LinkedIn. To ensure respondents could only answer the survey once, we created exclusive access codes to each email sent. The data collection process followed the Total Design Method (Dillman Citation2007). Overall, 1,156 emails were sent, and 329 valid questionnaire answers were received, totaling a response rate of 28.46%.

3.2. Research Instrument and Analysis Procedures

The questionnaire used in this research was developed specifically for this study. The main source for developing this instrument was the existing literature, which was complemented by informal conversations with auditing professionals regarding the theme. To validate the instrument, the questionnaire was sent to auditors, both former and currently in service, so that they could analyze and comment on whether any new questions could be added and whether the questionnaire resonated with their experiences.

The questionnaire is structured into four sections. The first section includes questions about the respondent's personal, educational, and familial profiles. The second one deals with aspects of their career and professions. The third section contains questions related to the quality of life and turnover. The fourth section focuses on their perception of the auditing career (e.g. career planning, gendered dynamics, diversity policies, etc.). The third and fourth sections were composed of affirmations that must be answered with an indication of (dis)agreement on a Likert five-point scale. At the end of the questionnaire, there was an optional space for additional considerations by the respondents, some of which are presented in our analysis of the results aiming to complement the analysis of the quantitative data.

For the quantitative analysis, we conducted Mann–Whitney and Kruskal–Wallis non-parametric statistical tests to compare a dependent variable, measured on at least an ordinal level, based on stratification for different groups. In this research, the groupings were related to gender, race, and hierarchical position at the individual level, and for the firms, we divided them into (i) Big Four companies (PwC, KPMG, EY, Deloitte); (ii) large and medium-sized auditing companies which are not Big Four (BDO, Grant Thornton, RSM, Baker Tilly, Mazars, Moore Stephens); and (iii) other companies, mainly small ones. For the qualitative analysis, we conducted a content analysis on all the comments written at the end of the questionnaire to complement the quantitative results.

3.3. Research Sample

Our sample consists of 329 valid questionnaires. We present our sample demographic characteristics in . The sample mainly consists of male professionals from the Southeast region. The number of females respondents being close to the males respondents is due to the researchers’ efforts to ensure expressive contact with women who work in the area.

Table 2. Respondents demographics.

Noteworthy, according to the Census conducted by Instituto Brasileiro de Geografia e Estatística [IBGE – Brazilian Geography and Statistics Institute], the Brazilian population in 2022 was composed of 43,5% white, 45,3% Mixed-race of black and white descent, 10,2% black, 0.6% Asians, and 0.4% Indigenous. In this sense, our sample illustrates the whiteness of audit firms and their racialized bias.

We present the respondents’ education characteristics in . We notice a predominance of accounting as the major undergraduate degree (almost 85%), complemented by an MBA course (65,3%). The Brazilian regulatory context can explain the predominance of accounting undergraduates. The Conselho Federal de Contabilidade demands an undergraduate degree in accounting before applying for a professional license. For the MBA, a possible explanation is the CFC demands of continued education programmes.

Table 3. Academic training of respondents.

Overall, the profile of the average respondents is male (53.2%), white (72%), between 21 and 30 years old (74.2%), holding an accounting undergraduate degree and an MBA related to either accounting or finance.

4. Empirical Findings

4.1. Hierarchical Profile: Who is at the Top of the Career?

As previously discussed, audit firms claim to have a ‘clear path to the top of the career’ that has been challenged by previous research (e.g. Lupu Citation2012). To analyze this matter in the Brazilian context, we asked our respondents to answer some questions to characterise their hierarchical level and experience. Initially, we asked how long the participants had been working as external auditors and what kind of company they currently worked for ().

Table 4. Professional experience and which kind of company they work for.

As observed in , there is a predominance of auditors with up to 10 years of a career (85.4%). This fact is explained in the literature by the high staff turnover rate due to factors related mainly to the low quality of life experienced by auditing (Hermanson et al. Citation2016) and the ‘up or out’ culture (Lupu and Empson Citation2015). Regarding which kind of company, the respondents work for, almost 60% of them work for Big Four companies, which is explained by their high market representativity.

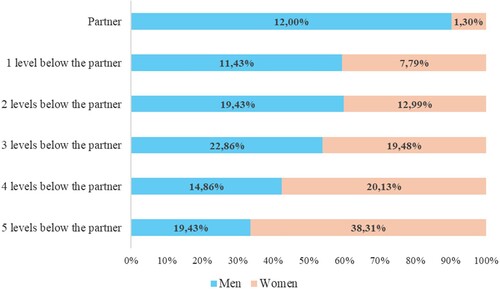

Regarding the analysis of the hierarchical configuration, we asked participants about their hierarchical position in the company. Despite being a very heterogeneous career path, each company adopts different names for the hierarchical positions. To ensure our questionnaire could adequately reflect the career planning for all the firms, we questioned the respondents about the distance, in hierarchical levels, between their current position and the partner (Graph 1).

Graph 1. Gendered hierarchical positionings. Source: Research data.

As presented in Graph 1, women represent most respondents in lower levels (4, 5, or more hierarchical levels below their partner), while men represent the majority of respondents who are or are close to being partners. To test the significance of these results, we adopted the Chi-square test, which had a level of significance of 1% (p-value <0.01). Accordingly, we can affirm that there are significant differences in the proportion of men and women in the different hierarchical levels of the career, corroborating the studies of Lupu (Citation2012), Kokot (Citation2015), and Cruz et al. (Citation2018) and showing that women still do not occupy the higher positions in the hierarchy of auditing firms.

Some respondents – with different personal and professional backgrounds – provided personal accounts at the end of the questionnaire that shed some light on the matter and help us understand this reality. Overall, the comments highlight maternity as an important matter, reinforcing the existing literature (Haynes Citation2008a, Citation2008b; Kokot Citation2014, Citation2015) and the unequal impact of maternity and paternity.

The job market, in general, is more complicated for women because of maternity, and it would not be different in auditing. Many [female] colleagues chose to quit auditing due to the excessive work hours and badly planned trips. Because of this, we see more men in higher positions than women. (Female auditor, white, non-Big Four large company, 3–5 years of experience)

Auditing firms are still sexist and still believe that men are more practical and don't have any deterrents like marriage or children hindering their career development. (Female auditor, white, non-Big Four large company, more than 10 years of experience)

Professional growth in the Big Four is accelerated, and for that, there's also a high demand. Internally, it is said that what an employee of other companies takes three years to learn, a Big Four employee learns in one. It's no coincidence that we work from Sunday to Sunday with no start or finish times, and often there's no recognition of that and it ends up becoming an obligation. A week ago, I was fired, just returning from my maternity leave. In the Big Four, there's no space for social life. (Female auditor, white, Big Four, 5–10 years of experience).

Based on , we notice that white and black men are represented in all career levels and only Asian men stopped 2 levels below the partner. For women, the scenario is the other way around: only Asian women are represented at the partner level, and black women rank the lowest in the hierarchical pyramid, reaching only 3 levels below the partner. In this sense, we sustain that the career progression in Brazilian audit firms is not only gendered but also racialized, having a deeper impact on black women’s professional development and advancement.

Table 5. Intersectional hierarchical position.

4.2. Is Auditing a Men’s World?

The second part of our questionnaire had questions regarding career plans, feeling valued, and the (dis)balance between family and professional life. With these questions, we aimed to analyze how respondents perceive their career planning and some dynamics related to the sexual division of labour.

Based on the data presented in , we notice that the affirmation with the highest degree of agreement is related to the pressures in the sense of constantly proving their professional value and competency. Previous literature (see Lima et al. Citation2021) argues that the pressure is felt deeper by non-hegemonic professionals as they are socially constructed as the other, always feeling they have to perform better than their peers as a way of being legitimised and included. The affirmations with the highest disagreement were the ones relating to current plans of changing careers due to maternity/paternity and those about conciliating personal and professional lives. This challenges the promise of a ‘clear path to the top’ advertised by audit firms (Empson Citation2007), especially when taking into account maternity/paternity.

Table 6. Frequency distribution of the questions.

To analyze if social groups feel these questions differently, we conducted the Chi-square test to the answers to the questions above. In addition to possible differences between the sexes, we also tested whether the pressures felt were related to career stages and race, as shown in .

Table 7. Career planning and advancement.

Furthermore, we observed that the questions about career planning and the ones about changing careers to dedicate themselves to maternity/paternity presented statistically significant differences. This result corroborates that of Kokot (Citation2015), in which women perceive that it is expected of them to choose between familial and professional life while men do not feel that pressure, reinforcing the idea that women are responsible for caring for the family while men's role is to provide for the family; in other words, a very traditional perception regarding the social roles of men and women. In this sense, Brazilian audit firms (re)produce the sexual division of labour.

Regarding the hierarchical level, we noticed that there is a statistically significant difference for most of the questions, showing that most of the factors listed, especially those related to the balance between personal and professional life, are related to the hierarchical position of the respondent. Lastly, regarding race, we observe significant differences in the questions about career planning and work-life balance. Furthermore, the difference may result from the socialisation process, naturalisation of the pressure, and ‘up or out’ culture (Lupu and Empson Citation2015).

The different perceptions between white and black people may be explained because of the low representation of black people in higher hierarchical positions. The issue of low representativity can be faced with a message or sign that black people do not reach such positions, thus influencing the perception of black people at other hierarchical levels. As a result of the underrepresentation of black people, thus, they may feel that they will not reach top positions since they’re not the ‘partner type/ideal worker’ (Reid, Citation2015), they are made strangers in the organisation (Ahmed Citation2012).

4.3. Harassment and Discrimination

To maintain the sexism and racism in place, the hegemonic group tends to use violence as a way to (re)produce these oppression systems (hooks Citation2018), especially to reproduce the conqueror ideal established by masculinity and whiteness (Segato Citation2018). Adding to the previous research that documented gendered-based violence in the audit profession (Bitbol-Saba and Dambrin Citation2019), the Brazilian setting is one of the most violent countries towards women and black people (Lima et al. Citation2022). For these reasons, we asked the participants about their experiences and their perceptions of harassment and discrimination.

Building on Bitbol-Saba and Dambrin’s (Citation2019) result, we expand the view on harrassment to include auditor-client interactions. In this case, our data shows that only about a quarter (26%) of our respondents have suffered some case of harassment, while more than half of the respondents (57%) are aware of someone who has suffered either sexual or moral harassment from a client. Regarding the relationship with the supervisor, 34% of the respondents argue that they have suffered some case of harassment, and 59% of the respondents are aware of harassment cases. In this context, harassment may be related to the hierarchical/power structure within auditing companies. Lastly, less than half of the respondents have suffered or are aware of some harassment cases between colleagues, reinforcing the idea that harassment is used as a power strategy to maintain the hierarchy .

Table 8. Frequency distribution of the questions about harassment.

In agreement with Segato (Citation2018), we maintain that harassment is more than violence. It is a communication device to reaffirm a social group's dominance, to communicate and teach society about their power, value, prestige, and territorialisation. In this sense, ‘violence is the cement that keeps the edifice of asymmetries standing, the atmosphere in which we have learned to live’ (Segato Citation2018, 61).

To look further into the differences in the questions about harassment, we applied the Chi-square test, separating answers by sex, type of company, hierarchical level and race, as shown in . Our findings show that when separating the respondents according to sex, all three questions about having suffered harassment present statistical significance, corroborating the idea that harassment is a gendered dynamic. On the type of firm, none of the questions showed statistical significance. Regarding the hierarchy, though, the question about suffering harassment from clients presented high statistical significance, which may be explained as a result of the sexualization processes of women’s bodies (Bitbol-Saba and Dambrin Citation2019). Considering that the lower women are placed in the hierarchy, the higher the danger of being harassed by clients is another factor in the sexist structure of audit firms and helps us to understand the construction of women scarcity (Dambrin and Lambert Citation2008).

Table 9. Harassment stratification.

Furthermore, considering the racial democracy myth, displays the perception of discrimination and the statistical testing to see whether there are significant differences based on the respondent’s race. Overall, we observe that most of the participants stated that they had not suffered any kind of discrimination, which resulted in no difference regarding race. However, it is possible that the participants may have suffered from discriminatory practices but are not aware of that since discrimination happens in subtle ways.

Table 10. Discrimination perceptions.

4.4. Wage Gaps, Career Differences, and Retention Policies

The last section of our questionnaire focused on understanding the wage gap, the overall perception of the career, and the retention policies adopted by the firms.

Considering sexist violence as an enunciation act (Segato Citation2018), we sustain the wage gap as an economic gendered violence that communicates to women that they are not as valuable as men in the profession. In addition to the wage gap, we analyze an overall perception of the career: Is the auditing career harder for women? Specifically, the Likert scale was changed to seven points for these questions. The closer a respondent's answer is to 1, the more they believe that men have higher wages/the career is harder for men; close to 4, they believe there is no wage gap/the career is equally difficult for both sexes; and the closest to 7, they believe women have higher wages/the career is harder for women.

Based on , we note that over 90% of the men believe that there is no wage gap. Women believe a wage gap benefits men (30,2%), and only a small portion of men acknowledge the wage gap (8%). The average grade found for the wage gap issue was 3.6, leaning towards men having higher salaries. The average grade for the issue of difficulty in the career was 5.7, representing a perception of a higher difficulty for women. We found that the smaller the company, the greater the perception regarding wage gaps. The average grade decreased from 3.77 in Big Four companies to 3.21 in small auditing companies. Regarding hierarchy, the average for those in the higher career levels was 3.71, while for the lower career levels, it was 3.54. Lastly, similar to our results, Brighenti, Jacomossi, and da Silva (Citation2015) demonstrate that, overall, although women have similar or higher levels of education than men, their average pay is still lower, indicating an endemic situation of wage gap.

Table 11. Wage gap and career perception by sex.

From the statistical testing, we notice that this perception varies according to the respondent’s sex, the kind of company they work for, and their hierarchical level within that company. In this sense, we see that women are aware of that message and economic violence, while men are not – or are in denial. Regarding the difference between Big Four Firms and smaller-than-Big-Four-Firms, we argue that given the magnitude of the firms, the wage gap within Big Four Firms sometimes can be disguised among variable pay arrangements, while on the smaller firms, there is a higher proximity between the auditors that can find out each other’s payment and see the gap.

When questioned whether the auditing career is harder for women or men, regardless of gender, respondents recognised it as being harder for women. However, women showed a higher degree of agreement, resulting in a statistically significant difference. Lastly, adding all the discussion, the following statements help us to understand better the structural differences between men and women in audit firms.

There are no wage gaps, but men are more well-regarded in the auditing career. (Female auditor, white, non-Big Four large companies, over 10 years of experience)

I don't think there is a wage gap; what happens is that it's easier for a man to reach the position of a partner than it is for a woman. Auditing is a very sexist area, and because of that, the pressure on women ends up being higher because they need to adapt to a different treatment […] Anyway, there are many factors behind that issue of difference between men and women in the auditing area, and it begins up high, with the partner. (Female auditor, white, non-Big Four large company, 1–3 years of experience)

Questioned on the existence of policies to support women’s retention in the organisation, around 51% answered that these policies exist in the company where they work. However, it is important to note that 86.2% of the Big Four respondents indicated the existence of such policies, versus 9.6% of those from non-Big Four large companies and 17.2% of those from small auditing companies. In other words, these policies are largely restricted to Big Four companies. From these results, we analysed the perception of those who said the policy exists in their company regarding its effectiveness (), and the perception of the need for such a policy for those whose companies do not have any such policies ().

Table 12. Analysis of the effectiveness of retention policies.

Table 13. Analysis of the need for retention policies for companies which do not have any.

As observed in , women perceive the effectivity of such policies as higher and believe that their colleagues also see the effectivity of these policies. Male respondents, however, in addition to not seeing these policies as effective, believe that their colleagues, both male and female, also do not see effectivity in these policies’ results. In the statistical analysis, we identified a statistically significant difference between the sexes for the second and third questions (p-value <0.10). To get a deeper understanding of this scenario, we present some statements from the respondents.

Even [though I am] aware that there is a sexist culture behind the career, on which is based the belief that the career is more adequate for men – which can be observed in how there are more male partners than female partners in the organization – I don't believe that women retention policies would be useful in changing this culture. In the organization where I work, I haven't seen any dismissals or promotions that were biased by the sex of the professional. During the time in which I was in the company, I only saw one case in which the professional was fired. Usually, the professionals themselves placed their resignation (Female auditor, white, non-Big Four large company, over 10 years of experience)

[t]he main strategy of power is opacity and concealment, and the codes and agreements between those who share its privileges lack transparency, cannot be seen, verified and much less ‘ethnographed’. The way in which power pacts and decides is inaccessible to those outside its narrow circle. (Segato Citation2018, 68)

It is very important to highlight that the internal culture of each company is different, so even among the Big Four, there are those that are more inclusive and even have programs aimed at encouraging women to take up leadership roles, and there are [firms] which aren't inclusive in the least. (Male auditor, Big Four, over 3 years of experience)

Upon analyzing the perception of the professionals from companies which do not have such policies, as shown in , men are indifferent to the creation of such policies, while women believe them to be necessary but notice that their male colleagues are indifferent to the creation of these policies. Given the Chi-square test, we found statistically significant differences between the sexes, on a level of 5% (p-value < 0.05) for the first question and 1% (p-value < 0.01) for the second. Based on these results, we argue that men are not fully aware of the retention policies’ importance and effectiveness, yet they remain in managerial roles designing and applying the policies firms adopt. Consequently, the lack of women in managerial positions is a gendered and gendering issue.

5. Final Remarks

Given the importance of diversity for society, audit firms – whether based on social justice or business case – have been developing and adopting diversity policies to include non-hegemonic groups. Despite being a well-established topic of interest in Western countries, Latin-American experiences remain silenced. Furthermore, the existing literature tends to focus heavily on Big Four Firms. Based on this scenario, we analysed the perception of Brazilian auditors regarding differences in career development for women and black people.

Theoretically, we engaged with the previous literature to provide an account of the Brazilian case and drew upon feminist theory concepts – such as gender, race, and the sexual division of labor – to grasp an understanding of how gendered and racialized dynamics influence the Big Four Firms and non-Big Four Firms. Methodologically, we conducted a web survey with a sample of 329 respondents. The questionnaire was written based on literature and on informal conversations with auditing professionals about the subject. We left a space in the questionnaire for optional considerations by the respondents as a way of allowing for reflections and reports of personal experiences regarding the theme. The data analysed showed that in the perception of men and women regarding aspects of the career, salary, and harassment; and finally, the proportion of men and women in the various hierarchical levels of the career. The respondents show the existence of differentiations that were indicated by women and, oftentimes, confirmed by men themselves. It is important to note that there was a smaller perception of gender differences mainly in the Big Four.

Our results confirm the main argument that the Brazilian social construction is still present in the daily professional life of an auditor. Therefore, they face the challenge of being at the crossroads of identity, where they are positioned by the social markers for which their professional paths are predefined. Brazilian female auditors face the triple discrimination of being women and, even more so, of being black women, of being subjected to sexist and racist violence and of ultimately being expelled from a career that is doomed to reproduce itself. Much needs to be changed so that the sins of other places are not the same as those South of the Equator. Many of them leave the career so that they can conciliate their profession with their maternity and family roles. They are mulatas having their bodies subjected to harrasment and discrimination. But they end being amas de leite and mucamas, leaving the profession to dedicate themselves to their families.

We hope our findings can add to the literature in three ways: (i) by expanding the theme to cover medium and small-sized companies; (ii) by bringing to the Brazilian scenario the discussion on the perception of differences in the careers of external auditing professionals; and (iii) by contrasting perceptions about the career and the environment for professionals from diverse groups in terms of sex and race. We sustain that studies naming and illustrating oppressive dynamics are important because ‘[w]ithout naming gender and without naming race, we will not be able to talk about the forms of differentiated treatment that reproduce inequality, nor will we be able, for example, to put into practice ‘positive discrimination’ as an instrument for leveling and repairing negative discrimination’ (Segato Citation2018, 61).

As for the limitations of this research, we highlight the fact that the survey was a web survey, with the possibility of comprehension problems regarding the questions, as well as possible lack or excess of motivation for the respondents. On the other hand, given the intensity of the daily work rhythm of these professionals, we suspect that other data collection strategies would have a very high chance of failing and not reaching the response level that we obtained. As a suggestion for future studies, this research could also be applied to internal auditors to evaluate whether there are differences between the two jobs. The qualitative study of perceptions, perspectives, and possibilities may also bring meaning to the numbers obtained here. Another interesting possibility is collecting the professional experiences of retired auditors.

Disclosure Statement

No potential conflict of interest was reported by the author(s).

Notes

1 In this paper, we understand Western countries in the same sense as Komori (Citation2008, p. 508) in which she stated that “[h]owever, existing research deals almost exclusively with the situation in the UK, the USA and Australia, where the accounting professions are well-entrenched and powerful and in all of which there are well-established feminist movements”.

2 The Federal Accounting Council [CFC] is responsible for guiding, regulating, and supervising the exercise of the accounting profession. Its tasks include: deciding on possible penalties for irregular exercise of the profession; regulating accounting principles, the Sufficiency Examination, the technical qualification register, and continuing education programs; and issuing Brazilian Accounting Standards of a technical and professional nature.

References

- Ahmed, S. 2012. On being included: racism and diversity in institutional life. Durham: Duke University Press.

- Alves, L.D. 2022. A divisão racial do trabalho como um ordenamento do racismo estrutural. Revista Katálysis 25, no. 2: 212–21. doi:10.1590/1982-0259.2022.e84641.

- Anderson-Gough, F., C. Edgley, K. Robson, and N. Sharma. 2022. Organizational responses to multiple logics: diversity, identity and the professional service firm. Accounting, Organizations and Society 103: 101336. doi:10.1016/j.aos.2022.101336.

- Annisette, M. 2003. The colour of accountancy: examining the salience of race in a professionalisation project. Accounting, Organizations and Society 28, no. 7-8: 639–74.

- Annisette, M. 2020. Race and ethnicity. In The routledge companion to accounting history. 2o ed, eds J.R. Edwards and S. Walker, 530–552. London: Routledge.

- Association of International Certified Professional Accountants [AICPA]. 2017. 2017 Trends in the supply of accounting graduates and the demand for public accounting recruits.

- Bitbol-Saba, N., and C. Dambrin. 2019. “It’s not often we get a visit from a beautiful woman!” The body in client-auditor interactions and the masculinity of accountancy. Critical Perspectives on Accounting 64: 102068.

- Brighenti, J., F. Jacomossi, and M.Z. da Silva. 2015. Desigualdades de gênero na atuação de contadores e auditores no mercado de trabalho catarinense. Enfoque: Reflexão Contábil 34, no. 2: 109–22.

- Cameran, M., A. Ditillo, and A. Pettinicchio. 2018. Audit team attributes matter: how diversity affects audit quality. European Accounting Review 27, no. 4: 595–621.

- Carmona, S., and M. Ezzamel. 2016. Accounting and lived experience in the gendered workplace. Accounting, Organizations and Society 49: 1–8.

- Casa Nova, S.P.C. 2022. “Ridin’ down the highway” - reflections on the trajectories of women professors in academia. Advances in Scientific and Applied Accounting. doi:10.14392/asaa.2022150202.

- Castro, M.R. 2012. Time demands and gender roles: the case of a big four firm in Mexico. Gender, Work & Organization 19, no. 5: 532–54.

- Cho, S., K.W. Crenshaw, and L. McCall. 2013. Toward a field of intersectionality studies: theory, applications, and praxis. Signs: Journal of Women in Culture and Society 38, no. 4: 785–810.

- Cohen, J.R., D.W. Dalton, L.L. Holder-Webb, and J.J. McMillan. 2020. An analysis of glass ceiling perceptions in the accounting profession. Journal of Business Ethics 164, no. 1: 17–38. doi:10.1007/s10551-018-4054-4.

- Comissão de Valores Mobiliários [CVM]. 2018. Cadastro Geral. Retrieved from: https://sistemas.cvm.gov.br/?CadGeral.

- Conselho Federal de Contabilidade [CFC]. 2022. Quantos somos: Profissionais da Contabilidade Ativos por Gênero e Região. Retrieved from: https://cfc.org.br/registro/quantos-somos-2/.

- Crenshaw, K. 2002. Documento para o encontro de especialistas em aspectos da discriminação racial relativos ao gênero. Revista Estudos Feministas 10, no. 1: 171–188. doi:10.1590/S0104-026X2002000100011.

- Cruz, N.G., G.H. Lima, S.O. Durso, and J.V.A. Cunha. 2018. Desigualdade de gênero em empresas de auditoria externa. Contabilidade, Gestão e Governança 21, no. 1: 142–159. doi:10.21714/1984-3925_2018v21n1a8.

- Dambrin, C., and C. Lambert. 2008. Mothering or auditing? The case of two Big four in France. Accounting, Auditing & Accountability Journal 21, no. 4: 474–506.

- Dillman, D.A. 2007. Mail and internet surveys: The tailored design method. John Wiley & Sons Inc.

- Duff, A. 2011. Big four accounting firms’ annual reviews: A photo analysis of gender and race portrayals. Critical Perspectives on Accounting 22, no. 1: 20–38.

- Edgley, C., N. Sharma, and F. Anderson-Gough. 2016. Diversity and professionalism in the Big four firms: expectation, celebration and weapon in the battle for talent. Critical Perspectives on Accounting 35: 13–34.

- Egan, M., and B. L Voss. 2023. Redressing the Big 4’s male, pale and stale image, through LGBTIQ+ ethical praxis. Critical Perspectives on Accounting 96. doi:10.1016/j.cpa.2022.102511.

- Empson, L. 2007. Professional service firms. In International encyclopedia of organization studies, eds S. Clegg and J.R. Bailey, 1315–1318. London: Sage.

- Gendron, Y. 2018. On the elusive nature of critical (accounting) research. Critical Perspectives on Accounting 50: 1–12. doi:10.1016/j.cpa.2017.11.001.

- Gonzalez, L. 1984. Racismo e sexismo na cultura brasileira. Ciências Sociais Hoje 223–244.

- Gonzalez, L. 2020. Por um feminismo afro-latino-americano. São Paulo: Editora Zahar.

- Haynes, K. 2008a. (Re)figuring accounting and maternal bodies: the gendered embodiment of accounting professionals. Accounting, Organizations and Society 33, no. 4-5: 328–48.

- Haynes, K. 2008b. Transforming identities: accounting professionals and the transition to motherhood. Critical Perspectives on Accounting 19, no. 5: 620–42.

- Haynes, K. 2017. Accounting as gendering and gendered: A review of 25 years of critical accounting research on gender. Critical Perspectives on Accounting 43: 110–24.

- Hermanson, D.R., R.W. Houston, C.M. Stefaniak, and A.M. Wilkins. 2016. The work environment in large audit firms: current perceptions and possible improvements. Current Issues in Auditing 10, no. 2: A38–A61. doi:10.2308/ciia-51484.

- Hines, R.D. 1988. Financial accounting: in communicating reality, we construct reality. Accounting, Organizations and Society 13, no. 3: 251–261. doi:10.1016/0361-3682(88)90003-7.

- Hirata, H. 2004. Trabalho doméstico: uma servidão “voluntária”? In Políticas Públicas e Igualdade de Gênero, eds T. Godinho, and M. L. Silveira, 43–54. São Paulo: Coordenadoria Especial da Mulher.

- Hirata, H. 2010. Novas configurações da divisão sexual do trabalho. Revista Tecnologia e Sociedade 6, no. 11: 1–7.

- hooks, B. 2018. O feminismo é para todo mundo: políticas arrebatadoras [Feminism Is for Everybody: Passionate Politics]. Rio de Janeiro: Rosa dos Tempos

- Instituto dos Auditores Independentes do Brasil [Ibracon]. 2017. Relatório de Gestão - Diretoria Nacional 2017 (Gestão 2015/2017) / Ibracon's Management Report 2017.

- Ittonen, K., and E. Peni. 2012. Auditor's gender and audit fees. International Journal of Auditing 16, no. 1: 1–18.

- Kerner, I., and B. Tavolari. 2012. Tudo é interseccional?: Sobre a relação entre racismo e sexismo. Novos Estudos - CEBRAP 93: 45–58. doi:10.1590/S0101-33002012000200005.

- Kokot-Blamey, P. 2021. Mothering in accounting: feminism, motherhood, and making partnership in accountancy in Germany and the UK. Accounting, Organizations and Society 93: 101255. doi:10.1016/j.aos.2021.101255.

- Kokot, P. 2014. Structures and relationships: women partners’ careers in Germany and the UK. Accounting, Auditing & Accountability Journal 27, no. 1: 48–72.

- Kokot, P. 2015. Let's talk about sex(ism): cross-national perspectives on women partners’ narratives on equality and sexism at work in Germany and the UK. Critical Perspectives on Accounting 27: 73–85.

- Komori, N. 2008. Towards the feminization of accounting practice. Accounting, Auditing & Accountability Journal 21, no. 4: 507.

- Kornberger, M., C. Carter, and A. Ross-Smith. 2010. Changing gender domination in a Big four accounting firm: flexibility, performance and client service in practice. Accounting, Organizations and Society 35, no. 8: 775–91.

- Lehman, C.R. 1992. “Herstory” in accounting: the first eighty years. Accounting, Organizations and Society 17, no. 3-4: 261–85.

- Lima, J.P.R., S.P.C. Casa Nova, R.G. Sales, and S.C.D. Miranda. 2021. (In)equality regimes in auditing: are we allowed to bring our true selves to work?. Revista Catarinense da Ciência Contábil 20: e3147. doi:10.16930/2237-7662202131471

- Lima, J.P.R., S.P.C. Casa Nova, F.F. Sauerbronn, and M. Castañeda. 2022. “Is it just a little flu”? producing a news-based counter account on COVID-19 discursive crises in Brazil. Accounting Forum, 1–25. doi:10.1080/01559982.2022.2149441.

- Lima, J.P.R., S.P.C. Casa Nova, and E. O. Vendramin. 2023. Sexist academic socialization and feminist resistance: (De)constructing women’s (Dis)placement in Brazilian accounting academia. Critical Perspectives on Accounting 102600. doi:10.1016/j.cpa.2023.102600.

- Lopes, I. F., and J.P.R. Lima. 2022. Diversidade e Inclusão: Reflexões e Impactos da Natureza Política da Contabilidade. Revista Contabilidade & Inovação, 1. doi:10.56000/rci.v1i1.71482

- Lupu, I. 2012. Approved routes and alternative paths: the construction of women's careers in large accounting firms. Evidence from the French Big Four. Critical Perspectives on Accounting 23, no. 4-5: 351–69.

- Lupu, I., and L. Empson. 2015. Illusio and overwork: playing the game in the accounting field. Accounting, Auditing & Accountability Journal 28, no. 8: 1310–40.

- Marcos, C., M. Vogt, and P.R. Cunha. 2017. Capital Psicológico no Trabalho e a Intenção de Rotatividade de Auditores Independentes. In: Proceedings of International Conference in Accounting. São Paulo, SP, 17.

- Nganga, C.S.N., W.M. Gouveia, and S.P.C. Casa Nova. 2018. Unchanging element in a changing world? women in accounting academy. Vol. 18. São Paulo, São Paulo: Congresso USP de Controladoria e Contabilidade.

- Oliveira, D.D. 2018. A violência estrutural na América Latina na lógica do sistema da necropolítica e da colonialidade do poder. Revista Extraprensa 11, no. 2: 39–57. doi:10.11606/extraprensa2018.145010.

- Paisey, C., N. Paisey, H. Tarbert, and B. Wu. 2020. Deprivation, social class and social mobility at Big four and non-Big four firms. Accounting and Business Research 50, no. 1: 61–109.

- Reid, E. 2015. Embracing, passing, revealing, and the ideal worker image: how people navigate expected and experienced professional identities. Organization Science 26, no. 4: 997–1017. doi:10.1287/orsc.2015.0975.

- Richardson, A.J. 2015. Quantitative research and the critical accounting project. Critical Perspectives on Accounting 32: 67–77. doi:10.1016/j.cpa.2015.04.007.

- Saffioti, H. 1976. A mulher na sociedade de classes: mito e realidade. Petrópolis: Vozes.

- Segato, R.L. 2018. Contra-pedagogías de la crueldad [Counter-pedagogies of cruelty], 101. Ciudad Autónoma de Buenos Aires: Prometeo Libros.

- Silva, S.M.C. 2016. Tetos de vitrais: gênero e raça na contabilidade no Brasil. São Paulo: Tese de Doutorado, Faculdade de Economia, Administração e Contabilidade, Universidade de São Paulo. doi:10.11606/T.12.2016.tde-03082016-111152.

- Silva, S.M.C., S.P.D.C.C. Nova, and D.B. Carter. 2016. Brazil, racial democracy? The plight of afro-descendent women in political spaces. Accounting in Conflict: Globalization, Gender, Race and Class 29: 29–56.

- Silva, A.R., A. Vasconcelos, and T.A. Lira. 2021. Inscrições contábeis para o exercício do poder organizacional: o caso do fundo de emancipação de escravos no Brasil. Revista de Administração de Empresas 61, no. 1. doi:10.1590/s0034-759020210106.

- Smith, M. 2022. Research Methods in Accounting. 6th ed. Sage.

- Tremblay, M.S., Y. Gendron, and B. Malsch. 2016. Gender on board: deconstructing the “legitimate” female director. Accounting, Auditing & Accountability Journal 29, no. 1: 165–90.