Abstract

The current study aims to examine how digitalization forensic accounting (DFA) demonstrates impact on accelerated internationalization (ACIN) and provides insights into the function of metaverse circular business model innovation (MCBMI) in the relationship between DFA and MCBMI. This study took advantage of a quantitative method and relied on deductive approach. The hypothesized model was investigated using structural equation modeling, which was rested on mathematical data collected from a survey circulated to a cross-sectional snowballing sample of 783 accountants in small and medium enterprises (SMEs). The data analysis was conducted using the Partial Least Squares Structural Equation Modeling (PLS-SEM) technique with the assistance of SmartPLS 4.0 software. The results analyses supported a strong relationship between DFA and MCBMI as well as the relationship MCBMI and ACIN in terms of significance and impact size. Conversely, DFA was reported to induce an insignificant impact on ACIN. The results further highlighted the role of MCBMI as a full mediator in the relationship between DFA and ACIN. The observations of this study would serve as a stable cornerstone to provide research pointers for follow-up works, in addition to providing scientific understandings by extending the current boundaries of this research string. From a practical standpoint, such important insights could enable the formulation of focused strategies for the implementation of circular business models as well as policies and regulations relevant to the adoption of metaverse platforms for boosting ACIN in SMEs.

1. Introduction

Adopting internationalization as a strategic choice is crucial for a company’s expansion and maintaining a competitive edge (Zhang & Cheng, Citation2023). Small and medium-sized firms (SMEs) that have quickly expanded their operations globally have emerged in emerging economies due to a changing economic and competitive environment (Machado & Bischoff, Citation2023). In order to survive and expand, SMEs are compelled to engage in accelerated internationalization (ACIN) due to increasing competition and evolving customer demands (Salamzadeh et al., Citation2022). An increasing number of SMEs worldwide are making efforts to expedite their process of accelerating their internationalization (Samant et al., Citation2023). According to Zalan (Citation2018), ACIN is becoming more and more common among SMEs early in their life cycles. ACIN establishes and strengthens a SME’s competitive advantage by utilizing resources that may be underutilized, acquiring new knowledge, effectuating (Uzhegova & Torkkeli, Citation2023), utilizing network effects, and hastily commercializing their goods or services (Freeman et al., Citation2010).

Technologies like the internet and the shifting dynamics of the global environment have given businesses the chance to expand internationally. These elements have influenced how businesses internationalize themselves while also advancing the field of internationalization research for SMEs (Christofi et al., Citation2021; Coudounaris, Citation2021). In particular, SMEs in emerging economies internationalize their activities by utilizing networking, information technology, and finance (Manolova et al., Citation2013; Ayob et al., Citation2015). Alternatively, businesses have been forced to reinvent themselves and innovate how they have created and captured value across foreign markets by way of innovating their business models as a result of the persuasive development of new digital technologies and the recent worldwide pandemic (Li et al., Citation2022; Sousa et al., Citation2020). Indeed, Anwar et al (Citation2024) advocated that digital skills help SMEs innovate their business model for the process of going global.

Remarkably, governments, profit-driven and non-profit organizations pressure businesses to pursue sustainability and offer sustainable goods as a result of these worries and the growing interest in sustainable development (Kannan, Citation2018). Furthermore, customers are becoming more and more aware of the moral ramifications of product manufacturing (Grazzini et al., Citation2021). Business leaders and decision-makers frequently see the circular economy (CE) as a viable approach to balance economic growth and sustainable development (Corvellec et al., Citation2022; Kirchherr et al., Citation2023). As such, circular business models have been developed to help organizations reduce waste and increase material retention, recycling, and reuse (Mostaghel et al., Citation2017). There is general consensus that digital transformation is essential for enabling the industry to implement circular economy procedures (Ertz et al., Citation2022; Patyal et al., Citation2022). While adapting to the concepts of CE, established enterprises that are founded on the conventional ‘take-make-dispose’ paradigm encounter significant obstacles (Blomsma & Brennan, Citation2017). Such obstacles include fewer resources than larger businesses, lacking of managerial expertise and financial resources (Micheli et al., Citation2021), and they frequently lack the necessary knowledge and support for innovation (Mitchell et al., Citation2020). In consequence, they frequently implement and employ fewer digital transformation than big businesses (Stentoft et al., Citation2021; Tamvada et al., Citation2022).

In response to this, managers should utilize the first mover advantage when it comes to technology like metaverse in the post-COVID-19 era (Gauttier et al., Citation2022). A fictional three-dimensional virtual environment called the Metaverse provides virtual reality experiences as an alternative to the real world. Future technologies like edge computing, blockchain, virtual reality, and augmented reality will all benefit from the Metaverse (Tlili et al., Citation2022). In addition to overcoming concerns like time, place, and financial constraints, the Metaverse can offer people with equal opportunities (Mehta et al., Citation2023). The ability of the Metaverse to endure and grow in the future without depleting natural resources is reflected in its sustainability (Zhang et al., Citation2023).

In this regard, businesses must create, develop, and use Metaverse circular business model innovation (MCBMI) in order to benefit from Metaverse and stay competitive in this tumultuous and complicated digital business environment. Unfortunately, a number of risks are associated with the growth of the Metaverse ecosystem, including those related to ownership, control, fraud, threats to personal information, ethics, accountability, and security challenges inherent in every transaction in the metaverse environment. Digital forensic analysis is needed to investigate crimes that occur in the Metaverse (Seo et al., Citation2023). More importantly, digital forensic accounting (DFA) refers to the utilization of digital technologies in accounting procedures, investigation strategies, and legal knowledge to analyze financial information, identify instances of fraud, and take measures to avoid it. As a result, digital forensic accountants are trained to proficiently utilize digital technology in order to analyze complex financial transactions and reconstruct financial records to identify anomalies, discrepancies, or patterns of fraudulent behavior.

This has incited the demand to rethink and formulate a new and in-depth insight on MCBMI, to tap higher potential and to achieve ACIN. Starting from these considerations on the lack of an established academic background on this specific subject, an analysis on how MCBMI can build up ACIN with the enabling role of DFA represents the main motivation in this research and underscores chances for theoretical and practical contributions. Also, this theoretical gap inspires the intriguing research questions as follows.

RQ1. What is the effect of DFA on ACIN?

RQ2. Does MCBMI act as a mediator in the interconnection between DFA and ACIN?

Given that SMEs’ internationalization has gained attention recently, particularly in emerging markets (Bai et al., Citation2021; Mishra et al., Citation2022; Nguyen et al., Citation2023), this study adds to the body of knowledge about this topic by extending the discussion of SMEs’ ACIN in developing nations. As a result, this study sheds light on the internal factors that encourage SMEs to internationalize more quickly. By concentrating on the issues surrounding sustainable development, it becomes possible to investigate how and why some SMEs are able to reinvent their business models and outperform their competitors. Rested on the perspective of Strange and Zucchella (Citation2017), established business structures, revenue streams, and the global reach of companies have all been impacted by the latest technological waves known as ‘Industry 4.0’. Concerning to this, SMEs have been particularly compelled to reinvent themselves and innovate in their value creation and capture processes across international marketplaces. In order to react swiftly to these outside threats and disruptions, many companies have embraced new platform-based digital business models, which drastically lower the minimum size and scale needed for a small digital company to do business beyond its original markets (Evers et al., Citation2023). Circular business model innovation or digital business model innovation have been the main topics of previous business model innovation research. Studies on business model innovation among SMEs have been few and far between (Bashir et al., Citation2023). The new proposal on creating organizational competencies that will ultimately result in enhanced performance and ACIN can help. This study adds to the scant body of research on the topic of using the Metaverse in business, which is still considered to be in its infancy (Mehta et al., Citation2023). Given that forensic accounting uses science and technology to identify fraudulent accounting, finance, and business practices (Rezaee et al., Citation2016), the goal of the research is to advance knowledge of the role of forensic accounting in the Metaverse environment by highlighting the connection between DFA and the development of circular business models in the Metaverse, which boosts international trade performance.

The economic progress of nations is greatly influenced by SMEs (Subrahmanya & Loganathan, Citation2021). They are involved in employment, exports, and ongoing innovation (Su et al., Citation2020). According to Jafari-Sadeghi et al. (Citation2022) as well as Subrahmanya and Loganathan (Citation2021), SMEs have been faced with a number of challenges including insufficient financial resources, weak managerial and entrepreneurial skills, marketing, low levels of technological adaption, and low productivity. As such, for SMEs looking to expedite their expansion, studying accelerated SME internationalization will have practical ramifications (Petrou et al., Citation2020). With a holistic focus on the circular business model, Metaverse application, and forensic accounting, the paper offers managerial and operational pointers as well as a roadmap to practitioners and policymakers at the policy degree. The results of this study also suggested practical steps that software or information technology suppliers could take to introduce cutting-edge methods that best met the expanding needs of potential clients.

The remainder of this manuscript is planned thus: Section 2 gives the theoretical understanding, and Section 3 contains the manuscript’s research hypotheses and proposed model. The research methodology used for the study is captured in Section 4. Analysis and discussion of the results are deepened in the penultimate section. In the final section, implications and directions for additional research are exposed.

2. Theoretical comprehension

2.1. Contingency theory

The contingency theory (CT) is in opposition to the established classical conceptions of managing organizations and society (Akinwale & Onokala, Citation2022). According to Islam and Hu (Citation2012), CT was an approach to the study of organizational behavior that explains how contingent factors affect the structure and operation of organizations. Its fundamental premise was that no single organizational structure can be applied to all organizations equally; organizational effectiveness instead depends on a fit or match between the kind of technology, the volatility of the environment, the size of the organization, the organizational structure’s features, and its information system (Nkundabanyanga et al., Citation2022). Accordingly, research based on CT contend that organizational results were the result of how well two or more components fit together (Islam & Hu, Citation2012). Any work that an organization did involve interactions between the task, people, environment, structure, and technology, according to Leavitt (Citation1972). Strategic and operational configurations were taken into account as part of a systematic process for managing disruptive events to develop resilience (Lozada-Contreras et al., Citation2022). An essential component of business strategic decision-making was risk management. The successful implementation of an effective risk management system depends on a variety of factors, and these decisions will be frequently made in the future (Kulchmanov et al., Citation2016).

2.2. Conceptual respects

2.2.1. Digital forensic accounting

Based on the viewpoints of Xanthopoulou et al. (Citation2023), forensic accounting protected the accuracy of economic data by means of identifying patterns and suspicious transactions, spotting trends and suspicious activities, identifying suspicious transactions and patterns, spotting and mitigating accounting crimes, and ultimately eradicating them. According to Rehman and Hashim (Citation2021), forensic accounting referred to the application of accounting principles, theories, and methods to analyze and resolve factual or hypothetical issues in a legal context. It incorporated all areas of accounting knowledge and practices used by accountants to address legal disputes. With the rapid development of digital technology, Akinbowale et al. (Citation2023) suggested integrating big data into forensic accounting in the banking sector. DFA focuses on the incorporation of digital technologies into forensic accounting methodologies. Consequently, forensic accounting can evaluate the events in accounting, auditing, and legal dimensions in this way with the aid of these types of digital technologies to produce accurate and trustworthy information about the market, politics, and the environment for the achievement of better monitoring and predicting the behavior of suppliers and customers.

2.2.2. Metaverse circular business model innovation

The term ‘Metaverse’ has gained popularity among tech companies (Dolata & Schwabe, Citation2023). Finding an acceptable definition of the term ‘Metaverse’ may be difficult because so many disciplines are engaged in its development. As a result, there has been no universal agreement on what constitutes a metaverse (Koohsari et al., Citation2023). Under the viewpoint of business, management and accounting, the business activities and commercial applications that virtual worlds can support will be the main emphasis of the research of Papagiannidis et al (Citation2008), which will also look at the broader ramifications of these frequently referred to as ‘Metaverses’ virtual environments. To put it concretely, the so-called Metaverse, a virtual realm analogous to the atom-based world in which we live, is made up of four cutting-edge technologies. These technologies include augmented reality (sensory overlays of digital information on the real or even virtual world), virtual worlds (digital representations of any space imagined to exist), mirror worlds (digital representations of our own atom-based world), lifelogging, and virtual reality (Boulos & Burden, Citation2007). The future of the technologies and ecosystem elements driving the migration from the existing Internet to the metaverse have a significant impact on the correct development of the metaverse (Vidal-Tomás, Citation2023). According to Lee et al. (Citation2021), there were eight potential enabling technologies (extended reality, user interactivity, artificial intelligence, blockchain, computer vision, internet of things and robotics, edge and cloud computing, and future mobile networks) as well as six ecosystem aspects (avatar, content creation, virtual economy, social acceptability, security and privacy, and trust and accountability) that must be improved in order to let human users live and play within a persistent, shared virtual world.

A circular business model is an approach to running a company that combines CE concepts and tactics for slowing down, enlarging, or closing resource loops (Santa-Maria et al., Citation2021). It can be thought of as a subset of sustainable business models (Henry et al., Citation2019). Emerging circular business models are supported by key activities that include developing new business models and reshaping old ones (Tukker, Citation2015). Therefore, the process of altering current business models to create (more) circular configurations that would (re)create, (re)deliver, and (re)capture value, or the process of developing entirely new circular business models to create, deliver, and capture value in novel ways, can be defined as circular business model innovation (Guldmann & Huulgaard, Citation2020). As proposed by Dubey et al. (Citation2022), Metaverse helped to foster a culture of CE through reusing, refilling, and reducing waste through technology. In this research, MCBMI reflects on a series of intentional actions that managers and business owners do to gradually modify and develop the circular business model’s components and architecture in a consistent manner on the Metaverse platform.

2.2.3. Accelerated internationalization

Accelerated internationalizers differ from slower internationalizing enterprises, according to studies on the pace of internationalization, mostly in terms of the entrepreneur’s cognition, knowledge base, and access to networks (Petrou et al., Citation2020). According to Casillas and Moreno-Menéndez (Citation2014) and Kuivalainen et al. (Citation2012), the idea of ACIN has emerged as a critical strategic choice for companies seeking to enter global markets. Focusing on the pre-internationalization stage, ACIN is the interval between a company’s formation and the start of its international activities (Jones & Coviello, Citation2005).

3. Research hypotheses development and research model formulation

Globally, the frequency of dishonest and suspicious financial transactions is rising, putting organizations at danger of dishonest and fraudulent practices. The increasing incidence of business crises globally is evidence that this trend has increased demand for forensic accounting (Islam et al., Citation2011). SMEs would be advised, based on the viewpoints of Freeman et al. (Citation2006), to pay attention to the uncertainty arising from a number of determinants, including information asymmetry, geographic space, and the complexity of both implementing contracts across borders and determining the capacities of a foreign distributor if they hope to improve and develop their internationalization operations. According to Hennart (Citation2010), transaction costs included costs associated with monitoring, information, negotiation, and enforcement. Businesses frequently have to deal with the risk of being unable to fulfill the contractual conditions of an agreement while working with foreign partners. The host nation’s and the home nation’s dissimilarities in culture and institutions were one tenable explanation. Additionally, individuals had to deal with the possibility of being duped by unsatisfactory exchanges of goods or services or other opportunistic acts (Hennart, Citation2012), as there were no methods to judge the reliability of other party’s ex ante. In this regard, DFA can enable SME to address these issues in an efficient and effective manner. More concretely, blockchain technology can help forensic accountants prove that assets exist, are owned by certain parties, and have been transferred (Garanina et al., Citation2022). Blockchain-based smart contracts would reduce the costs associated with principal-agent relationships that result from competing interests in contracting (Murray et al., Citation2019). On the other hand, blockchain and smart contracts had the ability to encrypt the necessary data in the transaction to eliminate the risk of inaccurate data (Hennart, Citation2001). Additionally, by automating contract execution built on pre-programmed terms, blockchain and smart contracts may be able to equalize the importance of counterparties with widely varying sizes in supplier-buyer transactions (Murray et al., Citation2019). This would increase fairness and competitiveness for SMEs by preventing the more powerful party from exerting greater pressure on the weaker party to amend contract terms (Cole et al., Citation2019). As advocated by Gnizy (Citation2019), informational processes have been an element of a company’s exploratory competency when it comes to competing globally because exporters who possess related information are more likely to have a greater number of opportunities from overseas marketplaces. In light of this, big data may provide real-time, detailed, and multi-source information to manage this significant uncertainty, research and scan the market, as well as assess risks (Dam et al., Citation2019; Gnizy, Citation2019). Data analytics methods are being used more frequently in forensic accounting for fraud detection and prevention, according to Rezaee and Wang (Citation2019). In light of analysis covered above, the first hypothesis of this study is logically proposed as follows

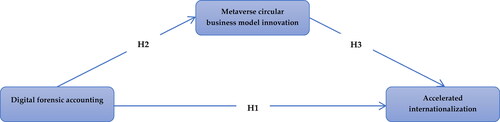

Hypothesis 1 (H1). DFA engenders a significant and positive effect on ACIN.

The implementation of the circular business model innovation among SMEs is pondered to be hindered by associated difficulties and cross-disciplinary risks, which frequently deter organizations. In particular, restructuring is expensive and hazardous. Managers who stand to gain from the current structure may be resistant, which could prevent the firm and the environment from experiencing the anticipated benefits (Hoffman & Bazerman, Citation2007). Partners work closely together and become more reliant on one another, according to Barquet et al. (Citation2016), which is a risk that needs to be managed. Additionally, validation cannot be achieved without subsequent sales, and resource exposure risk increases during validation (Linder & Williander, Citation2015). On the other hand, businesses also have to tackle with risk in the market or business environment as a result of a poor economic cycle or a lack of financial stability, which lowers demand for goods globally (Brillinger et al., Citation2020; Yazdani et al., Citation2019), risk related to significant upfront investment costs and capital expenditures necessary to develop and fulfill the value proposition of the new business models, including expenditures for manufacturing facilities and inventory (Dulia et al., Citation2021; Urbinati et al., Citation2021), risk brought on by unfavorable changes in tax laws, such as a reduction or elimination of tax benefits for green products, and/or uncertainty over changes to fiscal policies (Brillinger et al., Citation2020; Dulia et al., Citation2021; Yazdani et al., Citation2019). Moreover, legal problems are emerging for non-ownership business models because service providers are not permitted to legally retain ownership of a sold product (applicable only to non-ownership business models) (Dulia et al., Citation2021; Govindan & Hasanagic, Citation2018); and risks related to the loss of intellectual property or know-how, including private information about the organization’s partners (Brillinger et al., Citation2020; Urbinati et al., Citation2021) are the additional concerns that are causing businesses to be reluctant to deploy circular business model innovation. The development of the metaverse ecosystem entails a number of hazards, including those connected to law, ownership, control, fraud, threats to personal information, ethics, accountability, and security difficulties inherent in each transaction in the metaverse environment. Investigation of crimes that take place in the Metaverse requires digital forensic research (Seo et al., Citation2023). In the field of accounting known as DFA, financial fraud and misbehavior are identified and prevented through the use of investigative and analytical methods. DFA can, in fact, improve the capabilities in identifying and preventing financial fraud, losses, and dangers with the help of technological improvements. The use of data analytics tools to find trends, abnormalities, and probable financial frauds is a key component of DFA, and data analysis is one of these. Data analytics approaches used by digital forensic accountants include data mining, machine learning, and predictive modeling. These methods may examine huge amounts of data to find correlations between data points and identify fraud indications. Additionally, machine learning and artificial intelligence can evaluate vast amounts of data and spot trends that point to fraudulent activity (Ali et al., Citation2022). Digital forensic accountants can evaluate the efficiency of cybersecurity-related internal controls and make recommendations for enhancements to prevent fraud and hazards during implementation MCBMI. In light of analysis covered above, the second hypothesis of this study is logically proposed as follows

Hypothesis 2 (H2). DFA engenders a significant and positive effect on MCBMI.

The CE concept is used by businesses to produce values, which is an advantage for them from a business standpoint. Using both environmental and economic benefits built into products, circular business model innovation assist in balancing resource efficiency with the generation of commercial value (Bocken et al., Citation2016). Enterprise will increase operational efficiency and lower costs by reducing waste and inefficiencies in production and distribution in addition to resource efficiency (Arnold et al., Citation2023). They might construct a closed resource flow for their own company or produce resources for other market participants. The enlarged obligation of the manufacturer is supported by this business model. The obligation of the product’s maker extends all the way to the conclusion of its life cycle (Bocken et al., Citation2016). Circular business models can improve supply chain stability by lowering inefficiencies and boosting loyalty in terms of sustainability requirements along the entire value chain (Arnold et al., Citation2023). In addition, they help the firm maintain supply chain alliances. Therefore, if purposefully created (Tukker, Citation2004; Tukker, Citation2015), these business models could greatly lessen the harmful effects on the environment (Ferasso et al., Citation2020). Many of the current digital transformative technologies for manufacturing will be enhanced by the metaverse (Dwivedi et al., Citation2022). In the context of managing manufacturing operations, Metaverse will practically improve industrial capability through technologically driven innovation such as digitization, artificial intelligence, and manufacturing, structure optimization, and emphasis on quality, encourage and maintain access to and mastery of such technologies, and maintain ‘industrial and technological sovereignty’ through reshoring global value chains (Koohang et al., Citation2023). The deployment of MCBMI will facilitate SMEs to handle societal as well as environmental challenges or focusing on sustainability, increasing customer and stakeholders appeal and loyalty through providing new services or distinctive customer experiences as well as integrating the product-as-a-service model, repair and maintenance services, and product recycling programs into the customer experience. It also helps businesses comply with regulatory regulations. Companies that implement circular business models will be better positioned to meet these requirements and avoid penalties as sustainability and waste regulations become more stringent. By doing this, the organization also helps to show its dedication to sustainability, which might draw funding from investors. In light of analysis covered above, the third hypothesis of this study is logically proposed as follows

Hypothesis 3 (H3). MCBMI engenders a significant and positive effect on ACIN.

Expanding upon the aforementioned analyses, illustrates the research model that depicts the postulated interconnections between the DFA and ACIN, with MCBMI serving as a mediator.

4. Overview of the methodology and justification

4.1. Research context

SMEs has experienced significant growth and has become an active and energetic part of the global economy (Ali Qalati et al., Citation2020). In contrast to large corporations, SMEs possess a remarkable level of flexibility, which enables them to effectively respond to technological changes, promote income distribution, and adapt to market fluctuations and evolving customer demands (Perez-Gomez et al., Citation2018). Moreover, their organizational structure facilitates swift decision-making processes (Perez-Gomez et al., Citation2018). Furthermore, SMEs have exhibited adaptability and versatility in executing strategic manoeuvres, enabling them to promptly make necessary modifications in unpredictable circumstances (Williams et al., Citation2017).

Vietnam is an emerging nation in Southeast Asia that is experiencing fast economic growth and SMEs in Vietnam function within the framework of government policies and programs that aim to foster the development of SMEs (Adomako & Nguyen, Citation2023). Admittedly, the Vietnamese government has made changes to encourage entrepreneurship, simplify the steps needed to start a firm, and help SMEs financially. The chosen entities in this study were SMEs located in Southern Vietnam. These firms were frequently chosen in several prior research on the implementation of innovation (e.g. Nguyen and Wongsurawat, Citation2012; Hoang and Otake, Citation2014), as the southern regions have been regarded as the most vibrant places in Vietnam. SMEs in several industries in Southern Vietnam have significant comparative advantages over larger corporations, enabling them to respond promptly and efficiently to evolving global trends. According to Ha et al. (Citation2022), innovation implementation was more promptly and efficiently embraced by SMEs in Southern Vietnam compared to other regions of Vietnam. The emergence and growth of SMEs in Vietnam may be traced back to the late 19th century in Southern Vietnam, during the period of French colonial control (1884-1945). During the period from 1954 to 1975, the expansion of SMEs was particularly noticeable. However, this growth was mainly observed in South Vietnam, as the establishment and operation of private businesses were not allowed in the centrally planned economy of the North. However, the reunification of North and South Vietnam in 1975 led to the implementation of the North’s system and the immediate nationalization of all private companies. Consequently, despite the similar economic development across Vietnam, each region still exhibits distinct characteristics, especially in the implementation of innovation (Ha et al., Citation2022).

4.2. Operationalization of measurement variables

This study took advantage of a quantitative method and relied on deductive approach. Accounting staff from several SMEs in Vietnam’s Southern region took part in the cross-sectional survey. This method allowed the researchers to thoroughly investigate the current study questions by guaranteeing a representative sample that was both varied and inclusive. Hinged on the research objectives, survey is considered as the most appropriate approach for the current work because it is frequently used in non-experimental design and theory testing (Elkaseh et al., Citation2016). Questionnaires are used as the method for acquiring the study’s data. The survey questionnaire is created by reviewing the literature and leveraging pertinent concepts from earlier publications. The questionnaire, which is written in English, is made up based on the tools identified by earlier investigations. A professional who is fluent both languages carried out the translation. The translator translated the completed Vietnamese questionnaire back into English. To assess the respondents’ points of view or attitudes, a questionnaire of the five-point Likert scale is used (Burns & Grove, Citation2009). The pre-tested approach with 7 experts was also used to minimize unanticipated complexity (Montgomery & Stone, Citation2009). The constructs were modified to eliminate unclear measuring items hinged on expert feedback. In order to confirm the questionnaire and measurement tools as recommended by Kothari (Citation2004), a small-scale pilot test with 30 participants is conducted. Based on their feedback, only a few minor changes are subsequently made.

4.2.1. Digital forensic accounting

The four second-order constructs of governance, fraud detection, internal controls, and anti-fraud policies were included in the first-order construct used to evaluate the DFA. More practically, the criteria utilized in this study’s evaluation of anti-fraud policies are derived from those advanced by Lloyd Bierstaker (Citation2009) and Carvalho et al. (Citation2018). The criteria utilized in this study to assess governance are derived from those put forth by Law (Citation2011) and Carvalho et al. (Citation2018). The criteria utilized in this study to assess fraud detection are derived from those put out by Yogi Prabowo (Citation2012) and Carvalho et al. (Citation2018). The criteria utilized in this study’s evaluation of internal controls are derived from those advanced by Rae and Subramaniam (Citation2008) and Carvalho et al. (Citation2018).

4.2.2. Metaverse circular business model innovation

The four second-order constructs of exchangeable, actor, activity, transaction mechanism and governance were included in the first-order construct used to evaluate the MCBMI. More practically, the criteria utilized in this study to assess exchangeable, actor, activity, transaction mechanism and governance are derived from those put forth by Arnold et al. (Citation2023), Koohang et al. (Citation2023), Dubey et al. (Citation2022), Periyasami and Periyasamy (Citation2022), Haftor and Costa (Citation2023).

4.2.3. Accelerated internationalization

In this research, ACIN is measured through the multi-item construct formulated from those recommended by Chebbi et al. (Citation2023).

4.3. Sampling procedures and data collection

The subject of the analysis is SME, and the main source of information for this study is accountants in SMEs.

The focus of this research was on SMEs accountants who could offer insightful analysis and deep knowledge on pertinent topics from their organizations’ perspectives. In order to be considered for participation, candidates must have a solid grasp of digitalization on accounting, forensic accounting, business model innovation, circular economy, metaverse, and ACIN. They must also have worked for their organizations for at least eight years in their organizations. To make sure they had the information to fill out the survey, participants were also asked to rate their level of acquaintance with the application of digitalization on accounting, forensic accounting, business model innovation, circular economy, metaverse, and ACIN in an organizational setting. By following these steps, the researchers might be sure that the dataset was free of people who were oblivious to these issues. The nonprobability sampling method known as snowball sampling was used to select study volunteers from among the researchers’ acquaintances. When there were difficult-to-reach groups or transportation constraints, this strategy had the advantage of addressing anonymous persons. The researchers made every effort to ensure the ethical integrity of the current study. Participants were provided with a comprehensive elucidation of the study’s goals, their entitlements, and the safeguarding of their response confidentiality (Khoa, Citation2023). Prior to data collection, explicit agreement was obtained from each participant, and stringent protocols were adopted to safeguard anonymity throughout the study (Khoa, Citation2023). Non-response was addressed by employing participant reminders and ensuring their anonymity was maintained. It was critical to ensure the model’s sample size was enough before developing SEM. It appears that the 10-time rule was employed to streamline the process of size estimation, as stated by Kock and Hadaya (Citation2018). According to Sekaran and Bougie (Citation2013), most social science inquiries with unknown population estimates could be adequately studied with a sample size ranging from 30 to 500 respondents. Data were collected between the months of November 2022 and April 2023. A total sample size of 783 cases with a data loss rate of 15.81 percent was remained after screening and reviewing the questionnaires. presents comprehensive demographic data gathered from the study.

Table 1. Distribution of participants based on demographic characteristics.

4.4. Data analysis

According to Arshad et al. (Citation2023), PLS-SEM is a commonly used method for analyzing multivariate data. Complex research models, which combine theory with empirical data and function as estimation frameworks, can be analyzed using the Smart PLS-SEM (Sobaih & Elshaer, Citation2022). Remarkably, PLS-SEM is being favored more and more due to its exceptional prediction capabilities. To make out-of-sample predictions, predictive modeling use statistical models (Manley et al., Citation2021; Sarstedt and Danks, Citation2022). The demographic data of the respondents was analyzed by using SPSS version 29.0 software. Moreover, PLS-SEM was used with software Smart PLS 4.0.9.2 to confirm the hypothesized model of the current research. Building on the perspectives of Sarstedt et al. (Citation2014), it took two steps to analyze the PLS-SEM results. The validity and reliability of the measurement model were investigated in the initial stage. In Stage 2, the structural model was assessed for its predictive usefulness, path coefficient significance, and indirect impacts.

5. Result analysis and discussion

5.1. Measurement model

In a research project, the measurement model was considered as a statistical model that evaluated the reliability of measurement scales. It entailed employing several items or indicators to measure several constructs or variables. The measurement model’s main goal is to make sure the items accurately represent the underlying ideas that they are meant to assess.

Cross-loading, which was used to evaluate content validity, revealed that the meanings of the questionnaire items were the same as those that were incorporated into particular concepts by Ur Rehman et al. (Citation2019). A construct’s value must be higher than the values of the other constructs in the same rows and columns in order to do this (Hair et al., Citation2010). The assessment scale utilized in this investigation attained full content validity, as evidenced by the values for all tested constructs displayed in .

Table 2. Results summary for the content validity.

To confirm the authenticity and trustworthiness of the research, several testing procedures were carried out. The reliability of the measuring scales was also evaluated using Cronbach’s alpha, composite reliability (CR), and Dijkstra-Henseler rho as recommended by Hair et al. (Citation2022). Cronbach’s alpha, CR, and Dijkstra-Henseler rho values for each construct should be higher than the recommended cutoff value of 0.70 (Hair et al., Citation2022). The necessary detail of reliability shown in demonstrated that this study achieved the reliability of the measurement model.

Table 3. Results summary for Construct reliability.

According to Sarstedt and Cheah (Citation2019), the factor loading is the correlation between latent construct elements with a value greater than 0.7. The average variance extracted (AVE) was evaluated in the next phase. According to Hashmi et al. (Citation2021), all constructs had AVEs that were higher than the minimally acceptable value of 0.50, demonstrating a decent level of convergent validity. The necessary detail convergent validity shown in demonstrated that this study achieved the robustness of the measurement model.

Table 4. Results summary for Convergent validity.

As stated by Farrell (Citation2010), cross-loadings initially required that the factor loadings of each component item relevant to its linked construct be greater than those of other constructions. The data in thus shows that no item has a bigger load in a construct other than the one it measures.

Second, as shown in , the discriminant validity met the Fornell-Larcker requirement, which states that the square root of each construct’s AVE must be greater than the correlation between a given construct and all others (Fornell & Larcker, Citation1981). This metric has drawn criticism since variance-based SEM techniques may overestimate factor loadings and underestimate structural model links (Henseler et al., Citation2015). The third criterion was consequently issued.

Table 5. Results summary for discriminant validity on Fornell–Larker criterion.

Using the heterotrait-monotrait ratio (HTMT), the connections were estimated. As proposed by Henseler et al. (Citation2015), it was the average of item correlations between constructs as opposed to within a single concept. The HTMT measurements should not exceed a threshold value of 0.9, according to Henseler et al. (Citation2015). While some researchers claim that 0.85 and lower is the optimum HTMT range (Franke & Sarstedt, Citation2019), as stated by Deng and Yu (Citation2023), the threshold value was proposed to be 0.85 when conceptions were conceptually dissimilar and 0.90 when they were conceptually similar. Additionally, the percentile approach and bootstrapping with 10,000 subsamples were used. The criteria were one-tailed testing and a 0.05 level of significance. The HTMT statistic was significantly below the threshold value of 0.85, as shown by the bootstrapping analysis results in , which validated the discriminant validity (Franke & Sarstedt, Citation2019).

Table 6. Results summary for discriminant validity on Heterotrait–Monotrait ratio.

5.2. Structural model

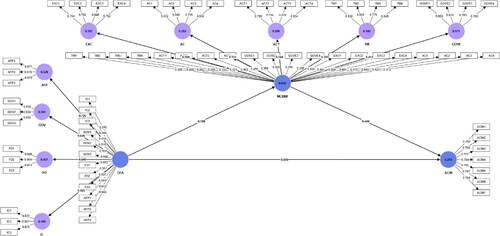

The structural model was utilized to evaluate the interconnections between the independent factors and the dependent variables. It enabled researchers to comprehend the impact of alterations in DFA and MCBMI on the structural correlation when combined with ACIN. Structural models facilitated the analysis of both direct and indirect relationships between constructs, enabling researchers to evaluate their suggested hypotheses in the conceptual model. Due to all inner variance inflation factor (VIF) values being well below the necessary threshold value of 3 in the initial step, there were no substantial collinearity difficulties (Hair et al., Citation2022). The second stage involved evaluating the importance and magnitude of the structural model relationships using SmartPLS 4.

Direct effect

For the purpose of determining whether or not the path coefficients are statistically significant, the bootstrapping approach (percentile bootstrapping, two-tailed test, 0.05 significance level, with 10,000 resamples) was utilized (Streukens & Leroi-Werelds, Citation2016). The bootstrap results revealed that DFA markedly and positively influenced MCBMI (β = 0.188; t-value = 4.801; p-value = 0.000). In the same vein, MCBMI was corroborated to demonstrate noteworthy and positive impacts on ACIN (β = 0.449; t-value = 13.171; p-value = 0.000). In contrast, the results analysis highlighted that DFA had insignificant influence on ACIN (β = 0.049; t-value = 1.448; p-value = 0.148). Thus, H2, H3 were accepted while H1 was rejected.

Indirect effect

Nitzl et al. (Citation2016) argued that the bootstrap technique is more appropriate than the Sobel (Citation1982) test for assessing indirect effects. The significance of the indirect effect of DFA and ACIN via MCBMI was assessed. The bootstrapping outcomes demonstrated that the indirect effect between DFA and ACIN via MCBMI was significant (p < 0.05); however, the direct effect of MCBMI and ACIN was also supported while the direct effect of DFA and ACIN was not supported, it was inferred that MCBMI fully mediated the interconnection between DFA and ACIN (Hair et al., Citation2022).

The third stage encompassed evaluating the model’s explanatory or in-sample predictive capacity. The R2 was 0.035 for MCBMI and 0.212 for ACIN. The analysis revealed that DFA had a small effect size on ACIN (0.003). In the same vein, DFA had a small effect size on MCBMI (0.037). Conversely, MCBMI had a medium effect size on ACIN (0.246). and depicted the structural model that was created during the execution of the PLS algorithm in SmartPLS 4.

Figure 1. Hypothesized model.

Figure 2. Structural model.

Table 7. Results of hypotheses testing.

When compared to a linear benchmark model, the model could not illustrate perfect out-of-sample prediction capabilities for all construct indicators. The PLSpredict (Shmueli et al., Citation2019) results in outlaid that the RMSE acquired by the linear model (LM) was much smaller than the RMSE acquired by PLS-SEM for almost all items. Moreover, when employing the cross-validated predictive ability test (CVPAT) (Liengaard et al., Citation2021; Sharma et al., Citation2023), the result analysis disclosed that the LM possessed a reduced average loss than the PLS-SEM. Alternatively, PLS-SEM could outperform the naive indicator average (IA) prediction benchmark for both PLSpredict and CVPAT. To this end, the model acquired some predictive capability that enabled it to pass the IA test but not the more conservative LM benchmark.

Table 8. Predictive model assessment.

5.3. Discussion

Contrary to the expectation of the researchers, the statistical evidence was inadequate to establish a substantial influence of DFA on ACIN. Nevertheless, the aforementioned research findings carried specific implications. Primarily, the discoveries contributed to the existing knowledge in the domain of implementing digital technology in forensic accounting. This study introduced a novel examination of the application of DFA among SMEs and its correlation with ACIN. Moreover, this study is novel as there has been no other literature research, to the authors’ knowledge, that has examined this problem from a forensic accounting standpoint. Even though the results indicated that DFA has a negligible effect on ACIN. This research would be beneficial for SMEs since it considered the specific attributes of DFA that might improve their international commercial operations. For SMEs to engage in international activity, internationalization risks are not a barrier; rather, it is how they are managed that causes SMEs to increase their performance (Calzadilla et al., Citation2022). A sound risk management procedure is required to control any implicit hazards that internationalization may bring about and to reduce any harm they may do in order to boost organizational performance (Ferreira de Araújo Lima et al., Citation2020). While digital forensics is the process of uncovering evidence and establishing facts by utilizing a deep understanding of the inner workings of networks, computers, and other associated equipment (Awodiran et al., Citation2023), forensic accounting is a specialized field that integrates expertise in accounting, investigative skills, and legal understanding to uncover instances of financial crime, provide support in legal disputes, and assist in legal processes (Kaur et al., Citation2023). Unfortunately, forensic accounting is still not adopted earlier or involved more proactively, falling under the risk management function although ‘fraud risk’ management is becoming more and more important and is becoming more and more important in the corporate governance field (Power, Citation2013), especially internationalization operations.

In consonance with the anticipation of the researchers, the results analysis underlined the potential role of DFA in enhancing the effectiveness of MCBMI. To the best of the understandings of researchers, this scholarly effort may be the first to provide new and significant insights into the highly distinctive effects of DFA on MCBMI. Nonetheless, this finding enlarged the perspectives of Seo et al. (Citation2023) on the prerequisite of digital forensic investigation framework for the metaverse. Admittedly, while the Metaverse has been regarded as a potentially lucrative business model for the future (Periyasami & Periyasamy, Citation2022), its implementation may give rise to cybersecurity vulnerabilities (Jaipong et al., Citation2022). Moreover, organizational databases encompass a wealth of information that pertains to a company’s financial performance, clients, suppliers, and other pertinent details regarding the company’s operations. This can be viewed as a crucial determinant for the successful implementation of MCBMI. Regrettably, organizational databases are also drawing the attention of criminals who are making use of many advanced and developing digital technologies. Significantly, all of these electronic media generate digital footprints, which offer valuable data for the process of digital investigation. The increasing prevalence of digital crime, which involves the unauthorized access and theft of large amounts of sensitive information from databases, necessitates the need for specialized knowledge and a well-informed strategy in the field of database forensics (Boumediene & Boumediene, Citation2023). One significant obstacle at the organizational level that impedes the adoption of circular business models is the lack of clarity regarding regulation in this domain (Guldmann & Huulgaard, Citation2020). Regarding this matter, utilizing DFA would serve as a potent instrument for facilitating the implementation of MCBMI by SMEs. Reasonableness testing, often refers to as substantive analytical methods of DFA, comprises of assessing the operational data of an organization, including interconnections and trends, to ascertain their conformity with expectations, industry standards, or prior periods. On the other hand, the anti-fraud policies function as facilitators to assess risks and diminish occurrences of financial fraud in SMEs, while also being adjusted to tackle prevailing economic circumstances. Corporate governance refers to a system of regulations, standards, and procedures that control the administration and supervision of a company’s activities and decision-making processes (Alzoubi, Citation2023). The primary objective of corporate governance is to guarantee the implementation of ethical, responsible, and accountable practices, while concurrently creating sustainable value for all stakeholders. The primary objective of digital forensic techniques is to collect, analyze, and protect digital evidence. Alternatively, internal control systems play a crucial role in preventing and detecting fraud within a business. These strategies are primarily used to ensure the efficient implementation of DFA, which is capable of minimizing instances of fraud and cyber fraud. This, in turn, contributes to the success of MCBMI.

In accordance with the researchers’ expectations, MCBMI was highlighted to demonstrate significant effect on ACIN. Alternatively, the statistical outcomes of the current research shed light on the full mediating role of MCBMI in the interconnection between DFA and ACIN. In other words, the more efficiency and effectiveness the DFA acquired in the process of addressing risk in MCBMI, the more likelihood SMEs could succeed in ACIN. To the best of the understandings of researchers, this is the first scholarly investigation to shed light on the fresh and paramount understanding on the incredibly unique effects of MCBMI on ACIN as well as its full mediating role in the interconnection between DFA and ACIN. In light of concerns about pollution and the overexploitation of the planet’s resources, many view internationalization and technological advancement as environmentally hazardous (Attig et al., Citation2016; Karlsson, Citation2017). The key to driving development and global prosperity along these growth trajectories is ensuring their sustainability (Kusi-Sarpong et al., Citation2019; Maksimov et al., Citation2019). Research on sustainability in SMEs has recently increased (Bartolacci et al. Citation2020; Bakos et al. Citation2020), reflecting the topic’s popularity in both academic and practitioner community. Therefore, MCBMI has been seen as a replacement for the conventional SME model, which is defined by a smaller geographic reach, less technological sophistication, and a lack of concern for environmental impact (Denicolai et al., Citation2021). As advocated by Zhu et al. (Citation2022), the circular transition may be crucial to the survival and expansion of SMEs. Notably, the process of company internationalization can be accelerated by digitalization in the age of the digital economy (Feliciano-Cestero et al., Citation2023; Caputo et al., Citation2022). As the Metaverse can give human with equal possibilities while also addressing real-world issues like as time, space, and cost barriers (Mehta et al., Citation2023), it will become in appropriate with the SMEs which feature by the lack of human resources and financial constraints (Micheli et al., Citation2021). On the other hand, the sustainability of the Metaverse was extensively detailed in the work of De Giovanni (Citation2023). Hence, the importance of digitalization and business models in the internationalization of SMEs are underscored by several academicians (Reim et al., Citation2022; Yu et al., Citation2022). Taken together, the implementation of MCBMI will intensify the performance of ACIN.

6. Final thoughts and suggestions for the future

6.1. Practical implication

The findings have implications for managerial practice, especially for SMEs pursuing international expansion during times of crisis and post crisis. First, the findings in this manuscript help SME managers to understand the importance of ACIN to SMEs. According to our results, government officials and SME managers should spend as much effort as possible precisely understanding how to help SMEs to succeed in ACIN. To do so, SME managers can develop contingency plans that can help mitigate the negative impact of crises on their businesses. Second, officials and SME managers must also consider situational factors like the potential impacts when planning a rapid international expansion. In order to reduce or eliminate the numerous risks, managers of SMEs should increase their firms’ agility as they conduct ACIN. Furthermore, since the institutional contexts of some host countries expose firms to increased uncertainty (Shirodkar & Konara, Citation2017), SMEs should seek to accelerate international expansion in host countries with effective DFA and MCBMI. The full mediating role of DFA in the interconnection between MCBMI and ACIN placed emphasis on the potential role of DFA in ACIN. This would help SMEs to navigate the complexities of international expansion and minimize risks associated with doing business in unfamiliar environments. Effective DFA can help SMEs be more adaptable and gain competitive advantages in their dynamic home market, supporting their international expansion. Managers in SMEs should develop their managerial cognitive abilities and give DFA more attention through creating a supportive environment in the workplace to ensure the stability of the forensic accounting environment. Besides, consolidation of tangible resources, such as infrastructure and digital platforms, as well as other necessary resources for forensic accounting implementation, is encouraged concurrently. Forensic accountants should be trained to recognize the importance of their role in society, and to conduct their work in a manner that is aligned with societal expectations. The most important skill is experience. This experience is gained through simply maturing in the profession. The forensic accountant acquires skills in accounting and auditing, taxation, law, economics, information technology, business operations, and management, internal controls, interpersonal relationships and communication. They are advised to grasp and abide by the rules governing information gathering, preservation, analysis, relevancy and admissibility of the processed information in evidence in the law court and be professional at all times. All managers in SMEs should focus on enhancing organizational staff proficiency through periodic training programs to keep them up to date with cutting-edge programming systems. In addition, forensic accountants should be trained to uphold professional ethical standards to conduct their work in an unbiased and independent manner. Besides, forensic accountants should be trained to develop a strong understanding of various investigative techniques and financial analysis tools, which can help them to identify and uncover fraudulent activities. Importantly, training programs should focus on enhancing the technical skills of forensic accountants, so that they can effectively analyze complex financial data.

The government should invest in the forensic accountants by giving them specific priority rights and all the materials that will make them acquire investigative skills needed to expose every kind of financial theft as well as to train the financial accountants to make them acquire better professional skills for financial analysis and make them uphold the quality of honesty and objectivity which will remove any emotional affiliation and inordinate interest in the outcome of any litigation. Policymakers should prioritize the establishment of strong legal frameworks that facilitate the utilization of sophisticated technologies in forensic accounting, while also safeguarding data privacy and upholding ethical norms. Global efforts to combat digital financial fraud can be greatly enhanced through international cooperation and the establishment of standardized processes.

The current study’s findings also showed how important MCBMI is, since it was found to considerably and positively increase the influence of DFA on ACIN. Therefore, it was urged to all managers in SMEs to implement effective tactics in line with organizational quirks to develop their business model in line with the circular economy. More importantly, to overcome the barriers to access and operability in metaverse environment, all SME managers should focus on creating the appropriate digital and physical adaption mechanisms. As such, the SME must do an adequate resource analysis in order to assess the necessary investment for the development of the strategy in the new environment. This would raise the likelihood of its implementation in the metaverse succeeding. This research emphasizes the need for public policies that are suited to the environment of SME. This would suggest that the various policies and strategies used by government should attempt to lessen the negative economic effects on SMEs and the costs related to the adoption of new technologies. Hardware and software makers as well as retailers are requested to gain their understanding on the advantages and drawbacks of the Metaverse in order to produce more cutting-edge systems that are appropriate for the quirks of SMEs.

6.2. Limitations and orientation for future research

Even though it highlighted notable results, the current academic effort in a new field of study ran into a number of unavoidable restrictions. However, the limits described might provide the impetus for the creation of new paths for future efforts. To begin, it is important to exercise caution when drawing broad conclusions from research, as the specific characteristics of the study setting may restrict the validity of conclusions derived from observations. Given that all the samples were from Vietnam, it is necessary to conduct further cross-regional examinations in order to validate the findings before they can be applied universally. Collecting extra data from both developed and emerging economies can provide a more comprehensive understanding of the subject. To enhance the usefulness of these findings, follow-up researchers are advised to carry out comparative studies between emerging and developed nations. The statistical data in this study primarily relied on a self-report design. Consequently, only one individual per SME was provided with survey questionnaires. The presence of a positive attitude in individuals may lead to a higher likelihood of them completing and returning their survey forms, therefore potentially introducing bias in the input provided by a single participant. Hence, forthcoming research endeavors should consider collecting the viewpoints of additional relevant stakeholders within this particular situation. The study’s generalizability may be affected by the third bottleneck, which arose from the utilization of snowball sampling approaches. Future research suggests that the utilization of quota sampling is essential for gathering sample data in order to ensure that the obtained results are both representative and scientifically valid. The study’s limited sample size, necessitating more research to verify the reliability of the findings presented in this work, constituted its fourth limitation. Furthermore, it is suggested that additional follow-up studies should be conducted to depict a more precise depiction of the interrelationship between DFA and ACIN. Sixthly, longitudinal studies are suggested for further research into the same factors over an extended period of time. Last but not least, the definition of MCBMI was based on a semantic amalgamation of theoretical components and illustrative descriptions that were attained from the literature. However, several in-depth investigations are urged to extend the linked constructs and use them in order to establish a more robust and rigorous interpretation of MCBMI.

Author contributions

P.Q.H. established the conception and design of the research. P.Q.H and V.K.P. conducted the data acquisition, analysis and interpretation. P.Q.H. prepared the drafted paper. P.Q.H. provided vital revision of the paper. P.Q.H. offered final approval of the version to publish. P.Q.H. was accountable for the accuracy or integrity of any part of the work. The other parts have had same contributions by all authors. In addition, all authors have read and made the final approval to the published version of the manuscript.

Disclosure statement

All authors have no conflict of interest for this research. Moreover, two authors whose names are listed immediately above certify that they have NO affiliations with or involvement in any organization or entity with any financial interest (such as honoraria; educational grants; participation in speakers’ bureaus; membership, employment, consultancies, stock ownership, or other equity interest; and expert testimony or patent-licensing arrangements), or non-financial interest (such as personal or professional relationships, affiliations, knowledge or beliefs) in the subject matter or materials discussed in this manuscript.

Data availability statement

Not applicable

Additional information

Funding

Notes on contributors

Quang Huy Pham

Quang Huy Pham is an Advanced Lecturer in Public Sector Accounting at the School of Accounting, University of Economics Ho Chi Minh City, Vietnam. He has authored several chapters for books, contributed to a multitude of scholarly journals, and delivered speeches at conferences both domestically and internationally.

Kien Phuc Vu

Kien Phuc Vu is a lecturer at University of Economics Ho Chi Minh City, Vinh Long Campus in Vietnam, where she is affiliated with Faculty of Accounting. Her primary research interests lie in the accounting and management fields. She published a number of articles and conducted paper for international conferences.

References

- Adomako, S., & Nguyen, N. P. (2023). Digitalization, inter-organizational collaboration, and technology transfer. The Journal of Technology Transfer, 1–24. https://doi.org/10.1007/s10961-023-10031-z

- Akinbowale, O. E., Mashigo, P., & Zerihun, M. F. (2023). The integration of forensic accounting and big data technology frameworks for internal fraud mitigation in the banking industry. Cogent Business & Management, 10(1), 1–22. https://doi.org/10.1080/23311975.2022.2163560

- Akinwale, O. E., & Onokala, U. C. (2022). Leadership and power dynamics in crisis management: a brain-drain effect – the Trump and US experience. LBS Journal of Management & Research, 20(1/2), 57–72. https://doi.org/10.1108/LBSJMR-05-2022-0008

- Ali Qalati, S., Li, W., Ahmed, N., Ali Mirani, M., & Khan, A. (2020). Examining the factors affecting sme performance: The mediating role of social media adoption. Sustainability, 13(1), 75. https://doi.org/10.3390/su13010075

- Ali, A., Razak, S. A., Othman, S. H., Eisa, T. A. E., Al-Dhaqm, A., Nasser, M., Elhassan, T., Elshafie, H., & Saif, A. (2022). Financial fraud detection based on machine learning: A systematic literature review. Applied Sciences, 12(19), 9637. https://doi.org/10.3390/app12199637

- Alzoubi, A. B. (2023). Maximizing internal control effectiveness: the synergy between forensic accounting and corporate governance. Journal of Financial Reporting and Accounting, 1–13. https://doi.org/10.1108/JFRA-03-2023-0140

- Anwar, M., Scheffler, M., & Clauss, T. (2024). Digital capabilities, their role in business model innovativeness, and the internationalization of SMEs. IEEE Transactions on Engineering Management, 71, 4131–4143. https://doi.org/10.1109/TEM.2022.3229049

- Arnold, M. G., Pfaff, C., & Pfaff, T. (2023). Circular business model strategies progressing sustainability in the German textile manufacturing industry. Sustainability, 15(5), 4595. https://doi.org/10.3390/su15054595

- Arshad, M. Z., Arshad, D., Lamsali, H., Alshuaibi, A. S. I., Alshuaibi, M. S. I., Albashar, G., Shakoor, A., & Chuah, L. F. (2023). Strategic resources alignment for sustainability: The impact of innovation capability and intellectual capital on SME’s performance. Moderating role of external environment. Journal of Cleaner Production, 417, 137884. https://doi.org/10.1016/j.jclepro.2023.137884

- Attig, N., Boubakri, N., El Ghoul, S., & Guedhami, O. (2016). Firm internationalization and corporate social responsibility. Journal of Business Ethics, 134(2), 171–197. https://doi.org/10.1007/s10551-014-2410-6

- Awodiran, M. A., Ogundele, A. T., Idem, U. J., Anwana., & Emem, O. (2023 Digital Forensic Accounting and Cyber Fraud in Nigeria [Paper presentation]. 2023 International Conference on Cyber Management and Engineering (CyMaEn) (pp. 1–6). https://doi.org/10.1109/CyMaEn57228.2023.10050992

- Ayob, A. H., Ramlee, S., & Abdul Rahman, A. (2015). Financial factors and export behavior of small and medium-sized enterprises in an emerging economy. Journal of International Entrepreneurship, 13(1), 49–66. https://doi.org/10.1007/s10843-014-0141-5

- Bai, W., Johanson, M., Oliveira, L., & Ratajczak-Mrozek, M. (2021). The role of business and social networks in the effectual internationalization: Insights from emerging market SMEs. Journal of Business Research, 129, 96–109. https://doi.org/10.1016/j.jbusres.2021.02.042

- Bakos, J., Siu, M., Orengo, A., & Kasiri, N. (2020). An analysis of environmental sustainability in small & medium-sized enterprises: Patterns and trends. Business Strategy and the Environment, 29(3), 1285–1296. https://doi.org/10.1002/bse.2433

- Barquet, A. P., Seidel, J., Seliger, G., & Kohl, H. (2016). Sustainability Factors for PSS Business Models. Procedia CIRP, 47, 436–441. https://doi.org/10.1016/j.procir.2016.03.021

- Bartolacci, F., Caputo, A., & Soverchia, M. (2020). Sustainability and financial performance of small and medium sized enterprises: A bibliometric and systematic literature review. Business Strategy and the Environment, 29(3), 1297–1309. https://doi.org/10.1002/bse.2434

- Bashir, M., Alfalih, A., & Pradhan, S. (2023). Managerial ties, business model innovation & SME performance: Moderating role of environmental turbulence. Journal of Innovation & Knowledge, 8(1), 100329. https://doi.org/10.1016/j.jik.2023.100329

- Blomsma, F., & Brennan, G. (2017). The emergence of circular economy: A new framing around prolonging resource productivity. Journal of Industrial Ecology, 21(3), 603–614. https://doi.org/10.1111/jiec.12603

- Bocken, N. M. P., de Pauw, I., Bakker, C., & van der Grinten, B. (2016). Product design and business model strategies for a circular economy. Journal of Industrial and Production Engineering, 33(5), 308–320. https://doi.org/10.1080/21681015.2016.1172124

- Boulos, M., & Burden, D. (2007). Web GIS in practice V: 3-D interactive and real-time mapping in Second Life. International Journal of Health Geographics, 6(1), 51. https://doi.org/10.1186/1476-072x-6-51

- Boumediene, S., & Boumediene, S. (2023). Electronic Evidence: A Framework for Applying Digital Forensics to Data Base. Journal of Forensic Accounting Research, 8(1), 266–286. https://doi.org/10.2308/JFAR-2022-006

- Brillinger, A.-S., Els, C., Schäfer, B., & Bender, B. (2020). Business model risk and uncertainty factors: Toward building and maintaining profitable and sustainable business models. Business Horizons, 63(1), 121–130. https://doi.org/10.1016/j.bushor.2019.09.009

- Burns, N., & Grove, S. K. (2009). The Practice of Nursing Research: Appraisal, Synthesis, and Generation of Evidence (6th ed.). Saunders Elsevier.

- Calzadilla, A. C. G., Villarreal, M. S., Jerónimo, J. M. R., & López, R. F. (2022). Risk management in the internationalization of small and medium-sized Spanish companies. Journal of Risk and Financial Management, 15(361), 1–21. https://doi.org/10.3390/jrfm15080361

- Caputo, F., Fiano, F., Riso, T., Romano, M., & Maalaoui, A. (2022). Digital platforms and international performance of Italian SMEs: an exploitation-based overview. International Marketing Review, 39(3), 568–585. https://doi.org/10.1108/IMR-02-2021-0102

- Carvalho, N., Chaim, O., Cazarini, E., & Gerolamo, M. (2018). Manufacturing in the fourth industrial revolution: A positive prospect in Sustainable Manufacturing. Procedia Manufacturing, 21, 671–678. https://doi.org/10.1016/j.promfg.2018.02.170

- Casillas, J. C., & Moreno-Menéndez, A. M. (2014). Speed of the internationalization process: The role of diversity and depth in experiential learning. Journal of International Business Studies, 45(1), 85–101. https://doi.org/10.1057/jibs.2013.29

- Chebbi, H., Ben Selma, M., Bouzinab, K., Papadopoulos, A., Labouze, A., & Desmarteau, R. (2023). Accelerated internationalization of SMEs and microfoundations of dynamic capabilities: towards an integrated conceptual framework. Review of International Business and Strategy, 33(1), 35–54. https://doi.org/10.1108/RIBS-12-2021-0174

- Christofi, M., Iaia, L., Marchesani, F., & Masciarelli, F. (2021). Marketing innovation and internationalization in smart city development: a systematic review, framework and research agenda. International Marketing Review, 38(5), 948–984. https://doi.org/10.1108/IMR-01-2021-0027

- Cole, R., Stevenson, M., & Aitken, J. (2019). Blockchain technology: implications for operations and supply chain management. Supply Chain Management: An International Journal, 24(4), 469–483. https://doi.org/10.1108/SCM-09-2018-0309

- Corvellec, H., Stowell, A. F., & Johansson, N. (2022). Critiques of the circular economy. Journal of Industrial Ecology, 26(2), 421–432. https://doi.org/10.1111/jiec.13187

- Coudounaris, D. N. (2021). The internationalisation process of UK SMEs: exporting and non-exporting behaviours based on a four forces behavioural model. Review of International Business and Strategy, 31(2), 217–256. https://doi.org/10.1108/RIBS-06-2019-0075

- Dam, N. A. K., Le Dinh, T., & Menvielle, W. (2019). A systematic literature review of big data adoption in internationalization. Journal of Marketing Analytics, 7(3), 182–195. https://doi.org/10.1057/s41270-019-00054-7

- De Giovanni, P. (2023). Sustainability of the Metaverse: A Transition to Industry 5.0. Sustainability, 15(7), 6079. https://doi.org/10.3390/su15076079

- Deng, X., & Yu, Z. (2023). An extended hedonic motivation adoption model of TikTok in higher education. Education and Information Technologies, 28, 13595–13617. https://doi.org/10.1007/s10639-023-11749-x

- Denicolai, S., Zucchella, A., & Magnani, G. (2021). Internationalization, digitalization, and sustainability: Are SMEs ready? A survey on synergies and substituting effects among growth paths. Technological Forecasting and Social Change, 166, 120650. https://doi.org/10.1016/j.techfore.2021.120650

- Dolata, M., & Schwabe, G. (2023). What is the Metaverse and who seeks to define it? Mapping the site of social construction. Journal of Information Technology, 38(3), 239–266. https://doi.org/10.1177/02683962231159927

- Dubey, V., Mokashi, A., Pradhan, S. R., Gupta, P., & Walimbe, R. (2022). Metaverse and banking industry – 2023 the year of metaverse adoption. Technium: Romanian Journal of Applied Sciences and Technology, 4(10), 62–73. https://doi.org/10.47577/technium.v4i10.7774

- Dulia, E. F., Ali, S. M., Garshasbi, M., & Kabir, G. (2021). Admitting risks towards circular economy practices and strategies: An empirical test from supply chain perspective. Journal of Cleaner Production, 317, 128420. https://doi.org/10.1016/j.jclepro.2021.128420

- Dwivedi, Y. K., Hughes, L., Baabdullah, A. M., Ribeiro-Navarrete, S., Giannakis, M., Al-Debei, M. M., Dennehy, D., Metri, B., Buhalis, D., Cheung, C. M. K., Conboy, K., Doyle, R., Dubey, R., Dutot, V., Felix, R., Goyal, D. P., Gustafsson, A., Hinsch, C., Jebabli, I., … Wamba, S. F. (2022). Metaverse beyond the hype: Multidisciplinary perspectives on emerging challenges, opportunities, and agenda for research, practice and policy. International Journal of Information Management, 66, 102542. https://doi.org/10.1016/j.ijinfomgt.2022.102542

- Elkaseh, A. M., Wong, K. W., & Fung, C. C, Murdoch University, Australia. (2016). perceived ease of use and perceived usefulness of social media for e-learning in libyan higher education: A structural equation modeling analysis. International Journal of Information and Education Technology, 6(3), 192–199. https://doi.org/10.7763/IJIET.2016.V6.683

- Ertz, M., Sun, S., Boily, E., Kubiat, P., & Quenum, G. G. Y. (2022). How transitioning to Industry 4.0 promotes circular product lifetimes. Industrial Marketing Management, 101, 125–140. https://doi.org/10.1016/j.indmarman.2021.11.014

- Evers, N., Ojala, A., Sousa, C. M., & Criado-Rialp, A. (2023). Unraveling business model innovation in firm internationalization: a systematic literature review and future research agenda. Journal of Business Research, 158, 113659. https://doi.org/10.1016/j.jbusres.2023.113659

- Farrell, A. M. (2010). Insufficient discriminant validity: A comment on Bove, Pervan, Beatty, and Shiu (2009). Journal of Business Research, 63(3), 324–327. https://doi.org/10.1016/j.jbusres.2009.05.003

- Feliciano-Cestero, M. M., Ameen, N., Kotabe, M., Paul, J., & Signoret, M. (2023). Is digital transformation threatened? A systematic literature review of the factors influencing firms’ digital transformation and internationalization. Journal of Business Research, 157, 113546. https://doi.org/10.1016/j.jbusres.2022.113546

- Ferasso, M., Beliaeva, T., Kraus, S., Clauss, T., & Ribeiro-Soriano, D. (2020). Circular economy business models: The state of research and avenues ahead. Business Strategy and the Environment, 29(8), 3006–3024. https://doi.org/10.1002/bse.2554

- Ferreira de Araújo Lima, P., Crema, M., & Verbano, C. (2020). Risk Management in SMEs: a systematic literature review and future directions. European Management Journal, 38(1), 78–94. https://doi.org/10.1016/j.emj.2019.06.005

- Fornell, C., & Larcker, D. F. (1981). Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Franke, G., & Sarstedt, M. (2019). Heuristics versus statistics in discriminant validity testing: a comparison of four procedures. Internet Research, 29(3), 430–447. https://doi.org/10.1108/IntR-12-2017-0515

- Freeman, S., Edwards, R., & Schroder, B. (2006). How Smaller Born-Global Firms Use Networks and Alliances to Overcome Constraints to Rapid Internationalization. Journal of International Marketing, 14(3), 33–63. https://doi.org/10.1509/jimk.14.3.33

- Freeman, S., Hutchings, K., Lazaris, M., & Zyngier, S. (2010). A model of rapid knowledge development: The smaller born-global firm. International Business Review, 19(1), 70–84. https://doi.org/10.1016/j.ibusrev.2009.09.004

- Garanina, T., Ranta, M., & Dumay, J. (2022). Blockchain in accounting research: current trends and emerging topics. Accounting, Auditing & Accountability Journal, 35(7), 1507–1533. https://doi.org/10.1108/AAAJ-10-2020-4991

- Gauttier, S., Simouri, W., & Milliat, A. (2022). When to enter the metaverse: business leaders offer perspectives. Journal of Business Strategy, 45(1), 2–9. https://doi.org/10.1108/JBS-08-2022-0149

- Gnizy, I. (2019). Big data and its strategic path to value in international firms. International Marketing Review, 36(3), 318–341. https://doi.org/10.1108/IMR-09-2018-0249

- Govindan, K., & Hasanagic, M. (2018). A systematic review on drivers, barriers, and practices towards circular economy: a supply chain perspective. International Journal of Production Research, 56(1-2), 278–311. https://doi.org/10.1080/00207543.2017.1402141

- Grazzini, L., Acuti, D., & Aiello, G. (2021). Solving the puzzle of sustainable fashion consumption: the role of consumers’ implicit attitudes and perceived warmth. Journal of Cleaner Production, 287, 125579. https://doi.org/10.1016/j.jclepro.2020.125579

- Guldmann, E., & Huulgaard, R. D. (2020). Barriers to circular business model innovation: A multiple-case study. Journal of Cleaner Production, 243, 118160. https://doi.org/10.1016/j.jclepro.2019.118160