Abstract

This article presents the systematic literature review (SLR) of accountability of pondok pesantren (Islamic boarding school). The purpose is to provide a review of the existing literature (theoretical/empirical) on the accountability of pondok pesantren and to analyze the future agenda of research. By using the Publish or Perish application, 200 units of initial article data were obtained for further analysis. The results showed that there were few reputable international journal articles (indexed by Scopus) that published articles on the topic of pondok pesantren accountability and focused more on financial management. The other related topics are accounting and financial reports, governance and accountability in Islamic organizations. The qualitative research method was more used and shows that accountability of pondok pesantren applied double accountability (responsibility to God and to others). Furthermore, it was found that the relevance of accountability for pondok pesantren with local cultural values other than Islamic values as a basis. In addition, the theory that was often used as a basis for accountability of pondok pesantren was legitimacy theory. The topics for the future research agenda on accountability of pondok pesantren is accountability of asset management and analysis the determinant of pondok pesantren accountability.

1. Introduction

Accountability of pondok pesantren (Islamic boarding school) is an interesting topic to study. Pondok pesantren are unique Islamic educational institutions and seem to be managed traditionally. However, pondok pesantren have developed in variety and form. Accountability is becoming increasingly necessary to increase legitimacy and public trust. Accountability shows a condition for assessing the quality of performance of a person’s responsibility (Murdayanti & Puruwita, Citation2017). Accountability can explain the relationship between two parties internally and externally. Internal relationships show a person’s accountability to God. Meanwhile, external accountability refers to horizontal responsibility, to humans and the environment.

Pondok pesantren are unique Islamic educational institutions and have indigenous Indonesian values (Arifin & Anisah, Citation2019). The presence of pondok pesantren has a big influence on moral formation and educational development (Suaidah & Rohmatillah, Citation2022). Pondok pesantren have been present in Indonesia to advance Islam and were formed by ulama including Walisongo, as a medium for spreading Islam in Java in particular (Susilo & Wulansari, Citation2020). Pondok pesantren have contributed to the progress of education in Indonesia. Data released on the satudata.kemenag.go.id website show that in 2022 there will be 38,927 pondok pesantren in Indonesia with 4,495,782 students (EMIS Data Update 8 November 2022).

The development of pondok pesantren is increasingly dynamic along with developments in information technology and science. Islamic boarding school services are increasing by providing general education besides religious education (Setyawan, Citation2019). Currently, there are three typologies of pondok pesantren in their development, namely salaf, modern and convergence of salaf and modern (Nihwan & Paisun, Citation2019). The presence of Law Number 18 of 2019 concerning pondok pesantren further emphasizes the government’s recognition of the existence of pondok pesantren. This law is a new history in the development of pondok pesantren in Indonesia (Panut, Giyoto, & Rohmadi, Citation2021). The law also demands that Islamic boarding school management be more accountable and transparent.

Several cases occurred related to the management of pondok pesantren in Indonesia. The big case that hit the caretaker of the Pondok Pesantren Al Zaytun in West Java impacted transferring assets owned by pondok pesantren (liputan6.com, 5 November 2023). The former head of Pondok Pesantren Al-Munawaroh was arrested for allegedly embezzling savings funds from Pondok Pesantren Al-Munawaroh students in Sungai Misang, Bangko Village, Jambi (JPNN.com, 20 November 2023). Apart from that, there are allegations of corruption in pondok pesantren grant funds, so the prosecutor’s office searches the warehouse of the Banten Welfare Bureau regarding these allegations (Kompas.com, 19 April 2021). This phenomenon provides an understanding that there is no right in the financial management of pondok pesantren.

Based on the description of the phenomena, research on the accountability of pondok pesantren is becoming increasingly important to conduct as empirical studies that examine accountability practices in pondok pesantren. Previous research has been found that attempts to reveal the accountability practices of pondok pesantren from quite diverse perspectives. This research aims to analyze the development of research regarding pondok pesantren accountability using a systematic literature review (SLR) approach. In this way, a more comprehensive analysis of pondok pesantren accountability practices and future research agendas can be performed.

2. Literature review

2.1. The concept of accountability and Islam

Over the past decade, accountability has acquired attention in a variety of fields including law, political science and public administration (Lindberg, Citation2013). The concept of accountability has become increasingly prominent in recent years, with various subtypes emerging, such as high stakes accountability, staff/system accountability, in-process accountability and no accountability (Ford & Ihrke, Citation2017). However, there are differences in the interpretation and application of accountability because standards of accountable behavior vary across roles, times, places and individuals (Bovens, Citation2007). The concept of accountability will continue to develop with various discussions regarding its limitations and implications (Mulgan, Citation2000).

Accountability is often linked to responsibility, which involves recognizing obligations within a particular role and moral framework (Plaisance, Citation2000). The concept of accountability is also linked to mechanisms that make powerful institutions responsive to the public, underscoring their role in ensuring transparency and responsiveness (Bovens, Citation2010). Accountability refers to a relationship in which people explain and take responsibility for their actions (Roberts & Scapens, Citation1985). Accountability is a multidisciplinary concept which explains that accountability is viewed differently by people based on their training and orientation (Gidado & Yusha’u, Citation2017). Accountability relates to a person’s responsibility to the person giving responsibility by creating performance. Additionally, accountability goes beyond traditional institutional frameworks, as seen in discussions regarding spiritual accountability in organizations such as churches (Kambey, Citation2021).

Sufficient theories in accounting attempt to explain the concept of accountability. The concept of accountability in accounting includes sufficient relationships between financial and operational items, including non-financial ones. Therefore, organizational performance and responsibility are more comprehensive, covering both financial and non-financial (Joannidès & Berland, Citation2008). Accountability reflects social reality and is aimed at understanding the contribution of accounting to the construction of social and organizational contexts (Lukka & Vinnari, Citation2014). Within the framework of various theories (stakeholder theory, legitimacy theory, etc.), accountability also includes sustainability reporting which includes ethical and social dimensions besides financial (Miles, Citation2019). Thus, the scope of accountability becomes broader and more comprehensive.

Accountability is related to sufficient areas such as health service management (Bakalikwira, Bananuka, Kaawaase Kigongo, Musimenta, & Mukyala, Citation2017), government institutions (Sofyani, Riyadh, & Fahlevi, Citation2020) and educational institutions (Ford & Ihrke, Citation2017). Using agency and stewardship theory, accountability in the health sector is significantly influenced by governance structure and managerial competence (Bakalikwira et al., Citation2017). Accountability is needed to create quality health service delivery and health governance (Abor & Tetteh, Citation2023). Accountability in local government institutions is significantly influenced by the effectiveness of information technology governance (Sofyani et al., Citation2020). Public accountability is significant because it will improve organizational performance (Tran & Nguyen, Citation2020). Apart from that, accountability can also increase community trust in the village government context (Pratolo, Sofyani, & Maulidini, Citation2022).

Accountability in Islam is closely related to Islamic teachings regarding the concept of monotheism, which views Allah as the only God and Muhammad as His messenger. Thus, Allah is the source of truth and the goal of the universe (Al Faruqi, Citation1982). Another opinion explains that accountability in Islam is dual. A person is responsible to Allah and to others (Gidado & Yusha’u, Citation2017). Various verses in the Koran explain the importance of accountability. One of them is QS Al Baqarah verses 282–284, which emphasizes that accounting, accountability and transparency are prescribed by Allah subhanahu wa ta’ala (Waluya & Mulauddin, Citation2021).

2.2. Accountability of pondok pesantren

Article 1 and Article 4 of the Pondok Pesantren Law explain that pondok pesantren can also be called dayah, surau, meunasah. Pondok pesantren is a community-based institution established by individuals, foundations, Islamic community organizations and/or communities that instill faith and devotion to Allah SWT, instill noble morals and uphold the Islamic teachings of rahmatan lil’alamin as reflected in their attitude. Humility, tolerance, balance, moderation and other noble values of the Indonesian nation through education, Islamic preaching, example, and community empowerment within the framework of the Unitary State of the Republic of Indonesia. The scope of Islamic boarding school functions includes education, da’wah and community empowerment.

Pondok pesantren consists of; pondok pesantren that provide education as studying the Yellow Book; pondok pesantren that provide education as Dirasah Islamiah with the Muallimin Education Pattern; or pondok pesantren that provide education in other forms that are integrated with general education. Judging from the type of management, pondok pesantren can be classified into two, namely traditional pondok pesantren and modern pondok pesantren (Rodiah et al., Citation2020).

Accountability is a manifestation of implementing Islamic education that implements good governance (Ja’far & Munawir, Citation2018). Pondok pesantren in the modern era are required to realize integrative accountability from a world perspective and an afterlife perspective (Handayani, Ludigdo, Rosidi, & Roekhudin, Citation2022). Accountability is transparency in financial management (Murdayanti & Puruwita, Citation2017). Thus, pondok pesantren should currently implement accountability practices as a form of better management and under the mandate of the law.

The previous explanation shows that accountability in Islam refers to the concept of double accountability, namely accountability to God (hablum minallah) and accountability to others (hablum minannas). In pondok pesantren, all parties in pondok pesantren should consciously be able to take responsibility for their activities under God’s commands (syariah) and socially and morally. Accountability to Allah is realized by performing worship and activities under religious teachings. Performing activities as a pondok pesantren may not conduct actions that are contrary to Islamic teachings such as acts of corruption, dishonesty and others. Apart from that, he must not commit acts of cheating, lying or injustice towards other members of the pondok pesantren. He must behave well towards other people. This is under the explanation from the Al Quran Surah Al-Hujurat (49:10) which emphasizes that believers are brothers. Thus, every time someone performs an activity at a pondok pesantren, they will try to do their best because it will be assessed by Allah as worship and recorded as a good deed towards others.

The parties who should practice accountability in pondok pesantren are all existing parties, including kiai, ustadz council, managements, students and others. Parents or guardians of students are also responsible for realizing pondok pesantren accountability with their respective roles and responsibilities. As a kiai, he has greater responsibilities because pondok pesantren are a medium for education and a medium for da’wah to spread Islamic values to society. As a manager, he must perform his mandate and possibly so that the Islamic boarding school’s operations can run well. As an Ustadz, he imparts knowledge, being a role model for students, and developing knowledge. As a santri, he continues to learn about religious knowledge, morals and developing other competencies. As a student’s parent, he provides full support for the administration and what his child needs in studying at the pondok pesantren. Other parties contribute according to their respective roles. If various parties can carry out their respective responsibilities well, then accountability of pondok pesantren will be created and implemented better under the teachings of the Islamic religion.

Previous studies showed the accounting and accountability practices of pondok pesantren in Indonesia in particular. Accounting practices in pondok pesantren are still underdeveloped and financial accountability showed by management is still not in line with community expectations (Basri & Siti-Nabiha, Citation2016). Another opinion stated that accounting practices are only rhetoric and only have a minimal impact in creating accountability (Mzenzi, Citation2023). Accountability is not yet an important thing that must be realized (Rodiah et al., Citation2020). Another study showed the weak response of pondok pesantren in compiling and reporting financial reports as expected by the government because of various contributing factors (Handayani, Ludigdo, Rosidi, & Roekhudin, Citation2021). The diverse conditions and culture of pondok pesantren are two important factors that determine this phenomenon. Pondok pesantren are unique because of the diversity of books studied, the schools adhered to, the area where the pondok pesantren is located, and including Kiai as the main leaders in the pondok pesantren.

Another study explains several factors that can determine the accountability of pondok pesantren. The financial competence of human resources is a significant factor that can determine the accountability of pondok pesantren (Murdayanti & Puruwita, Citation2019). Apart from that, pondok pesantren leadership factors are also another significant contributor (Alfani, Harmain, & Syahriza, Citation2023). Other researchers have proven that the existence of accounting standards can also increase the accountability of pondok pesantren (Yuliani & Mustofa, Citation2022). Thus, pondok pesantren accountability will be better if it has competent resources, supportive leadership and adhered to accounting guidelines.

This research seeks to explore research that analyzes and explains the accountability practices of pondok pesantren. Pondok pesantren that develop in Indonesia take various forms. Accounting practices and accountability will also be impacted indirectly.

3. Research method

The research method used was the SLR method. SLR research is a research method that aims to evaluate, identify and analyze all previous research results that are related and relevant to a particular topic, particular research or current phenomenon of concern (Perry & Hammond, Citation2002). The SLR research stages conducted include planning research questions, systematically searching for literature reviews, filtering and selecting appropriate research articles, conducting analysis and synthesis of qualitative findings, implementing quality control and preparing the final report. Alhossini, Ntim, and Zalata (Citation2021) and Alatawi, Ntim, Zras, and Elmagrhi (Citation2023) adapted from previous studies to develop the SLR approach the stages are defined review aims and questions, develop review techniques, literature search, data extraction and synthesize results. Nguyen, Ntim, and Malagila (Citation2020) also develop three-step approach to SLR adopted from previous studies including sources/database, sampling of studies for review and thematic analysis of sampled studies. There are four steps can be conducted for SLR; identification of the resources, search by the keywords, excluding and including, and analysis the results (Lu, Ntim, Zhang, & Li, Citation2022). Ibrahim, Hussainey, Nawaz, Ntim, and Elamer (Citation2022) developed SLR analysis by conducting three steps including planning a review, performing a review and reporting and dissemination.

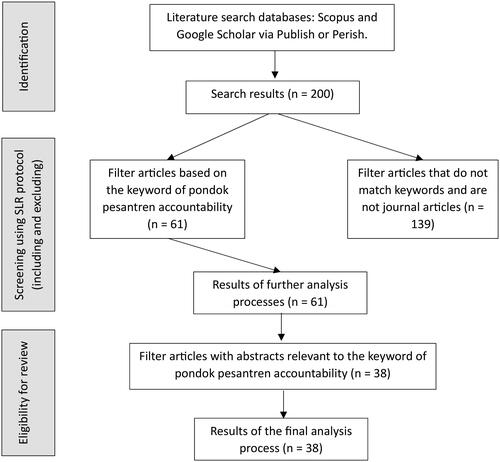

The PRISMA model (Preferred Reporting Items for Systematic Reviews and Meta-Analysis) was used in this SLR research (Moher, Liberati, Tetzlaff, Altman, & PRISMA Group, Citation2009). shows the research flow in the PRISMA model by adopting model from previous studies (Alatawi et al., Citation2023; Wolor, Nurkhin, & Citriadin, Citation2021). Using the Google Scholar and Scopus databases (using the Publish or Perish application) data were obtained for 200 articles relevant to the topic of Islamic boarding school accountability. The context of pondok pesantren is very limited in international studies so that the Scopus database cannot provide adequate sources. The Google Scholar database is important in this research and can provide a sufficient database for further analysis.

Figure 1. PRISMA search for relevant journal articles.

This SLR research procedure refers to previous studies (Alatawi et al., Citation2023; Wolor et al., Citation2021) which includes preparing background and objectives, formulating research questions, searching literature, determining selection criteria for the data found, data extraction strategies, assessing the quality of primary studies and data synthesis. The source of SLR research questions is from the research purposes by using the results of filtering the articles. Thus, the formulation of this SLR research question is:

How is the profile of publications on the topic of accountability in pondok pesantren?

How is the comparison of the methods and results of research that examines the accountability of pondok pesantren?

What relevant topics are related to the topic of pondok pesantren accountability?

What is the future research agenda related to the topic of pondok pesantren accountability?

We used the Scopus database for searching the article on accountability of pondok pesantren and the result showed that there is limited article by using keyword ‘accountability and pondok pesantren’ and ‘accountability and Islamic boarding school’. Pondok pesantren is unique and most in Indonesia, so few researchers have published their research findings on pondok pesantren in Scopus indexed journals. Then we used the publish and perish application to find more articles that explored the accountability of pondok pesantren. We used 200 articles for the initial selection year from 2011 until 2023.

In the article selection stage, in the first stage, 61 articles were obtained which were most relevant to the keywords. Various articles were less relevant because they discussed topics related to pondok pesantren financial management, non-financial accountability, waqf and other topics. In addition, many articles were thesis manuscripts, theses, service journal articles and not journal articles based on research results. In the second selection stage, 38 articles were obtained after analyzing the abstracts of the article base obtained. Of the 38 articles, there were 21 articles that were very relevant regarding pondok pesantren accountability, 11 articles that examined pondok pesantren accounting, four articles that discussed the topic of pondok pesantren governance and two articles that analyzed accountability in Islamic organizations.

4. Results and discussion

4.1. Publication profile (journal article) on the topic of pondok pesantren accountability

The research results shown in described the profile of publications (journal articles) that discussed the accountability of pondok pesantren. There were 38 journal articles which were further analyzed in this SLR article. There were four sub-topics that applied to pondok pesantren accountability, namely accountability of pondok pesantren financial management, pondok pesantren accounting, pondok pesantren governance and accountability in Islamic organizations. indicates that there was no dominant author researching the accountability of pondok pesantren financial management. Basri is the author who most often studied accountability with a qualitative approach. His writing was also the most cited article. Twenty citations for articles regarding accountability in pondok pesantren financial management and 81 citations for articles discussing accountability in Islamic organizations.

Table 1. Publication profile (journal article) on the topic of pondok pesantren accountability.

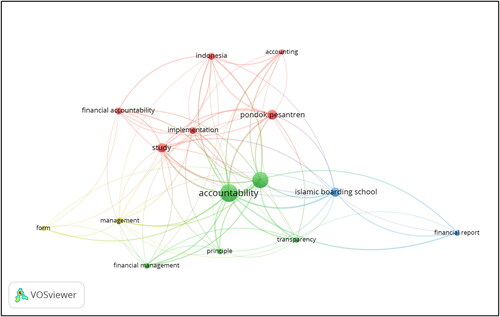

also shows the profile of previous research regarding accountability of pondok pesantren using the VOSViewer application. There were three big topics including accountability, pondok pesantren and Islamic boarding school. The relationship between several research topics regarding pondok pesantren accountability also did not appear to be too dominant on certain topics. Pondok pesantren accountability was often associated with financial accountability, financial management, accounting, financial reporting, transparency and others. The relationship line also showed that there were still possibilities for further research such as the topic of form, principles, and so on.

Figure 2. Analysis of the research profile of pondok pesantren accountability using VOSviewer.

4.2. The comparison of methods and results of research that qualitatively examines the accountability of pondok pesantren

describes the comparison of methods and results of research that qualitatively examined the accountability of pondok pesantren. There were various qualitative research approaches used by researchers, including case studies, interpretive, grounded theory and phenomenology. Qualitative descriptive methods were also used to reveal phenomena related to accountability practices in pondok pesantren. The data collection methods used were relatively the same, namely interviews, documentation and observation. The interview method was developed into structured interviews and in-depth interviews. The triangulation method was used to test the validity of the data.

Table 2. Comparison of methods and results of articles on accountability of pondok pesantren with qualitative methods.

The topic of pondok pesantren accountability was quite diverse in terms used. The terms pondok pesantren accountability, pondok pesantren financial accountability and pondok pesantren financial management accountability were found. Measurements and meanings became more diverse. There were authors who used meaning in the tafakkur method (Gafur et al., Citation2021); an interesting method for understanding the deep meaning of accountability in pondok pesantren. Numerous authors linked accountability with Islamic values such as being based on trust and the framework of amar ma’ruf nahi munkar (Firdausi & Al Amin, Citation2021; Gafur et al., Citation2021; Handayani et al., Citation2022; Wirawan, Citation2019). In addition, accountability practices in pondok pesantren could not be separated from accounting practices, which were still considered weak and not under applicable guidelines (Baehaqi et al., Citation2021; Basri & Siti-Nabiha, Citation2016; Hanifah et al., Citation2022; Murdayanti & Puruwita, Citation2017).

A comparison of research methods and results that quantitatively examined the accountability of pondok pesantren is shown in . There were variations on the topic of pondok pesantren accountability, such as pondok pesantren financial accountability, pondok pesantren financial reporting accountability, and pondok pesantren accountability. The multiple linear analysis method was more often used to analyze the influence of independent variables on pondok pesantren accountability. The independent variables tested included financial HR competency (Burhan et al., Citation2023; Dewi et al., Citation2021; Murdayanti & Puruwita, Citation2019; Yuliani & Mustofa, Citation2022), trust and leadership (Alfani et al., Citation2023), accounting guidelines (Yuliani & Mustofa, Citation2022), understanding pondok pesantren accounting and pondok pesantren accounting training (Burhan et al., Citation2023) and the use of technology (Naz’aina et al., Citation2022). HR competency was an independent variable that was often analyzed with mixed results. Meanwhile, other variables were proven to have a significant influence on the accountability of pondok pesantren. It has been proven that the use of technology could not affect accountability.

Table 3. Comparison of methods and results of articles on accountability of pondok pesantren with quantitative methods.

4.3. Relevant topics related to the topic of accountability of pondok pesantren

Previous research also examined several relevant and interesting topics such as implementing pondok pesantren accounting, pondok pesantren governance and accountability in Islamic organizations. The research methods used were quite diverse, both quantitative and qualitative methods. Implementation of pondok pesantren accounting guidelines and PSAK (Statement of Financial Accounting Standards) Number 45 was the basis for assessing the application of accounting in several pondok pesantren. The Modern Pondok Pesantren of Al-Manar Muhammadiyah had prepared financial reports but had not presented financial reports based on Pondok Pesantren Accounting Guidelines (Sahri et al., Citation2021). It was further revealed that pondok pesantren were limited in preparing their financial reports, namely reports on cash receipts and disbursements (Solikhah et al., Citation2019). The accounting medium used as accountability at the pondok pesantren of Nazhatut Thullab was a report on cash receipts and disbursements. Financial reports had also not been presented based on PSAK Number 45 concerning non-profit entities (Arifin, Citation2014). The financial report of the pondok pesantren of al Muthmainnah was incomplete and did not comply with the guidelines (Syukri et al., Citation2023). Thus, it can be stated that the quality of financial reports at pondok pesantren was still relatively low.

Other research examined the importance of accounting information systems (Akbar & Meirini, Citation2022) and analyzed the factors that influenced it (Murdayanti & Purwohedi, Citation2018). Strong support with showed higher involvement in project progress and provision of resources would improve the financial accounting system. Another study proved significant differences in the financial reporting practices of pondok pesantren in Indonesia and Malaysia, especially in accounting knowledge and use of information technology (Periansya et al., Citation2023). These two aspects were significant to improve by collaborating with other related parties such as Islamic financial institutions, education and training institutions, and universities.

Another relevant topic was governance. Pondok pesantren as educational institutions would implement distinctive governance, although they could not abandon the governance principles that had been recognized in business entities (Kurniawan et al., Citation2020). Apart from the principles of transparency, accountability, independence and fairness, pondok pesantren would apply other principles such as sharia supervision and adab or ethics. Another study showed that Pondok Pesantren Al-Fattah, Sidoarjo had implemented governance principles well. The development of pondok pesantren was getting better (Oktafia & Basith, Citation2017). In addition, Ma’had Al-Muqoddasah Litahfidhil Qur’an Ponorogo had implemented governance based on Islamic values well (Anggara & Faradisi, Citation2021). There were sufficient verses in the Koran as the basis for implementing good governance in pondok pesantren. QS. Al Baqarah verse 42 emphasizes the importance of accountability and QS. Al Imron verse 159 as the basis for the importance of transparency.

4.4. The future research agenda is related to the topic of accountability of pondok pesantren

The future research agenda on accountability of pondok pesantren is still interesting to study using various approaches and research methods. The topic is accountability in pondok pesantren asset management. This specific topic will review the phenomenon of asset management in pondok pesantren starting from planning to utilization and reporting. Another interesting topic is the relationship between variables that influence the accountability of pondok pesantren management quantitatively. Kiai’s central position in the pondok pesantren is undeniable. However, the creation of accountability in pondok pesantren is growing and requires attention from various parties to increase public trust in pondok pesantren. In addition, the application of governance based on Islamic values and local culture will provide interesting and more comprehensive studies, not limited to accountability.

5. Conclusion

This research sought to reveal findings regarding the accountability of pondok pesantren using a SLR approach. Based on data analysis (found articles) it can be explained that there were several relevant topics, namely accountability for financial management of pondok pesantren, accounting and financial reports for pondok pesantren, governance of pondok pesantren and accountability in Islamic organizations. Research on pondok pesantren accountability mostly used qualitative methods with various approaches such as phenomenology, case studies, interpretive and grounded theory. Accountability in pondok pesantren could not be separated from accounting practices by applying Islamic principles such as trust, honesty, amar ma’ruf nahi munkar. The accountability of pondok pesantren was not only tiered and holistic but also dual (accountability to God and others).

This research has limitations in the scope of articles obtained for further analysis. Using the Google Scholar database on the topic of accountability in pondok pesantren was still focused on the Indonesian context. Using other databases with expanded keywords will cause more adequate database retrieval. Data analysis can also be conducted in more depth by uncovering the concept and meaning of accountability, both as applied to pondok pesantren and wider Islamic organizations.

The implications of this study show the variety of research approaches used to reveal the accountability of pondok pesantren. This research seeks to describe several research approaches used in both quantitative and qualitative research to capture the accountability practices of pondok pesantren. Qualitative research used more by previous researchers indicates that the concept of Islamic boarding school accountability is quite diverse in the practice of pondok pesantren in Indonesia. In addition, studies regarding the determinants of pondok pesantren accountability are still quite limited, so a more in-depth study is needed by examining various related theories.

Funding

No funding for this research.

Author contributions statement

Conception and design: Ahmad Nurkhin, Abdul Rohman, Tri Jatmiko Wahyu Prabowo.

Analysis and interpretation of the data: Ahmad Nurkhin, Tri Jatmiko Wahyu Prabowo.

Drafting of the article: Ahmad Nurkhin, Abdul Rohman.

Revising it critically for intellectual content: Ahmad Nurkhin, Abdul Rohman, Tri Jatmiko Wahyu Prabowo.

Final approval of the version to be published: Ahmad Nurkhin, Abdul Rohman, Tri Jatmiko Wahyu Prabowo.

All authors stated that agree to be accountable for all aspects of the work.

Disclosure statement

No potential conflict of interest was reported by the authors.

Data availability statement

The data obtained in this research is data that can be accessed openly via the Scopus database, Google Scholar and the Publish or Perish application. The data in this article are journal articles related to certain themes obtained through searching articles on the Scopus and Google Scholar databases. Data search using the publish or perish application. The data analyzed in this research can be openly accessed to be shared if needed.

Additional information

Notes on contributors

Ahmad Nurkhin

Ahmad Nurkhin is a student of doctoral program in economics, Faculty of Economics and Business, Universitas Diponegoro, Semarang, Indonesia. He is also a lecturer and researcher in accounting education, Faculty of Economics, Universitas Negeri Semarang, Semarang, Indonesia. He is a reviewer in some international and national academic journals. He active in organization profession of accounting and economic educator. His field of research are ICT and education, learning method, information system, and accounting. He was published some articles at international journal. He can be contacted at e-mail: [email protected].

Abdul Rohman

Abdul Rohman is a Professor at the Faculty of Economics and Business, Universitas Diponegoro, Semarang, Indonesia. He is the head of the UNDIP internal supervisory unit and has served as the head of the accounting master’s study program. He is active in the Indonesian Institute of Accountants (IAI) Central Java. His field of research is public sector accounting. He is also active in writing books and articles for reputable international journals. He can be contacted at e-mail: [email protected].

Tri Jatmiko Wahyu Prabowo

Tri Jatmiko Wahyu Prabowo is a Doctor of Accounting at the Department of Accounting, Universitas Diponegoro, Semarang, Indonesia. His main research is in public sector accounting. He has published some articles in the Journal of Public Budgeting, Accounting and Financial Management, Quality - Access to Success, International Journal of Supply Chain Management, and national accredited journal. He can be contacted at e-mail: [email protected].

References

- Abor, P. A., & Tetteh, C. K. (2023). Accountability and transparency: Is this possible in hospital governance? Cogent Business & Management, 10, 1. https://doi.org/10.1080/23311975.2023.2266188

- Adnan, M. I., Aliamin, & Mulyany, R. (2023). Accountability of traditional Islamic boarding school in Aceh. Jurnal Ilmiah Ekonomi Islam, 9(2), 1885–16. https://doi.org/10.29040/jiei.v9i2.8495

- Akbar, M. S., & Meirini, D. (2022). Perancangan Sistem Akuntansi Penerimaan Kas Pada Pondok Pesantren Al-Muchsinun Blitar. KITABAH: Jurnal Akuntansi Dan Keuangan Syariah, 6(1), 27–51. http://jurnal.uinsu.ac.id/index.php/JAKS/article/view/11481

- Al Faruqi, I. R. (1982). Al Tawhid: Its implication for thought and life. International Institute of Islamic Thought (IIIT).

- Alatawi, I. A., Ntim, C. G., Zras, A., & Elmagrhi, M. H. (2023). CSR, financial and non-financial performance in the tourism sector: A systematic literature review and future research agenda. International Review of Financial Analysis, 89, 102734. https://doi.org/10.1016/j.irfa.2023.102734

- Alfani, D., Harmain, H., & Syahriza, R. (2023). Pengaruh Kepercayaan dan Kepemimpinan Transformasional Terhadap Akuntabilitas Laporan Keuangan Pondok Pesantren Al Husna. AKUA: Jurnal Akuntasi Dan Keuangan, 2(2), 107–119. https://doi.org/10.54259/akua.v2i2.1540

- Alfie, A. A., Khanifah, & Nuranisya, G. H. (2023). Implementasi Akuntansi Pesantren Sebagai Bentuk Transparansi Dan Akuntabilitas Pelaporan Keuangan Pondok Pesantren. Jurnal Rekognisi Ekonomi Islam, 2(1), 13–27. https://doi.org/10.34001/jrei.v2i01.504

- Alhossini, M. A., Ntim, C. G., & Zalata, A. M. (2021). Corporate board committees and corporate outcomes: An international systematic literature review and agenda for future research. The International Journal of Accounting, 56(01), 2150001. https://doi.org/10.1142/S1094406021500013

- Anggara, F. S. A., & Faradisi, R. J. (2021). The implementation of corporate governance fundamental pillars based on Islamic perspective at Ma’had A-Muqoddasah Litahfidhil Qur’an. Management and Accounting Expose, 4(2), 71–79. http://jurnal.usahid.ac.id/index.php/accounting https://doi.org/10.36441/accounting.v4i2.261

- Arifin, Z. (2014). Pertanggungjawaban Keuangan Pondok Pesantren. Jurnal Ilmu Dan Riset Akuntansi, 3(1), 1–6.

- Arifin, S., & Anisah, A. (2019). Dinamika Pendidikan Pesantren. Fikrotuna; Jurnal Pendidikan Dan Manajemen Islam, 10(2), 1271–1291. https://doi.org/10.32806/jf.v10i02.3764

- Baehaqi, A., Faradila, N., & Zulkarnain, L. (2021). Akuntabilitas dalam akuntansi dan pelaporan keuangan pondok pesantren di Indonesia. Liquidity: Jurnal Riset Akuntansi Dan Manajemen, 10(1), 44–53. https://doi.org/10.32546/lq.v10i1.785

- Bakalikwira, L., Bananuka, J., Kaawaase Kigongo, T., Musimenta, D., & Mukyala, V. (2017). Accountability in the public health care systems: A developing economy perspective. Cogent Business & Management, 4(1), 1334995. https://doi.org/10.1080/23311975.2017.1334995

- Basri, H., Afifuddin, & Nabiha, A. K. S. (2010). Towards good accountability: The role of accounting in Islamic religious organisations. World Academy of Science, Engineering and Technology (WASET), 66, 1133–1139.

- Basri, H., Nabiha, A. K. S., & Majid, M. S. A. (2016). Accounting and accountability in religious organizations: An Islamic contemporary scholars’ perspective. Gadjah Mada International Journal of Business, 18(2), 207–230. http://journal.ugm.ac.id/gamaijb https://doi.org/10.22146/gamaijb.12574

- Basri, H., & Siti-Nabiha, A. K. (2016). Accounting system and accountability practices in an Islamic setting: A grounded theory perspective. Pertanika Social & Humanities, 24(S), 59–78. http://www.pertanika.upm.edu.my/

- Bovens, M. (2007). Analysing and assessing accountability: A conceptual framework. European Law Journal, 13(4), 447–468. https://doi.org/10.1111/j.1468-0386.2007.00378.x

- Bovens, M. (2010). Two concepts of accountability: Accountability as a virtue and as a mechanism. West European Politics, 33(5), 946–967. https://doi.org/10.1080/01402382.2010.486119

- Buanaputra, V. G., Astuti, D., & Sugiri, S. (2022). Accountability and legitimacy dynamics in an Islamic boarding school. Journal of Accounting & Organizational Change, 18(4), 553–570. https://doi.org/10.1108/JAOC-02-2021-0016

- Burhan, S. N., Yusnelly, A., Yulianti, S. (2023). The influence of Islamic boarding school accounting understanding, HR competence and Islamic boarding school accountability training on Islamic boarding school financial accountability. Jurnal Inovasi Bisnis Dan Akuntansi, 4(2), 548–559. https://doi.org/10.55583/invest.v4i2.641

- Dewi, N., Wijaya, I., Husin, D., Raihan, R., & Mawaddah, N. (2021). Pengaruh Pemahaman Standar Akuntansi dan Kompetensi Karyawan terhadap Akuntabilitas Pengelolaan Keuangan Pondok Pesantren di Aceh. Seminar Nasional Politeknik Negeri Lhokseumawe, 5(1), 56–58. https://e-jurnal.pnl.ac.id/semnaspnl/article/view/2723

- Firdausi, I. C., & Al Amin, M. (2021). Akuntabilitas pondok pesantren dalam konsep amar ma’ruf nahi munkar. Borobudur Accounting Review, 1(1), 57–65. https://doi.org/10.31603/bacr.4880

- Fitri, S. A., Nabilla, S. F., Karim, R. A., Nasution, R., Ayunda, T., & Sari, E. (2023). Pentingnya Penerapan Akuntansi Ponpes Pesantren Tarbiyah Islamiyah Pariangan. JAMMI – Jurnal Akuntasi UMMI, III(2), 63–74. https://doi.org/10.37150/jammi.v3i2.2040

- Ford, M. R., & Ihrke, D. M. (2017). School board member definitions of accountability: A comparison of charter and traditional public school board members. Journal of Educational Administration, 55(3), 280–296. https://doi.org/10.1108/JEA-04-2016-0040

- Gafur, A., Abdullah, R., & Adawiyah, R. (2021). Akuntabilitas berbasis amanah pada pondok pesantren. Jurnal Akuntansi Multiparadigma, 12(1), 95–112. https://doi.org/10.21776/ub.jamal.2021.12.1.06

- Gidado, A. D., & Yusha’u, A. S. (2017). Influence of accountability and transparency on governance in Islam. International Journal of Academic Research in Business and Social Sciences, 7(6), 449–456. https://doi.org/10.6007/ijarbss/v7-i6/3002

- Handayani, N., Ludigdo, U., & Rosidi, Roekhudin. (2022). The concept of financial accountability in education system: Study on private own Islamic boarding school. Quality – Access to Success, 23(189), 48–55. https://doi.org/10.47750/QAS/23.189.07

- Handayani, N., Ludigdo, U., Rosidi, R., & Roekhudin, R. (2021). The concept of shiddiq in financial accountability: An ethnomethodology study of boarding school foundation. The International Journal of Accounting and Business Society, 29(3), 63–98. https://doi.org/10.21776/ub.ijabs.2021.29.3.3

- Hanifah, R. U., Romadon, A. S., & Sulistyorini, S. (2022). Optimization of the implementation of PSAK 112 in an effort to increase accountability for the management and reporting of waqf assets at the Pondok Pesantren Foundation. Quantitative Economics and Management Studies, 3(3), 457–467. https://doi.org/10.35877/454RI.qems958

- Ibrahim, A. E. A., Hussainey, K., Nawaz, T., Ntim, C., & Elamer, A. (2022). A systematic literature review on risk disclosure research: State-of-the-art and future research agenda. International Review of Financial Analysis, 82, 102217. https://doi.org/10.1016/j.irfa.2022.102217

- Ja’far, A. K. (2018). Good corporate governance pada lembaga pendidikan pesantren: Studi pada pondok pesantren Universitas Islam Indonesia. AKADEMIKA: Jurnal Pemikiran Islam, 23(1), 197. https://e-journal.metrouniv.ac.id/index.php/akademika/article/view/1216 https://doi.org/10.32332/akademika.v23i1.1216

- Joannidès, V., & Berland, N. (2008). Reactions to reading “Remaining consistent with method? An analysis of grounded theory research in accounting”: A comment on Gurd. Qualitative Research in Accounting & Management, 5(3), 253–261. https://doi.org/10.1108/11766090810910254

- Kambey, A. N. (2021). Church accounting concepts with the understanding of God’s Kingdom. International Journal of Religious and Cultural Studies, 3(1), 39–52. https://doi.org/10.34199/ijracs.2021.04.03

- Kurniasari, W., Sawarjuwono, T., & Ryandono, M. N. H. (2019). The Islamic corporate governance implementation and program at Miftahussunnah Islamic Boarding School. Opción Año, 35(20), 1589–1606.

- Kurniawan, K., Alim, N., & Yuliana, R. (20200. Assessing the Governance Model and Fraud Prevention Based on Pesantren [Paper presentation]. The 1st Conference on Islamic Finance and Technology (CIFET) (pp. 1–17). https://doi.org/10.4108/eai.21-9-2019.2293956

- Lindberg, S. I. (2013). Mapping accountability: Core concept and subtypes. International Review of Administrative Sciences, 79(2), 202–226. https://doi.org/10.1177/0020852313477761

- Lu, Y., Ntim, C. G., Zhang, Q., & Li, P. (2022). Board of directors’ attributes and corporate outcomes: A systematic literature review and future research agenda. International Review of Financial Analysis, 84, 102424. https://doi.org/10.1016/j.irfa.2022.102424

- Lukka, K., & Vinnari, E. (2014). Domain theory and method theory in management accounting research. Accounting, Auditing & Accountability Journal, 27(8), 1308–1338. https://doi.org/10.1108/AAAJ-03-2013-1265

- Mahroji, M. S., & Rachmaini, N. (2022). Kegagalan nazir dalam tata kelola dan akuntabilitas pada kebangkrutan pondok pesantren. FairValue: Jurnal Ilmiah Akuntansi Dan Keuangan, 4(10). https://journal.ikopin.ac.id/index.php/fairvalue

- Makaryanawati, H., Suparti, P., & Muqorobin, M. M. (2020). Analysis of implementation sango application in pesantren accounting by using the technology acceptance model approach. International Journal of Business, Economics and Law, 23(1), 441–452. https://ijbel.com/wp-content/uploads/2021/03/IJBEL23-K23-222.pdf

- Meutia, I., & Daud, R. (2021). The meaning of financial accountability in Islamic boarding schools: The case of Indonesia. International Entrepreneurship Review, 7(2), 31–41. https://doi.org/10.15678/IER.2021.0702.03

- Miles, S. (2019). Stakeholder theory and accounting. In The Cambridge Handbook of Stakeholder Theory (pp. 173–188). Cambridge University Press. https://doi.org/10.1017/9781108123495.011

- Moher, D., Liberati, A., Tetzlaff, J., Altman, D. G., & PRISMA Group. (2009). Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. BMJ (Clinical Research ed.), 339, b2535. https://doi.org/10.1136/bmj.b2535

- Mulgan, R. (2000). “Accountability”: An ever-expanding concept? Public Administration, 78(3), 555–573. https://doi.org/10.1111/1467-9299.00218

- Murdayanti, Y., & Puruwita, D. (2017). Transparency and accountability of financial management in pesantren (Islamic education institution). Advanced Science Letters, 23(11), 10721–10725. https://doi.org/10.1166/asl.2017.10138

- Murdayanti, Y., & Puruwita, D. (2019). Kompetensi SDM keuangan dan akuntabilitas pesantren. Jurnal Akuntansi, Ekonomi dan Manajemen Bisnis, 7(1), 19–29. https://doi.org/10.30871/jaemb.v7i1.1085

- Murdayanti, Y., & Purwohedi, U. (2018). The usefulness of financial accounting systems in Islamic education institutions: Lessons learned. Academy of Accounting and Financial Studies Journal, 22(3), 1–14. https://www.abacademies.org/articles/The-Usefulness-of-Financial-Accounting-Systems-in-Islamic-Education-Institutions-Lessons-Learned-1528-2635-22-3-228.pdf

- Mzenzi, S. I. (2023). Accounting and accountability in Muslim secondary schools in Tanzania: A Bourdieusian perspective. International Journal of Public Sector Management, 36(1), 79–93. https://doi.org/10.1108/IJPSM-01-2022-0012

- Naz’aina, Raza., & H., Murhaban. (2022). Accountability Determination Analysis on Islamic Boarding Schools in Bireuen Regency. Budapest International Research and Critics Institute-Journal (BIRCI-Journal), 5(1), 378–6392. https://doi.org/10.33258/birci.v5i1.4360

- Nguyen, T. H. H., Ntim, C. G., & Malagila, J. K. (2020). Women on corporate boards and corporate financial and non-financial performance: A systematic literature review and future research agenda. In International Review of Financial Analysis, 71, 101554. https://doi.org/10.1016/j.irfa.2020.101554

- Nihwan, M., & Paisun, P. (2019). Tipologi pesantren (mengkaji sistem salaf dan modern). Jurnal Pemikiran Dan Ilmu Keislaman, 2(1), 59–81. https://www.jurnal.instika.ac.id/index.php/jpik/article/view/100

- Nilasari, Y., & Pangestuti, D. D. (2022). Akuntansi Pesantren Berbasis Kewirausahaan Berdasarkan SAK ETAP Dengan Aplikasi Myob. Owner, 7(1), 458–469. https://doi.org/10.33395/owner.v7i1.1299

- Oktafia, R., & Basith, A. (2017). Implementasi Good Corporate Governance pada Pondok Pesantren sebagai Upaya Peningkatan Daya Saing. Jurnal Ekonomi Islam, 8(1), 71–86. http://journal.uhamka.ac.id/index.php/jei

- Panut, P., Giyoto, G., & Rohmadi, Y. (2021). Implementasi Undang-Undang nomor 18 tahun 2019 tentang pesantren terhadap pengelolaan pondok pesantren. Jurnal Ilmiah Ekonomi Islam, 7(2), 816–828. https://doi.org/10.29040/jiei.v7i2.2671

- Periansya, D., Zakariah, E., Bin, S., Sawal, N. A. B., Frymaruwah, E., & Astuti, I. I. (2023). Financial reporting practice in pesantren: A comparative study of Malaysia and Indonesia. In 6th FIRST T3 2022 International Conference (FIRST-SS 2022) (pp. 38–43). https://doi.org/10.2991/978-2-38476-026-8_5

- Perry, A., & Hammond, N. (2002). Systematic reviews: The experiences of a PhD student. Psychology Learning & Teaching, 2(1), 32–35. https://doi.org/10.2304/plat.2002.2.1.32

- Plaisance, P. L. (2000). The concept of media accountability reconsidered. Journal of Mass Media Ethics, 15(4), 257–268. https://doi.org/10.1207/S15327728JMME1504_5

- Pratolo, S., Sofyani, H., & Maulidini, R. W. (2022). The roles of accountability and transparency on public trust in the village governments: The intervening role of COVID-19 handling services quality. Cogent Business & Management, 9(1). https://doi.org/10.1080/23311975.2022.2110648

- Raza, H. (2023). The influence of education, reporting behavior and perceptions of accounting standards on financial reporting accountability in Islamic Boarding Schools. Morfai Journal: Multidiciplinary Output Research for Actual and International Issue, 3(3), 611–620. https://doi.org/10.54443/morfai.v3i3.1223

- Rifa’i, M., & Wildaniyati, A. (2021). Penyusunan Laporan Keuangan Pondok Pesantren Darussalam Mekar Agung Tahun 2019 Berdasarkan Pedoman Akuntansi Pesantren. JAMER: Jurnal Ilmu – Ilmu Akuntansi, 2(2), 56–62. http://mail.unmermadiun.ac.id/index.php/jamer/index

- Roberts, J., & Scapens, R. (1985). Accounting systems and systems of accountability understanding accounting practices in their organisational contexts. Accounting, Organizations and Society, 10(4), 443–456. https://doi.org/10.1016/0361-3682(85)90005-4

- Rodiah, S., Satria, W., Agustina Putri, A., Azmi, Z., Gita Suci, R., Marlina, E., & Azhari, I. P. (2020). Akuntabilitas pengelolaan keuangan pada pondok pesantren Bahrul Ulum Pantai Raja Kampar. COMSEP: Jurnal Pengabdian Kepada Masyarakat, 1(1), 133–138. https://doi.org/10.54951/comsep.v1i1.32

- Safitri, R. N., & Narastri, M. (2023). Penerapan Akuntabilitas dan Transparansi Pengelolaan Keuangan Sesuai Interpretasi Standar Akuntansi Keuangan (ISAK 35) pada Yayasan Pondok Pesantren Assalafi Al Fithrah Surabaya. Management Studies and Entrepreneurship Journal, 4(2), 1781–1789. https://doi.org/10.37385/msej.v4i3.1442

- Sahri, Y., Permana, A., & Al-Haq, M. W. (2021). Analisis Penerapan Laporan Keuangan Berdasarkan Pedoman Akuntansi Pesantren Menggunakan PSAK No. 45. Eqien: Jurnal Ekonomi dan Bisnis, 8(2), 264–272. https://doi.org/10.34308/eqien.v8i2.256

- Setyawan, M. A. (2019). UU Pesantren: Local genius dan intervensi negara terhadap pesantren. MANAGERIA: Jurnal Manajemen Pendidikan Islam, 4(1), 19–40. https://doi.org/10.14421/manageria.2019.41-02

- Sofyani, H., Riyadh, H. A., & Fahlevi, H. (2020). Improving service quality, accountability and transparency of local government: The intervening role of information technology governance. Cogent Business & Management, 7(1), 1735690. https://doi.org/10.1080/23311975.2020.1735690

- Solikhah, S., Sudibyo, Y. A., & Susilowati, D. (2019). Fenomena Kualitas Laporan Keuangan Pesantren Berdasar Pedoman Akuntansi Pesantren Dan PSAK No. 45. SAR (Soedirman Accounting Review): Journal of Accounting and Business, 4(1), 19–39. https://doi.org/10.20884/1.sar.2019.4.1.1368

- Suaidah, Y. M., & Rohmatillah, E. (2022). Implementasi Prinsip-Prinsip Good Governance Pada Lembaga Pendidikan Pesantren (Studi Kasus Pada Pondok Pesantren Hamalatul Qur’an Jombang). SENMAKOMBIS: Seminar Nasional Mahasiswa Ekonomi Dan Bisnis, 6(1), 23–38. https://ejournal.stiedewantara.ac.id/index.php/SENMAKOMBIS/article/view/961

- Susilo, A., & Wulansari, R. (2020). Sejarah Pesantren Sebagai Lembaga Pendidikan Islam di Indonesia. Tamaddun: Jurnal Kebudayaan dan Sastra Islam, 20(2), 83–96. http://journal.stainkudus.ac.id/index.php/jurnalPenelitian/article/view/1325 https://doi.org/10.19109/tamaddun.v20i2.6676

- Syukri, M., Fitri, S. M., & Syafhariawan, H. (2023). Analisis Pelaporan Keuangan Pondok Pesantren Al-Muthmainnah Berdasarkan Pedoman Akuntansi Pesantren. Jurnal Economina, 2(1), 1175–1183. ejournal.45mataram.ac.id/index.php/economina https://doi.org/10.55681/economina.v2i1.266

- Tran, Y. T., & Nguyen, N. P. (2020). The impact of the performance measurement system on the organizational performance of the public sector in a transition economy: Is public accountability a missing link? Cogent Business & Management, 7(1), 1792669. https://doi.org/10.1080/23311975.2020.1792669

- Waluya, A. H., & Mulauddin, A. (2021). Akuntansi: akuntabilitas dan transparansi dalam QS. Al Baqarah (2): 282–284. Muamalatuna, 12(2), 15–35. https://doi.org/10.37035/mua.v12i2.3708

- Wati, R., Ardini, L., & Fidiana, F. (2022). The implementation of spiritual and financial accountability in Islamic boarding school. Al-Uqud: Journal of Islamic Economics, 6(1), 84–95. https://doi.org/10.26740/aluqud.v6n1.p84-95

- Wirawan, D. T. (2019). Social accountability process of Islamic Boarding School: Case study of Sidogiri Pasuruan Islamic Boarding School. International Journal of Multicultural and Multireligious Understanding, 6(1), 134–158. https://doi.org/10.18415/ijmmu.v6i1.497

- Wolor, C. W., Nurkhin, A., & Citriadin, Y. (2021). Leadership style for millennial generation, five leadership theories, systematic literature review. Quality – Access to Success, 22(184), 105–110. https://doi.org/10.47750/QAS/22.184.13

- Yuliani, N. L., & Mustofa, M. Z. (2022). Pengaruh Kompetensi Sumber Daya Manusia dan Pedoman Akuntansi Pesantren terhadap Akuntabilitas Pesantren. Akuisisi: Jurnal Akuntansi, 18(1), 86–97. http://www.fe.ummetro.ac.id/ejournal/index.php/JA