Figures & data

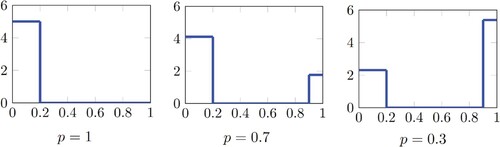

Figure 1. Depictions of for

and

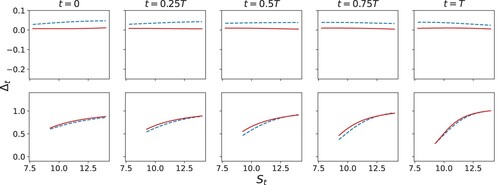

as p varies.

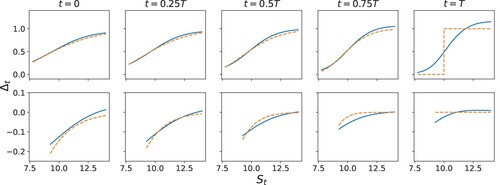

Figure 2. A comparison between trained non-robust strategies (blue) and Black–Scholes delta hedging (orange) for the knock-in call option. The top panel shows post-knock in strategies, while the bottom panels shows pre-knock in strategies.

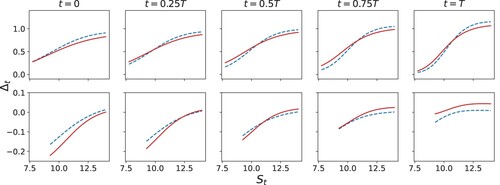

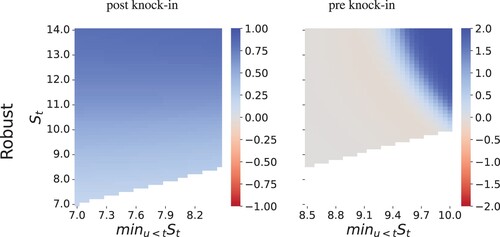

Figure 3. A comparison between robust (red) and non-robust (blue) strategies for the knock-in call option. The top panel shows post-knock in strategies, while the bottom panels shows pre-knock in strategies.

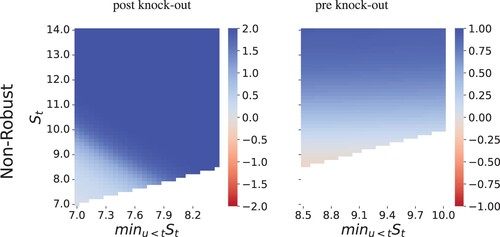

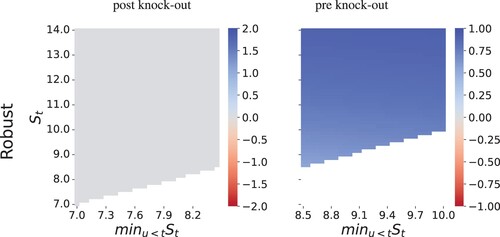

Figure 4. A comparison between robust (red) and non-robust (blue) strategies for the knock-out option. The top panel shows post-knock out strategies, while the bottom panels shows pre-knock out strategies.

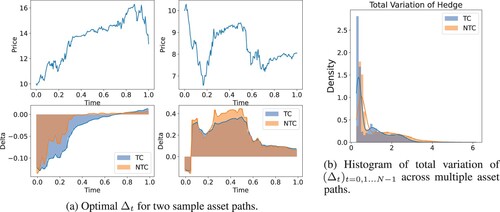

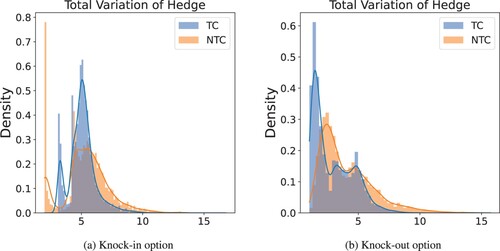

Figure 5. Strategies for hedging the down-and-in call option with transaction costs (TC) and with no transaction costs (NTC) built into the model. (a) Optimal for two sample asset paths and (b) Histogram of total variation of

across multiple asset paths.

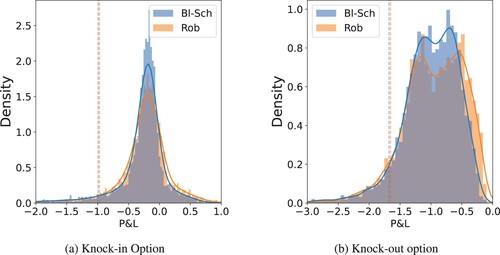

Figure 6. Comparison of Black–Scholes option hedging (Bl–Sch) and robust (Rob) P&L with transaction cost when model is misspecified with and

in reality. CVaR

is also shown. (a) Knock-in Option and (b) Knock-out option.

Table 1. Comparison of different pricing schemes.

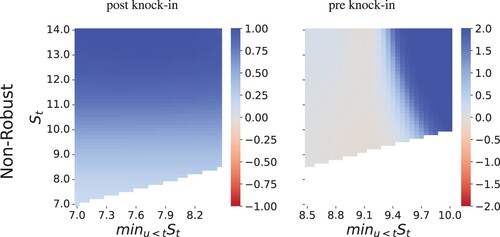

Figure 7. Non robust hedging strategies for a down-and-in call option. The graph show total asset holdings at t = 0.5T.

Figure 8. Robust hedging strategies for a down-and-in call option. The graph show total asset holdings at t = 0.5T.

Figure 9. Non robust hedging strategies for a down-and-out call option. The graph show total asset holdings at t = 0.5T.

Figure 10. Robust hedging strategies for a down-and-out call option. The graph show total asset holdings at t = 0.5T.

Figure 11. Comparison of total Variation of the hedge position across different asset price paths in cases with transaction costs (TC) and without transaction costs (NTC). (a) Knock-in option and (b) Knock-out option.

Figure 12. Comparison of non-robust(N-Rob) and robust (Rob) strategies. is shown as dotted lines in both plots. To help with visualizations, the x-axis uses a symmetric logarithmic scale, with values inside

displayed on a linear scale. (a) Knock-in Option and (b) Knock-out option.

![Figure 12. Comparison of non-robust(N-Rob) and robust (Rob) strategies. −RgU[Xθ] is shown as dotted lines in both plots. To help with visualizations, the x-axis uses a symmetric logarithmic scale, with values inside [−1,1] displayed on a linear scale. (a) Knock-in Option and (b) Knock-out option.](/cms/asset/56895f00-0f75-4a10-9366-1879662c0d5b/ramf_a_2301354_f0012_oc.jpg)

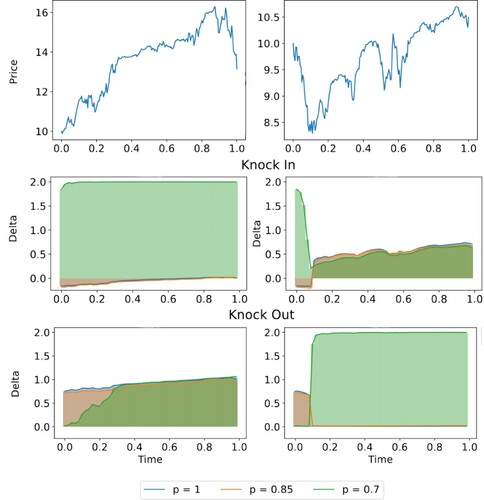

Figure 13. along two sample paths for knock-in (above) and knock-out (below) options. Strategies shown correspond to p = 1, 0.85 and 0.70.

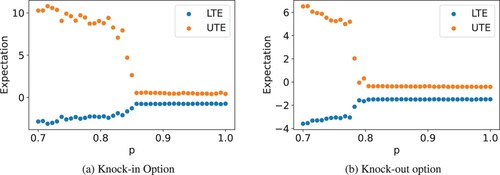

Figure 14. Comparison of lower tail expectation (LTE) and upper tail expectation (UTE) for and

while varying p. (a) Knock-in Option and (b) Knock-out option.