Figures & data

Table 1. Descriptive statistics for daily gain/loss (in IDR).

Table 2. Descriptive statistics for predictor variables of macroeconomy.

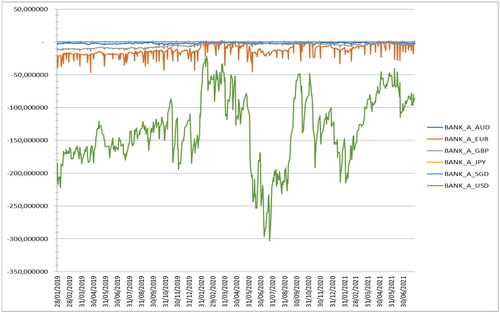

Figure 1. VaR estimation results for Bank A.

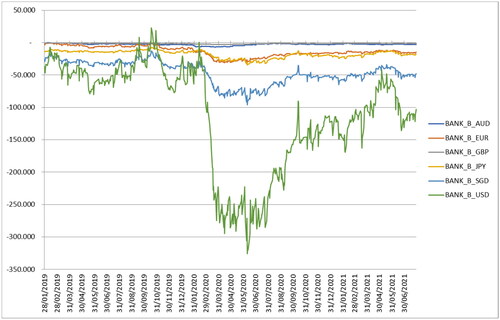

Figure 2. VaR estimation results for Bank B.

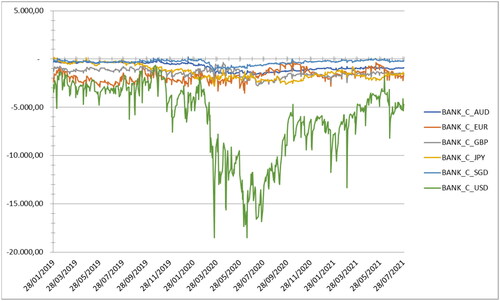

Figure 3. VaR estimation results for Bank C.

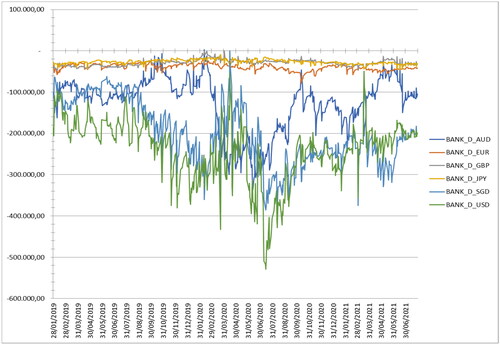

Figure 4. VaR estimation results for Bank D.

Table 3. Descriptive statistics of VaR estimation results.

Table 4. Dynamic quantile backtesting results.

Table 5. Backtesting results with benchmark model.

Data availability statement

The data used in this study (gain/loss data) is internal bank data that cannot be shared with the public.