ABSTRACT

This paper investigates how structural oil market shocks transmit through real oil price changes to the U.S. core prices. Separating out the sources of oil price increases reveals that supply shocks lead to significant and persistent increases in core prices while oil inventory demand shocks pull them down. Other demand-driven shocks do not cause any significant core price fluctuations. Examining different sample periods, we find empirical evidence supporting the strengthening of the oil price pass-through to some degree since mid-1980; however, not much change in the pass-through has been observed since the outbreak of Covid-19. Our findings highlight that understanding the sources of oil price changes is crucial for gauging their impacts on core prices and furthermore, for the conduct of monetary policy.

Acknowledgments

We would like to thank the editor (Kap-Young Jeong) and two anonymous referees for their valuable and constructive comments. We are grateful to Myungkyu Shim and the participants at the 2022 International Symposium on Econometric Theory and Applications for their helpful suggestions.

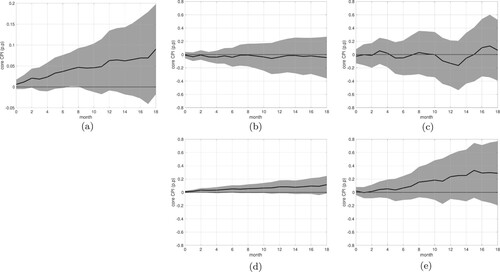

Figure A1. Pass-through of oil price shocks into core prices (1984M01–2016M12). (a) real RAC price. (b) Supply Shocks. (c) Economic Activity Shocks. (d) Oil Demand Shock and (e) Inventory Demand Shock.

Note: This figure reports the impulse responses of the core CPI to oil shocks, using data from 1984M01 to 2016M12. The grey-shaded area represents Newey and West (Citation1987)-corrected 95% error bands of the corresponding impulse responses in black solid lines. All of the structural shocks are normalised to elicit a 10% increase in the real RAC.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Funding

We acknowledge financial supports from Yonsei Economics Research Fund (R. K. Cho Research Cluster Program) and 2022 Yonsei Signature Research Cluster Program (2022-22-0012).

Notes

1 For more details on the definition and identification of shocks, we refer to pp.1888 in Baumeister and Hamilton (Citation2019).

2 The historical realisation of the four structural shocks before the normalisation is available on Christiane Baumeister's website: https://sites.google.com/site/cjsbaumeister/datasets?authuser=0.

3 One can alternatively extend the VAR model of Baumeister and Hamilton (Citation2019) by augmenting the U.S. core inflation in the system and by assuming a block diagonality in the impact matrix, similar in spirit to Aastveit, Bjørnland, and Cross (Citation2023). Compared to such an extended VAR model setup where the impulse responses are calculated as a non-linear function of structural shocks and reduced-form parameters, the local projection framework provides a simple way to calculate impulse responses without having to impose additional identification restrictions (Ramey Citation2016). In addition, both methodologies should result in similar impulse response estimates (Plagborg-Møller and Wolf Citation2021).

4 The starting period of our sample was determined by the supremum Wald break test results for real RAC and core price observations between 1984 and 2019. The final period was selected to December 2019 to exclude potential impacts of the Covid-19 pandemic. In Section 3, we conduct additional analysis by altering the sample periods.

5 As such, these studies did not include the 1970s in their main analysis, during which two oil crises had happened.

6 Alternatively, one may argue that the contradicting effects of oil supply and inventory demand shocks may have offset each other when passed through to core prices via oil prices increases, resulting in a muted response of core prices. To see if this is also feasible, we re-estimate our baseline model using data from the identical period as Conflitti and Luciani (Citation2019), January 1984 – June 2016, and show resulting responses of core prices in . We find that real RAC prices as well as structural oil market shocks do not significantly transmit to the core CPI and hence, the offsetting effects of different structural shocks have not likely caused the observed change in the pass-through pattern in .

7 We thank an anonymous referee for pointing this out.

8 Results using the number of deaths or hospitalised are very similar and available upon request.

9 Appendix 2 provides a detailed description of the analysis and resulting impulse responses.

10 This monthly survey asks respondents by what percent they expect prices in general will go up or down in the next 12 months. It also asks about how many cents the respondents expect gasoline prices will go up or down in the next 12 months. Questions asking respondents about their gasoline price expectations were included in the MSC questionnaire only from February 2006 on a continuous basis, prior to which these questions were asked intermittently. Hence, the estimated impulse responses of this variable are for periods starting from February 2006. While the former asks about expected price changes in percentages, the latter requires answers in cents, which may imply changes of drastically different sizes depending on the level of gasoline prices in the corresponding months. We hence divide the mean responses by the average monthly U.S. city average price of unleaded regular gasoline prices, obtained from the FRED database, and convert the responses in cents to percentages.

11 Since the raw data on price expectations is expressed in terms of the expected change, not the level of the price, we use the level of yt+h instead of cumulative differences in logs in Equation (1).

12 This series is downloaded from the FRED database.

13 The FRED data series of the average hourly earnings of all private employees start from March 2006. Hence, the estimated impulse responses of this variable are for periods starting from March 2006.

14 For instance, expectations for total inflation did not respond significantly to the oil supply shocks in the period ending before the COVID-19 outbreak. This appears to change greatly, once we include survey responses since 2020 but do not “de-covid”; consumers expected the overall price to climb substantially and significantly. However, such a change in the response pattern is not observed in the gasoline price expectation responses, as they remain statistically insignificant in the two sample periods. Hence, one may infer that the drastic change in total inflation expectation responds to the supply shocks by differences in expectation formation for non-energy prices.