Abstract

This study aims to examine the connection between global goals (sustainability) and corporate goals for long-term survival (business sustainability), as well as the role of Islamic business and work ethics in achieving them. 325 responses from employees of Islamic institutions were selected to be examined using the partial least squares (PLS-SEM). The results confirmed that business sustainability could be achieved by implementing Islamic business and work ethics and increasing awareness of sustainable goals (Sustainability Awareness). The results explained that when a company is aware of further goals such as sustainability, it will effectively achieve its ability to survive in the long term, called business sustainability. The originality of this study is providing a clear relationship between sustainability and business sustainability (long-term business goals), while previous research only analyzed sustainability toward business short-term goals.

IMPACT STATEMENT

Sustainability goals in an institution or corporation can be seen from two perspectives. First is the corporation’s ability to conduct business in the long term, and the second is how an organization encompasses economic, social, and environment-focused investments in its business model and operations. There was much research that put business sustainability as the corporate performance concerning economic, social, and environmental impacts. However, although global sustainability goals are important, corporations still need to assurance their business in the long term. Thus, the authors believe that this global sustainability orientation will not disadvantage the corporation, as this study has proven. In other words, this study tries to present another perspective on the business sustainability of the firm based on stakeholder and sustainability theory. As the author is concerned with Islamic business and ethics, the study focuses on Islamic institutions.

JEL CLASSIFICATION:

1. Introduction

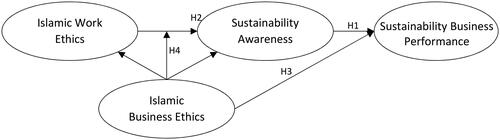

The objective of this research is to prove the relationship between Corporate Sustainability Awareness (SA) and Business Sustainability Performance (BS) and how Islamic Business Ethics and Islamic Work Ethics can optimize the achievement of Sustainability Awareness and Business Sustainability. Specifically, Islamic Business Ethics (IBE) is supposed to moderate Islamic Work Ethics (IWE) towards both Sustainability Awareness and Business Sustainability.

According to the theory, sustainability is described as achieving the needs of the present-day deprived of compromising the ability of future generations (United Nations Brundtland Commission) (Chang et al., Citation2017; Younus et al., Citation2012). The United Nations is attempting to occupy sustainability goals with Sustainability Development Goals SDGs) agenda in 2015, together with 194 countries in the world. There are 17 globals goals of SDGs that derived on 169 specific targets. The 17 goals could be grouped into five pillars, namely: People, Planet (environment), Prosperity (economy), Peace, and Partnership (Monteiro et al., Citation2024). The success of sustainability could be assessed due to 241 indicators of sustainable development goals (Ghoniyah & Hartono, Citation2020, pp. 2–3). National governments around the world, both developed and developing countries, have demonstrated their commitment to supporting sustainable practices by following a sustainable development agenda that focuses on implementing national-level sustainability initiatives through the Sustainable Development Goals (SDGs) Field (Ogundajo et al., Citation2022, p. 2). All parties should pursue this goal, including government, individuals, and institutions (Ghoniyah & Hartono, Citation2019, Citation2020).

Regarding sustainability goals in an institution or corporation, business sustainability can be defined from two perspectives. One interpretation might be related to a firm’s ability to conduct business in the long term (Bolton, Citation2015, p. 3). Another interpretation relates to how an organization encompasses human, social, and environment-focused investments in its business model and operations (Arianpoor & Salehi, Citation2021, p. 175; Bolton, Citation2015, p. 3; Gross-Gołacka et al., Citation2020; Sisaye, Citation2021, p. 5), this interpretation is inline with global sustainability goals. It could be defined that business sustainability is a company’s ability to run for a long time by making economic, social, and environmental aspects of their basic principles in running a business (Bolton, Citation2015, p. 3; Lashley, Citation2016).

Achieving sustainability must be pursued, among other things, by the institutions (Ghoniyah & Hartono, Citation2019, Citation2020). Accordingly, many studies have analyzed how companies carry out sustainability efforts every year. For example, the researcher (Lashley, Citation2016) researched leaders’ deep commitment toward sustainable business practices in the hospitality industry and concluded that the commitment to sustainability should be reflected in company foundations such as organizational mission, objectives, and goals. Marina and Imam Wahjono (Citation2017) highlights business sustainability in hospitals means a business continuity that is sustained by eco-efficiency, socio-efficiency, eco-effectiveness, socio-effectiveness, sufficiency, and ecological equity in the long-term. (Oudah et al., Citation2018) had analyzed the efforts of family companies in the United Arab Emirates to achieve business sustainability, namely meeting current needs without compromising the next generation’s ability to meet theirs. (Ghoniyah & Hartono, Citation2019) specifically analyzed the contribution of Islamic Banking in Indonesia towards Product Domestic Bruto as part of SDGs economic indicator. (Al-Abbadi & Abu Rumman, Citation2023; Al-Faouri, Citation2023; Habib et al., Citation2021; Latifah & Soewarno, Citation2023; Li et al., Citation2020; Najib et al., Citation2021) also analyzed the performance of sustainability in companies as the endogenous variable named Business Sustainability Performance or Corporate Sustainability Performance. This variable is commonly reflected in profits and economic performance, environmental performance, and social performance in the company.

On the other hand, other researchers reflected business sustainability based on the second definition delivered by (Bolton, Citation2015, p. 3), it is the firm’s ability to carry on business in the long term. For example, (Srisathan et al., Citation2020, p. 7) declared that organizational sustainability is the extent to which companies can survive and thrive in the future with plans to minimize potential harm to their business and those around them. As well as (Sarmawa et al., Citation2020) defined organizational sustainability as a multi-objective concept that is reflected through indicators such as Strategy related long-term economic, environmental, and social aspects, maintaining corporate financial conditions for long-term, Customer growth and product innovation, human resources management, and establish organizational governance standards for stakeholders. Different points of view between (Sarmawa et al., Citation2020; Srisathan et al., Citation2020) and (Al-Abbadi & Abu Rumman, Citation2023; Al-Faouri, Citation2023; Habib et al., Citation2021; Lashley, Citation2016; Latifah & Soewarno, Citation2023; Li et al., Citation2020; Marina & Imam Wahjono, Citation2017; Najib et al., Citation2021; Oudah et al., Citation2018; Pedersen et al., Citation2018; Taha et al., Citation2023) that make indicators or reflections of Business Sustainability very different.

The two definitions of business sustainability should not contradict each other (Bolton, Citation2015). However, (Daddi et al., Citation2019) highlighted the existence of a paradox theory in corporate sustainability, where the interests of the company’s profits and social and environmental impacts conflict with each other. Further researches by Pedersen et al. (Pedersen et al., Citation2018; Taha et al., Citation2023) have repulsed, as they have analyzed that corporate sustainability as maintain and grow corporate economic, social and environmental capital base while actively contributing to sustainability in the political domain and affect corporate financial performance itself, which reflected by profitability value.

The following factors motivate us to investigate the relationship between Sustainability Awareness and Business sustainability through Islamic Work Ethics and Islamic Business Ethics;

First, two definitions of business sustainability need to be separated clearly. (Al-Abbadi & Abu Rumman, Citation2023; Al-Faouri, Citation2023; Habib et al., Citation2021; Lashley, Citation2016; Latifah & Soewarno, Citation2023; Li et al., Citation2020; Marina & Imam Wahjono, Citation2017; Najib et al., Citation2021; Oudah et al., Citation2018) reflecting business sustainability as economic, social, and environment performance of the corporation, while (Sarmawa et al., Citation2020; Srisathan et al., Citation2020) explicitly reflecting business sustainability as the firm’s ability to carry on business in the long term. The different points of view between (Sarmawa et al., Citation2020; Srisathan et al., Citation2020) and (Al-Abbadi & Abu Rumman, Citation2023; Al-Faouri, Citation2023; Habib et al., Citation2021; Lashley, Citation2016; Latifah & Soewarno, Citation2023; Li et al., Citation2020; Marina & Imam Wahjono, Citation2017; Najib et al., Citation2021; Oudah et al., 2018; Pedersen et al., Citation2018; Taha et al., Citation2023) making indicators or reflections of Business Sustainability very different. The two definitions of business sustainability should not contradict each other (Bolton, Citation2015) but could be seen as processes and goals (Ghoniyah & Amilahaq, Citation2020).

Secondly, previous researchers have not linked sustainability awareness with business sustainability performance. (Pedersen et al., Citation2018; Taha et al., Citation2023; Van Stekelenburg et al., Citation2015) analyzes how corporate sustainability affects financial performance. (Pedersen et al., Citation2018; Taha et al., Citation2023) have proved that if corporations are highly concerned with economic, social, and environmental issues, it could increase their profit (corporate financial performance). Notwithstanding, corporate profit is a short term impact. While the long term business goal is the ability to survive and sustain (business sustainability) (Bolton, Citation2015). In other words, there is gap between the sustainability goals and the interests of the company to maintain their business sustainability.

Thirdly, this research aspires to prove the relationship between Corporate Sustainability Awareness and Business Sustainability Performance and how Islamic Business and Work Ethics can optimize the achievement of Business Sustainability through quantitative research. In Indonesia, it is essential to address spiritual ethics (Islamic ethics) because the majority of Indonesians are Muslim. Islam is a comprehensive faith that regulates the bond between humans and God and the relationship between humans and each other. Thus, separating religious matters from world business is an irresponsible action (secularism) (Ghoniyah & Amilahaq, Citation2020). Islam exists as a guide in carrying out every action related to religion and worship, as well as actions related to humankind activities, i.e. labor, commercial, professional, and behaving regarding others and the surroundings (muamalah) (Abuznaid, Citation2009), as written on the Al Quran (Islam’s holy book). Islam regulates not only the goals of humans but also how they are achieved. Thus, business ethics standards must include the value of goodness as a sturdier control than just rudiments of legality and attitude (Abuznaid, Citation2009).

Principally, social and environmental responsibility is not only charged to the large manufacturing corporations but also by every entity in the world to protect the world’s sustainability. This is in line with the purposes why humans were created, it is to become caliphs or leaders/guardians on Earth (Qur’an Surah Al Baqarah 2:30). From an Islamic perspective, the purpose of human on the earth is to worship Allah and become a caliph on earth (Qur’an Surah Al Baqarah:30, and Qur’an Surah Ad Dzariyat:56). The purpose is not limited to the goal of personal welfare but also to the welfare of all mankind and nature (Ghoniyah & Amilahaq, Citation2020). Thus, the Islamic goals align with sustainability goals developed by many countries.

Consequently, the current paper seeks to contribute to the existing literature.

First, this study tries to produce a clear picture of the role of sustainability goals in a business, especially the relationship between sustainability goals and business sustainability. So that global sustainability goals with the company’s goals to achieve business sustainability can be aligned without colliding with each other due to differences in interests.

Second, the study tries to change the business perspective of sustainability orientation not as a burden for corporations but as the responsibility and accountability of every entity. Doing something that has no material impact does not mean destroying the corporate future; it is quite the opposite. In other words, this study empirically analyzes the relationship between sustainability awareness and business sustainability. This is the novelty of this paper because it has not been studied before based on the author’s literature observation.

Third, the previous qualitative research believed embracing good ethical and spiritual values would obtain long-term corporate sustainability (Suriyankietkaew & Kantamara, Citation2019). (Lashley, Citation2016) supported the qualitative analysis of ethics regarding sustainability, and (Ezenwakwelu, Citation2020; Kurnia et al., Citation2020; Marina & Imam Wahjono, Citation2017; Sarmawa et al., Citation2020) demonstrated how business ethics could achieve business sustainability. The study analyzed how Islamic ethics of corporations and Islamic ethics belonging to Muslim employees could affect sustainability awareness and business sustainability.

Fourth, this research involves the foundation of the Al Quran in designing the model concept as the advantage of the research. It is known that Islam, with the Quran as its book, is a role model for all people in the world. This means that this concept has the potential to be effectively applied in any part of the world. Principally, social and environmental responsibility is not only charged to the large manufacturing corporation but also by every entity in the world to protect the world’s sustainability. This is in line with the purpose why humans were created, which is to become caliphs or leaders/guardians on Earth (Qur’an Surah Al Baqarah 2:30). From an Islamic perspective, the purpose of human on earth is to worship Allah and become a caliph on earth (Qur’an Surah Al Baqarah:30, and Qur’an Surah Ad Dzariyat:56). The purpose is not limited to the goal of personal welfare but also to the welfare of all mankind and nature (Ghoniyah & Amilahaq, Citation2020). Thus, the Islamic goals are in line with sustainability goals developed by many countries.

The remaining part of the paper is organised into Sections 2–7. Section 2 focuses on background related to the urgency of the study; Section 3 provides the main theory referenced, section 4 is a literature review and hypotheses development, section 5 is research design, Section 6 is related to the result and the discussion of findings, and the least the conclusion located on Section 7.

2. Background

When separating sustainability from business sustainability along a clear line, the question arises as to why companies should contribute to social goals and involve them deeply in the company’s mission and operations, as early capitalism theory emerged. As mentioned by Daddi et al. (Citation2019) about the paradox theory between sustainability orientation with corporate’s interest in gaining profit and survival. Therefore, a strong basic reason is needed to be oriented toward social goals while still trying to maintain business continuity.

The company was founded with the orientation of providing maximum profits to shareholders (shareholder theory). As time goes by, Freeman highlights that companies have a responsibility to the interests and needs of various parties involved in or affected by company decisions and activities (Freeman et al., Citation2010). The emergence of stakeholder theory emphasizes that companies not only have responsibilities towards shareholders but also toward employees, customers, suppliers, society, and other groups who have an interest in or are affected by the company’s operations. This understanding brings a shift in focus from the traditional concept that only considers shareholders to a view that is more inclusive and oriented towards relationships with all stakeholders.

Sustainability is an essential global goal. As an entity, a company’s actions should regard sustainability goals, not just aiming to benefit themself. Still and all, corporations should also achieve long-term goals for themselves, namely long-term survival. Based on these two interests, two definitions of business sustainability stated by (Bolton, Citation2015, p. 3) can be separated as process and objective/goals. Corporate sustainability that is reflected by the corporate performance related to economic, social, and environmental issues could be named corporate sustainability awareness, while the ability of a corporation to survive in the long-term is named the Business Sustainability Performance (Ghoniyah & Amilahaq, Citation2020). Sustainability awareness as a process means global sustainability goals in corporation become one way to achieve a sustainable business. The question arises of whether a sustainability awareness could harmonize with its Business Sustainability Performance empirically.

The empirical research between corporate sustainability awareness and business sustainability performance has not been done before. (Pedersen et al., Citation2018; Taha et al., Citation2023; Van Stekelenburg et al., Citation2015) analyzed how corporate sustainability affects financial performance. Meanwhile, other research on business sustainability performance has not separated clearly between the business goals and corporate sustainability awareness (Li et al., Citation2020; Lutfi et al., Citation2022; Najib et al., Citation2021). Therefore, this study intends to quantitatively examine the correlation between corporate sustainability awareness and business sustainability performance.

The study is also based on the recommendation of a previous researcher (Taha et al., Citation2023, p. 13). They suggested conducting more research to outline and classify suitable corporate financial indicators and how they correlate to sustainability performance procedures (Taha et al., Citation2023, p. 13). The use of company profit indicators together with company performance on social, environmental, and economic issues in previous studies has resulted in slightly ambiguous results.

The studies from developing countries still need to be made available (Taha et al., Citation2023, p. 13). One of them is in Indonesia. Indonesia as the majority population is Muslim, made the research that involves Islamic guidance prominent. Moreover, Islam exists as a guide in carrying out every action related to religion and worship, as well as actions related to humankind activities i.e. labor, commercial, professional, and behaving regarding others and the surroundings (muamalah) (Abuznaid, Citation2009), as written on the Al Quran (Islam’s holy book). For example, Sharia principle of Islam that guides Muslim that must be expected in every trade, commerce, business, and financial transactions (Albassam & Ntim, Citation2017, p. 183)

(Elamer et al., Citation2020, p. 915) suggested that religion can be influential in business decisions and operations. Moreover, it is empirically proven that corporations that voluntarily embrace and incorporate Islamic values into business operations signal their intention to commit to good governance standards (Albassam & Ntim, Citation2017, p. 186). Thus, this research involves Islamic ethics toward the model.

Islamic business ethics can be said as a combination of business strategy with Islamic principles, while social awareness basically is not only based on existing social issues but also is one of the responsibilities of Muslims as Caliphs on earth. The second element is from the Islamic point of view, namely how should Muslims set their goals for life in this world, and place them in daily life, both everyday Muslims as people who work, and in establishing vision and mission as well as values that must be owned by companies that become their mandate.

Previous qualitative research believed that embracing good ethical and spiritual values would obtain long-term corporate sustainability (Suriyankietkaew & Kantamara, Citation2019). (Lashley, Citation2016) supported the qualitative analysis of ethics regarding sustainability, and (Marina & Imam Wahjono, Citation2017) demonstrated how business ethics could achieve business sustainability.

To sum up, the study tries to answer the disconnect relation between sustainability at the macro intensity and micro (organization) intensity by figuring out macro-level sustainability as sustainability awareness in an organization (Dhanda & Shrotryia, Citation2021, p. 480). The study is also a follow-up of in-depth qualitative research done by authors in Ghoniyah and Amilahaq (Citation2020) that predicted the harmonized association between spiritual Business Ethics, Business Sustainability, and the Sustainability itself. This study proves the thought through empirical study.

3. Theoretical literature

3.1. Stakeholders theory

(Chang et al., Citation2017) explains the four basic theories that give rise to the concept of sustainability in companies. They are the theory of Corporate Social Responsibility (CSR) in 1953, the stakeholder theory in 1984, the corporate sustainability theory (1987), and the green economy theory.

Initially, companies were considered simply as economic entities primarily responsible to shareholders and only focused on achieving profits for shareholders. However, with increasing complexity and post-war social change, social responsibility of corporations starts to be highlighted. Companies have a moral responsibility to contribute to social welfare and maintain harmonious relations with society (Chang et al., Citation2017). CSR theory in this period emphasized that companies must go beyond economic goals and must be aware of their impact on society. Moreover, economic, environmental, and social CSR which is strengthened by profitability will consistently increase company value (Supriyadi & Ghoniyah, Citation2022).

The stakeholder theory emerged in 1984 as a significant development after the era of CSR theory in the 1950s. This theory brings changes in the understanding of corporate responsibility by emphasizing the role of various stakeholders in company management. In the beginning, the company’s main focus was only on shareholders as owners and shareholders (and investors). However, stakeholder theory, which was first introduced by R. Edward Freeman in his book ‘Strategic Management: A Stakeholder Approach’ (1984), changed this paradigm. Freeman highlights that companies have a responsibility to the interests and needs of various parties involved in or affected by company decisions and activities (Chang et al., Citation2017). As mentioned by (Indriastuti & Chariri, Citation2021, pp. 4–5) that stakeholder is any group or individual who can implement or be influenced by a company’s goals.

Stakeholder theory emphasizes that companies not only have responsibilities toward shareholders but also towards employees, customers, suppliers, society, and other groups who have an interest in or are affected by the company’s operations. This understanding brings a shift in focus from the traditional concept that only considers shareholders to a view that is more inclusive and oriented toward relationships with all stakeholders (Chang et al., Citation2017; Freeman et al., Citation2010). General stakeholder theory focuses on moral and ethical arguments and aims to guide stakeholder-oriented managers to consider multiple stakeholders in their corporate strategy (Taha et al., Citation2023, p. 3). The enterprise pays attention to all stakeholders and carries out its activities to provide environmentally friendly and environmentally responsible products, especially including the disposal of production waste (Latifah & Soewarno, Citation2023, pp. 4–5). Thus, Stakeholder theory states that a company’s operational capability is to incorporate stakeholder interests in decision-making (Indriastuti & Chariri, Citation2021, pp. 4–5).

Stakeholder theory based on Islam remarks the absolute and relative right of ownership and restructures the stakeholders themselves (Jakupović, Citation2023). Allah SWT is the absolute owner of every entity in the world, while humans are the caretakers/Khalifah (relative right of ownership) (Qur’an Surah Al Baqarah 2:30). Even though an entity or corporation is responsible to all stakeholder parties in the surroundings, the corporation also has a responsibility towards Allah SWT. In this stage, the Almighty has no interest in the corporation such as any other stakeholders. God does not receive any benefits or disadvantages from the corporate decision but could affect how the decision will be taken based on the Guidance Allah provided namely Al Quran. The intervention of Islamic rule (Al Quran) could be seen in the corporate foundation such as goals, mission, objective, and ethical values (Abuznaid, Citation2009). Thus, it is important to encourage the importance of ethical behavior in business (Abuznaid, Citation2009; Ghoniyah & Amilahaq, Citation2020; Jakupović, Citation2023).

3.2. Sustainability theory

In 1987, the emergence of the Brundtland Commission’s ‘Our Common Future’ report, officially introduced the concept of sustainable development and provided a more thorough definition of sustainability, namely development that ‘meets the needs of current generations without compromising the ability of future generations to meet their needs Alone.’ Corporate sustainability theory emerged after stakeholder theory adopted the principles of sustainable development in a business context. This emphasizes that companies must consider the interests of internal and external stakeholders, while ensuring that their business activities do not harm the environment and society. As issues such as climate change and concerns about limited natural resources emerge, stakeholders are starting to emphasize the need for a more sustainable economic model (Bolton, Citation2015; Chang et al., Citation2017).

Principally, social and environmental responsibility is not only charged to the large manufacturing corporations but also by every entity in the world to protect the world’s sustainability. This is in line with the purpose humans were created, which is to become caliphs or leaders/guardians on Earth (Qur’an Surah Al Baqarah 2:30). From an Islamic perspective, the purpose of humans on earth is to worship Allah and become a caliph on earth (Qur’an Surah Al Baqarah:30, and Qur’an Surah Ad Dzariyat:56). The purpose is not limited to the goal of personal welfare but also to the welfare of all mankind and nature (Ghoniyah & Amilahaq, Citation2020). Thus, the Islamic goals are in line with sustainability goals developed by many countries.

4. Empirical literature review and hypotheses development

4.1. Business sustainability

Business sustainability means sustainability at the organizational level that leads to a deep commitment to sustainable business practices and awareness related to human, social, and environment (Al-Abbadi et al., Citation2023, p. 3; Bolton, Citation2015). This pledge is decoded into organizational missions, objectives, and purposes (Bolton, Citation2015; Gross-Gołacka et al., Citation2020; Lashley, Citation2016). Sustainability matters should be contemplated in making company decisions. Those who put sustainability as the ultimate goal could be reflected by their activities and policies.

Business sustainability could also be expressed as its proficiency to persist in business over the long term (Asriati et al., Citation2022, p. 5; Bolton, Citation2015, p. 3). Thus, even though maximizing profit is important, it is much better to have continuous profits in the future. This means that the firm’s purpose should be its ability to run the business continuously for long-term value creation (Arvidsson, Citation2022, p. 47; Bolton, Citation2015; Freeman et al., Citation2010). With long-term orientation, the company can guarantee a profit stream in the future (Perri & Teague, Citation2022). To survive in the long term, companies also need to ensure that resources and the surrounding environment are sustainable, namely by committing to running a business (business operations) in accordance with the principles of sustainability (Lashley, Citation2016; Salehi & Arianpoor, Citation2021, p. 1449).

To reflect business continuity, measurement from one dimension or point of view is insufficient to deliver an inclusive illustration. Performance measurement must incorporate various measurement dimensions i.e. growth and ability (Bhargava et al., Citation1994). The belief in long-term business sustainability in an organization not only be reflected in the profit movement and the corporate growth but also in the support of the company’s people and goals for its involvement in socio-economic and environmental issues (Bhargava et al., Citation1994; Brønn & Vidaver-Cohen, Citation2009). This research must encompass the company’s impression according from the worker, related to their attachment to the corporate values (Brønn & Vidaver-Cohen, Citation2009; Freeman et al., Citation2010; Lashley, Citation2016; Marina & Imam Wahjono, Citation2017).

4.2. Sustainability (sustainability awareness)

The concern of sustainability was introduced in 1987 by the United Nations Brundtland Commission. They defined sustainability as the condition where one could achieve the needs of the present-day deprived of compromising the ability of future generations (United Nations Brundtland Commission) (Chang et al., Citation2017; Younus et al., Citation2012). The United Nations is attempt to occupy sustainability goals with Sustainability Development Goals SDGs) agenda. National governments around the world both developed and developing countries, have demonstrated their commitment to supporting sustainable practices by following a sustainable development agenda that focuses on implementing national-level sustainability initiatives through the Sustainable Development Goals (SDGs) (Ogundajo et al., Citation2022, p. 2). This goal should be pursued by all parties, including government, individuals and institutions (Ghoniyah & Hartono, Citation2019, Citation2020).

Awareness of protecting the future has led to the concept of sustainability (Taha et al., Citation2023, pp. 1–2). Awareness of sustainability refers to individuals’ and communities’ understanding of the importance of acting and living sustainably. They pay attention to the economic, social and environmental impacts of their actions. Awareness of sustainability motivates people to adopt behaviors, lifestyles and decisions that support sustainable development goals. In other words, awareness of sustainability is an important driver in creating positive change that supports the SDGs and ensures that we achieve the sustainable development goals.

Sustainability is fundamentally defined based on three factors: economic environmental and social (Taha et al., Citation2023, pp. 1–2). Sustainability indicators generally use macro-level statistical data (Central Bureau of Statistics, Citation2016, Citation2018; Ghoniyah & Hartono, Citation2020). Meanwhile, this study uses perspectives of institutional orientations and their actions related to global sustainability issues (Dhanda & Shrotryia, Citation2021). Previous research about sustainability in business has separated economic performance, social performance, environmental performance, regarding financial performance of corporate (Pedersen et al., Citation2018; Taha et al., Citation2023). Corporate sustainability performance in those researches refers to corporate awareness and action in responding to sustainability issues. For example, (Pedersen et al., Citation2018; Taha et al., Citation2023) reflected sustainability orientation in corporation as Corporate sustainability performance using secondary data sources from corporate, while in this study using primary data that could reflect the action of organization. Therefore, sustainability indicators using primary data must be reversed to the correct measurements (Fukuyama, Citation2018; Najib et al., Citation2021; Pedersen et al., Citation2021), or example, harmonize their economic purposes with upholding the environment and humanity matters (Abdelnaeim & El-Bassiouny, Citation2021, p. 1034). Thus in this research, we named sustainability in corporation as sustainability awareness.

4.3. Islamic business ethics

Islamic Business Ethics emphasizes business practices that comply with the moral principles of Islamic Sharia law. These principles include fairness in transactions, prohibition of usury, economic sustainability, and corporate social responsibility (Marina & Imam Wahjono, Citation2017). Islamic principle is the proper ethics to attain business continuity and the sustainability, especially for corporations that put Islamic principles as the core of their value. Thus, Islamic principles must be applied to company and employee ethics (Abuznaid, Citation2009; Albassam & Ntim, Citation2017, p. 182; Elghuweel et al., Citation2017).

According to behavioral theory, (Elghuweel et al., Citation2017, pp. 191–193) conjectures that corporate engagement could be influenced by informal Islamic religious experiences, beliefs and values in a predominantly Islamic country. Consequently, trade, commerce, business and financial transactions are expected to reflect Islamic principles generally. (Albassam & Ntim, Citation2017, p. 183). Moreover, it is inadvisable to separate religious and worldly matters (secularism). This is because Islam is basically a guide to all acts of worship (Ibadah) and worldly matters such as partnership, build a business, working, or dealing with other people/stakeholders and the environment (Mumallah) (Abuznaid, Citation2009).

4.4. Islamic work ethics

Islamic work ethics are based on Islamic rules in the Al Quran and Hadith which a Muslim applies in carrying out his work (Ali & Al-Owaihan, Citation2008; Balkis Binti Mohd Yusof et al., 2017; Romi et al., Citation2020). Islamic work ethic incorporates Gods involvement in every action (Akhavan et al., Citation2014; Asifudin, Citation2004). In the Islamic view, work is considered as a tool to improve life economically, socially and psychologically on the basis of belief in Allah SWT. Therefore, Islamic work ethics can be concluded as a set of values, principles and moral norms that underlie behavior and actions in the context of work or business, based on Islamic principles (Asifudin, Citation2004; Ghoniyah, Citation2010). What is done is seen as a commendable act (Asifudin, Citation2004; Ghoniyah, Citation2010).

The essence of Islamic work ethics comes from intentions rather than final results (Ali & Al-Kazemi, Citation2007; Ali & Al-Owaihan, Citation2008; Kumar & Che Rose, Citation2010, Citation2012). Some practical examples of Islamic work ethics; honesty, transparency, fairness, quality and dedication, social responsibility, environmental responsibility, work life balance, legal compliance (Asifudin, Citation2004; Ghoniyah, Citation2010).

4.5. Hypotheses development

4.5.1. The relationship between business sustainability and sustainability awareness

(Al-Abbadi et al., Citation2023; Bolton, Citation2015) had defined business sustainability in two different perspectives, i.e. sustainability orientation regarding economic, social, environmental issues, and sustainability of the corporation to run the business in the long term. (Taha et al., Citation2023, p. 3) also agree that there is gaps related to the usage of the sustainability dimension on the performance of companies itself. Thus this study hypothesizes that sustainability is a process and goal (Ghoniyah & Amilahaq, Citation2020). Sustainability, as a conscious effort or action carried out by a company (sustainability awareness), can achieve the sustainability of the company’s own business. (Pedersen et al., Citation2018; Taha et al., Citation2023) reflected sustainability orientation in the corporations as Corporate sustainability performance using secondary data sources from corporations, while this study used primary data that could reflect the organization’s action. Thus, we named it as sustainability awareness.

Previous research has proven that corporate sustainability performance could affect short term business goals i.e. the profit (Pedersen et al., Citation2018; Taha et al., Citation2023). This study elaborates on the endogenous variable becoming long-term business goals, i.e. business sustainability. The hypothesis is that sustainability awareness could affect business sustainability (H1) (Ghoniyah & Hartono, Citation2020; Li et al., Citation2020; Lutfi et al., Citation2022; Najib et al., Citation2021; Pedersen et al., Citation2018; Taha et al., Citation2023).

4.5.2. The relationship between Islamic work ethics and business sustainability

Muslims should act according to Islamic ethics, whether as individuals, social creatures, workers, or employers (Akhmadi et al., Citation2023, p. 3). A commendable act must have a value of worship toward God (ï·² سبحانه و تعالى) through the purpose and the sincerity of intention (husnul fa’iliyyah) (Akhavan et al., Citation2014; Asifudin, Citation2004, p. 93; Ghoniyah, Citation2010). Thus, Islamic work ethics are not only reflected by the excellent effort to obtain business sustainability but also the intention to accomplish the pleasure of God (ï·² سبحانه و تعالى) also as the accountability of humans as caliphs on earth. Implementing Islamic work ethics could also achieve social and environmental benefits, for example, achieving sustainable development goals as the responsibility of all parties, individuals, and agencies (Akhmadi et al., Citation2023; Central Bureau of Statistics, Citation2016; Guidara, Citation2022).

Previous research regarding Islamic work ethics has described the appliance in the corporation as an organizational approach to creating a sense of ownership of the company in workers. By having self-belonging in employees, the performance of employees would improve (Marina & Imam Wahjono, CitationCitation2017; Mohammad et al., Citation2018). Employees’ dedication is a long-term asset that could uphold business continuity (Ghoniyah, Citation2010; Perri & Teague, Citation2022), especially if the employees apply an Islamic work ethic. Thus, the study hypothesizes that Islamic work ethics can have an impact on sustainability awareness practice and business sustainability (H2).

4.5.3. The relationship between Islamic business ethics and business sustainability

According to Islam, business activities do not solely increase material profits (Gymnastiar, Citation2006, p. 78). In Islam, profit or benefit must be seen from the final outcome and how to obtain and use them (Ghoniyah, Citation2010). Companies are required not only to implement excellent business standards but also to be long-term oriented and contribute to social benefits (Akhmadi et al., Citation2023, p. 4; Lashley, Citation2016), such as sustainable development goals (Ordonez-Ponce et al., Citation2021, p. 1242). Business ethics standards must include the values of goodness as a sturdier control than just the elements of legality. For example, policies that meet both the standards and the ethics, which leads to both legal and good (halal and tayyib) (Abuznaid, Citation2009; Lashley, Citation2016; Marina & Imam Wahjono, Citation2017; Suriyankietkaew & Kantamara, Citation2019).

Islam regulates not only human goals but also how to achieve those goals (Ghoniyah, Citation2010). Islam exists as a guide in carrying out every action related to religion and worship, as well as actions related to world affairs i.e. labor, commercial, professional, and behaving regarding others and the surroundings (muamalah) (Abuznaid, Citation2009). Therefore, achieving sustainability goals and business sustainability goals should recognize the method and ethics used (Akhavan et al., Citation2014; Ghoniyah, Citation2010; Ghoniyah & Amilahaq, Citation2020).

Previous qualitative research believed that to accomplish long-term business sustainability, the enterprise should embrace right ethical and spiritual values (Marina & Imam Wahjono, Citation2017; Suriyankietkaew & Kantamara, Citation2019), and so did to gain sustainability goals (Lashley, Citation2016). In other words, ethics are crucial for the sustainable accomplishment of the triple-bottom-line goal (Suriyankietkaew & Kantamara, Citation2019).

Preceding research believed that companies have immense proficiency in encouraging their workers to act based on Islamic ethics. Institutions that developed Islamic values as their main foundation could create a pleasurable and peaceful workplace. After all, the bonding could arise and the company’s sustainable business could be achieved (Ghoniyah & Amilahaq, Citation2020). Thus, this research developed the third hypothesis: Islamic Business Ethics could affect Sustainability Awareness and Business Sustainability (H3)

4.5.4. The relationship between Islamic business ethics and Islamic work ethics

Islamic business ethics and Islamic work ethics are interconnected and support each other. Applying Islamic business ethics means running a business with Islamic principles, such as justice, honesty, transparency and social responsibility. This includes fair treatment of customers, suppliers, and all parties involved in the business (Marina & Imam Wahjono, Citation2017),. When organizations implement Islamic business ethics well, this usually creates a work environment that aligns with Islamic values. Employees will be expected to adhere to Islamic work ethics, such as working diligently, respecting the rights of fellow employees, and maintaining a balance between work and personal life (Asifudin, Citation2004; Ghoniyah, Citation2010).

In other words, implementing Islamic business ethics in an organization usually creates a strong foundation for implementing Islamic work ethics (De Clercq et al., Citation2018, p. 13). However, it remains the organization’s responsibility to ensure that these values are well integrated in all aspects of its operations, including in relationships with employees and in creating a work environment following Islamic ethics. Based on the literature review, the fourth hypothesis is that Islamic Business Ethics could moderate Islamic Work Ethics toward Sustainability and Business Sustainability (H4).

below provides a description of the research model based on the aforementioned hypotheses.

Figure 1. Research model. Source: Authors’ creation (2023).

5. Research design

The research variables consist of exogenous and endogenous variables. The Dependent Variable for this research is Business Sustainability, while the Independent Variable for this research is Islamic Work Ethics. Islamic Business Ethics is a moderating variable between Islamic Work Ethics and Sustainability Awareness. Meanwhile, Sustainability Awareness is a mediating variable between Islamic Work Ethics and Business Sustainability. Based on this explanation, the Operational Definition of Variables can be presented as follows ().

Table 1. Operational definition of variables.

The study employed quantitative survey research design as continuation of previous qualitative research (Ghoniyah & Amilahaq, Citation2020). This research is at the stage of proving the hypothesis of the relationship between the application of Islamic Work ethics and Islamic Business Ethics to increase Sustainability Awareness and Business Sustainability. In this study, Islamic business ethic refers to the object of research in institutions that uphold Islamic values as corporate values (Abuznaid, Citation2009). Thus, respondents for this research were employees in Islamic institution in Indonesia.

The questionnaire items used in this study were developed and adapted based on existing literature. Section 1 of questionnaire discusses the characteristics of the sample, including gender, age, education, income, and types of industries. In Section 2, respondents were asked to read statements and determine their degree of agreement on a 10-point scale (‘strongly disagree’ to ‘strongly agree’). Answers to each question posed are arranged into seven alternative explanations ranging (Asriati et al., Citation2022, pp. 7–8). The scale for the current study offers more options for respondents and also helps the researcher better understand the answer (Sheikh et al., Citation2018, pp. 8–9). Before completing the questionnaire, we performed a pre-test to check the word sentence, then tested again for its reliability and validity (Asriati et al., Citation2022, pp. 7–8).

The questionnaire was distributed to the employee manager in Islamic Institution in Indonesia, specifically in Middle Java Regency as the third largest population. The data has been collected from September 2022 to January 2023 by twenty-five Institutions that declared Institutions with Islamic Corporate values as their foundation. In the first phase, 243 data were received; on the second coming, 115 additional data could be received, and in total, 358 data were obtained. From this record, 33 answers were excluded due to incomplete and the same answer to all questions and missing answers. Finally, a usable sample of 325 valid answers was kept for analysis. The amount accounted for 85.52% valid responses of this study (Habib et al., Citation2021, p. 10), based on the sample targeted as 370 (37 questions times 10) (Hair et al., Citation2013, Citation2019; Memon et al., Citation2020). The method of Structural Equation Modeling (SEM) analysis considered in this study requires a sample size of over 200 observations, as suggested by the maximum likelihood estimation approach. Additionally, the research aims to analyze the data using SmartPLS 3, which helps in statistical processes. (Al-Faouri, Citation2023, pp. 7–8)

Partial Least Square (PLS) analysis was used to analyze the data that were obtained from the questionnaire (Ghozali & Latan, Citation2015a) (Ghozali & Latan, Citation2015b; Pedersen et al., Citation2018). The following procedures were used to test the empirical research model based on the PLS: (1) create a causal link diagram showing the causal relationship between the constructs for both latent variables and between latent variables with indicators and an estimate of each variable’s specific value; (2) conduct a validity test; (3) read the outer model using composite reliability techniques, convergent validity, and discriminant validity; and (4) read the inner model (Amilahaq & Ghoniyah, Citation2019).

6. Empirical results and discussion

6.1. Respondent demographic

This research was conducted at a profit and non-profit Islamic institution, and 325 respondents who worked in Islamic institutions were selected. Respondent demographic analysis can be presented in the following table ().

Table 2. Respondent demographic.

6.2. Analysis partial least square

6.2.1. Quality of the measurement

The quality of the measurement model was tested on the basis of the data presented in . The reliability of the models could be proven by Cronbach’s alpha or composite reliability value of more than 0.7 points. The validity test is expressed from the value of AVE (average variance extracted) and the factor loading. The AVE value should be more than 0.5, while the factor loading should be more than 0.4 points. All the quality criteria for reliability and validity were accomplished, as shown in . (Ghozali & Latan, Citation2015b; Pedersen et al., Citation2018).

Table 3. Quality of the measurement models.

The quality of the measurement model was tested on the basis of the information accessible in .

6.2.2. Hypotheses testing

Hypothesis testing was performed using the outcome of the Partial Least Square (PLS) inner model. This test was carried out to prove the relationship among latent variables by examining the results of the t-statistics and the significance level of influence (p-value) showed in .

Table 4. Hypotheses testing, result of path coefficient, and indirect effect.

This hypothesis predicts that business and sustainability can be explained by a relationship. In this study, it is suspected that a company’s awareness of sustainability goals can increase its business sustainability (long-term survival). shows that sustainability awareness significantly influenced business sustainability at a significance level of <0.001. A high coefficient indicates that every 1 point of a company’s sustainability awareness can increase its own business’s sustainability by 0.628 points. Thus, Hypothesis 1 was accepted.

The second hypothesis predicts the influence of Islamic Work Ethics increases business sustainability. Testing the direct relationship shows that Islamic Work Ethics is not able to have a direct impact, because the significance level is >0.05 (p-value 0.056). However, with Sustainability Awareness, Islamic Work Ethics will have a much more effective impact on maintaining business continuity, with a significance level of <0.01 and coefficient of 0.141. Thus, hypothesis 2 can be accepted that IWE has a positive effect on Business Sustainability through Sustainability Awareness as an intermediary.

The third hypothesis is that Islamic Business Ethics can increase a company’s long-term survival. The test results show that Islamic Business Ethics can improve Business Sustainability, both directly and indirectly. Islamic Business Ethics can directly impact Business Sustainability with a significance level of <0.01 and a coefficient of 0.208. Islamic Business Ethics also had an indirect effect on Business Sustainability through Sustainability Awareness, with a significance level of <0.001 and a coefficient of 0.451. Thus, Hypothesis 3 is accepted.

The fourth hypothesis predicts that Islamic Work Ethics cannot stand alone but that there is intervention from Islamic Business Ethics in contributing to Business Sustainability. shows that the moderation ability of Islamic Business Ethics toward Islamic Work Ethics is proven to be effective, with a significance level of 0.05, either directly or through Sustainability Awareness intermediaries. Thus, H4 was accepted.

The magnitude of the independent variables’ influence on the dependent variable is displayed in .

Table 5. R-square results.

Based on , the contribution of Sustainability Awareness, Islamic Work Ethics, and Islamic Business Ethics to Business Sustainability Performance was 66.2%. In other words, 66.2% of a company’s long-term survival is influenced by how IBE, IWE, and concern for sustainability are implemented, while 33.8% is affected by other factors. The contribution of Islamic business ethics and work ethics to sustainability awareness is 59.4%. This means that to increase company concerns related to sustainability issues, 59.4% are influenced by the IBE and IWE of the company, and the other 40.6% are influenced by other factors outside the research.

6. Discussion

6.1. Sustainability awareness on business sustainability

This study proves that awareness of sustainability goals can increase the sustainability of a business itself. In a business context, business sustainability can be defined as a firm’s ability to carry on business in the long term, can also be defined that business sustainability relates to how an organization encompasses human, social, and environment-focused investments into its business model and operations (Bolton, Citation2015, p. 3). These two definitions can be seen as processes and goals, namely the process seen in sustainability awareness of corporate, while the final goal is the business sustainability. As mentioned on the introduction and background of this writing, previous researchers have mixed economic issue with profit issue belong to corporation on measuring business sustainability (Al-Abbadi & Abu Rumman, Citation2023; Al-Faouri, Citation2023; Habib et al., Citation2021; Latifah & Soewarno, Citation2023; Li et al., Citation2020; Monteiro et al., Citation2024; Najib et al., Citation2021). Taking everything into consideration, this result can be regarded as a novelty and thread that connects sustainability goals with business sustainability (Bolton, Citation2015; Ghoniyah & Amilahaq, Citation2020; Ghoniyah & Hartono, Citation2020; Lashley, Citation2016; Lutfi et al., Citation2022; Marina & Imam Wahjono, Citation2017; Najib et al., Citation2021).

This study supports the application of stakeholder theory and sustainability theory. Theory states that companies must pay attention to the interests of all parties, not just pursue profit. Attention to stakeholders does not separate company operations from social responsibility as in corporate social responsibility theory. Sustainability theory also calls for how company operations are based on sustainability issues, as stated in the theory of sustainability in companies; that is how an organization encompasses human, social, and environment-focused investments into its business model and operations (Bolton, Citation2015, p. 3).

Corporate sustainability theory adopted the principles of sustainable development in a business context. The theory emphasizes that companies must consider the interests of internal and external stakeholders, while ensuring that their business activities do not harm the environment and society in a sustainable manner (Bolton, Citation2015; Chang et al., Citation2017). The company’s contribution is not only reflected in the corporate social responsibility actions taken, but also in more detail in the selection of raw materials, resource utilization, and waste treatment (input, process, output), even reflected on the corporate governance policies (Salehi & Arianpoor, Citation2021).

The study also refuse paradox theory stated by Daddi et al. (Citation2019). Due to the empirical result, when corporate give concern toward social economic and environmental issue, it actually could help the corporation to survive in long-term. This reinforces the demand for changes in the business processes owned by companies to focus on social, environmental, and economic impacts, both directly and indirectly (Freeman et al., Citation2010; Ghoniyah & Hartono, Citation2020; Gladwin et al., Citation1995; Marina & Imam Wahjono, Citation2017). As well as encouraged by governments that all parties including government, individuals and institutions should give commitment to achieve Sustainable Development Goals (Ghoniyah & Hartono, Citation2019, Citation2020; Ogundajo et al., Citation2022, p. 2).

Corporations, as entities that utilize many current resources to obtain high profits, need to be aware of the impact not only on the economic sector but also on the environment and social sector. Looking further into the future, the company’s goal is not only to have high profits at the present time, but also to run its business in a stable and growing manner for future periods (Freeman et al., Citation2010). To create a conducive environment for a company’s sustainable growth, efforts are needed to maintain the environment itself (sustainability). To achieve sustainability, it is necessary to realize the meaning of sustainability within a broad scope.

Awareness of protecting the future has led to the concept of sustainability (Taha et al., Citation2023, pp. 1–2). Awareness of sustainability refers to individuals’ and communities’ understanding of the importance of acting and living sustainably. They pay attention to the economic, social and environmental impacts of their actions. Awareness of sustainability motivates people to adopt behaviours, lifestyles and decisions that support sustainable development goals. In other words, awareness of sustainability is an important driver in creating positive change that supports the SDGs and ensures that we achieve the sustainable development goals.

The study also support the previous research from (Pedersen et al., Citation2018; Taha et al., Citation2023) about whether corporate social sustainability could increase the corporate financial performance. In this research, the latent variable not short-term business goal such as profit, but the long-term business goal. Because business sustainability is the main goal that takes priority, namely the ability to survive until the next generation (Ghoniyah & Aryani, Citation2018).

6.2. Islamic work ethics on business sustainability

This study proves that Islamic Work Ethics can rally Business Sustainability through Sustainability Awareness (H2 is accepted). Islamic work ethics is unable enhance Business Sustainability directly, but it effectively achieve Business Sustainability through Sustainability Awareness.

The study empirically support the previous researchers (Ghoniyah, Citation2010; Marina & Imam Wahjono, Citation2017; Mohammad et al., Citation2018; Perri & Teague, Citation2022). Previous research regarding Islamic work ethics has described the appliance in the corporation, it is by organizational approach in creating a sense of ownership of the company in workers. By having self-belonging in employees, the performance of employees would improve (Marina & Imam Wahjono, Citation2017; Mohammad et al., Citation2018). The dedication of employees is a long-term asset that could uphold business continuity (Ghoniyah, Citation2010; Perri & Teague, Citation2022), especially if the employees apply the Islamic work ethic.

Islamic work ethics reflects the principles of each individual in a company. Such as stated by (Rizk, Citation2008, p. 251) that business ethics could be seen in general, while the work ethic in particular. Islamic work ethics have become the basis of certain acts. A commendable act must have a value of worship toward God (ï·² سبحانه و تعالى) through the purpose and the sincerity of intention (Akhavan et al., Citation2014; Asifudin, Citation2004, p. 93). The sincere intention based on Islamic work ethics should be reflected by employee’s commitment of their responsibility at work with all their capability (Akhmadi et al., Citation2023). Thus, Islamic work ethics are not only reflected by the excellent effort to obtain business sustainability but also the intention to accomplish the pleasure of God (ï·² سبحانه و تعالى) also as the accountability of humans as caliphs on earth. The concept is applicable to achieving sustainable development goals as the responsibility of all parties, individuals, and agencies (Central Bureau of Statistics, Citation2016; Ordonez-Ponce et al., Citation2021).

Global sustainability is a common goal and in line with the goal of Muslims to become caliphs or guardians of Earth. The effort to obtain the objective must be an impulsive deed by both the corporation and the individuals (Central Bureau of Statistics, Citation2016, Citation2018). Sustainability issues must be considered in every decision made by companies and individuals. In other words, although sustainability is the ultimate goal, actions that show that a person or agency has sustainability goals can be reflected in their daily activities such as their ethics.

Work is a way to contribute to social and spiritual well-being. The main aim of Islamic work ethics is to guide individuals in carrying out economic and work activities based on moral principles and Islamic values (Asifudin, Citation2004; Ghoniyah, Citation2010). Islamic Work Ethics emphasizes moral principles that are relevant to daily activities in the workplace, involving aspects of relationships between individuals, responsibility for work, and maintaining a balance between work life and personal life (Asifudin, Citation2004; Ghoniyah, Citation2010). Values such as honesty, integrity, and empowering individuals are included in these principles. As for constructing Islamic ethics, should use the five axioms of Islamic ethics i.e. unity (tauhid), free will, proportionality (equilibrium), responsibility, and virtue (ihsan) (Muhammad, Citation2004, p. 53).

6.3. Islamic business ethics on business sustainability

This study empirically proved that Islamic Business Ethics both directly or through Sustainability Awareness can improve a company’s proficiency to survive in the long term. This positive relationship is created through awareness of the overall long-term goals. The result is support the thought related to the purpose of humans on Earth as Khalifah (as guardians of Earth), which is aligned with the objective of sustainability (Qur’an Surah Al Baqarah 2:30) (Ghoniyah & Amilahaq, Citation2020; Jakupović, Citation2023). A person or entity that performs based on Islamic law (Islamic business ethics) should have the goal of being the caretaker of the earth and universe created by Allah. In other words, the goals were aligned with the purposes for which humans were created.

Stakeholder theory based on Islam remarks the absolute and relative right of ownership and restructures the stakeholders theory that the absolute owner of every entity in the world, while humans are the caretakers/Khalifah (relative right of ownership) (Qur’an Surah Al Baqarah 2:30) (Jakupović, Citation2023). As the intervention of Islamic rule (Al Quran) could be seen in the corporate foundation such as goals, mission, objective, and ethical values (Abuznaid, Citation2009). Thus, it is important to encouraged the importance of ethical behavior in business (Abuznaid, Citation2009; Ghoniyah & Amilahaq, Citation2020; Jakupović, Citation2023).

This study emphasizes that entities should not focus on themselves and become selfish toward their personal goals. In general, business activities increase value-added through production, trading, or service supply. The aim of this activity was to boost profits as much as possible without considering spiritual value. According to Islam, business activities not only increase material profits (Gymnastiar, Citation2006, p. 78). Process integration (with Islamic ethics) and overall business goals create positive results in the form of sustainable business. Finally, the appliance of Islamic business ethics is not an obstacle to a company in achieving sustainable business, even help it (Perri & Teague, Citation2022).

Islam guides all actions both worship and actions related to world affairs, labor, commercial, professional, and behaving regarding others and the surroundings (muamalah) (Abuznaid, Citation2009; Akhmadi et al., Citation2023; Albassam & Ntim, Citation2017). Organization with Al Quran and al Hadith as the foundation in running the business, could be seen by the corporate value that express Islamic values. Evenmore, be syntethized in company’s vision, mission, and organizational culture. Having business with Islamic principles means prioritize fairness and transparency. The fairness in business could be reflected by tyranny inexisted, while the transparency mean the business must be condected in honest way (Akhmadi et al., Citation2023; Gymnastiar, Citation2006, p. 32). Islamic principle is the proper ethics in order to attain business continuity and the sustainability, especially for corporations that put Islamic principles as the core of their value. Thus, Islamic principles must be applied to company and employee ethics (Abuznaid, Citation2009; Albassam & Ntim, Citation2017, p. 182; Elghuweel et al., Citation2017).

The empirical result of this study support previous qualitative research by Suriyankietkaew and Kantamara (Citation2019) to embracing good ethical and spiritual values would obtain long-term corporate sustainability, also support previous literature of Lashley (Citation2016) that analyzed ethics regarding sustainability. (Suriyankietkaew & Kantamara, Citation2019) believed that embracing good ethical and spiritual values would obtain long-term corporate sustainability. (Lashley, Citation2016) supported the qualitative analysis of ethics regarding sustainability, (Elghuweel et al., Citation2017, pp. 191–193) conjecture that in a predominantly Islamic country, corporate engagement could be influenced by informal Islamic religious experiences, beliefs and values, and (Ezenwakwelu, Citation2020; Kurnia et al., Citation2020; Marina & Imam Wahjono, Citation2017; Sarmawa et al., Citation2020) demonstrated how between business ethics could achieve business sustainability. Commonly, religion can be influential in business decisions and operations (Elamer et al., Citation2020, p. 915). Companies that install Islamic values in their operations and company foundations, such as implementing Islamic Business Ethics, will be more concerned with fulfilling their corporate responsibilities (Albassam & Ntim, Citation2017, p. 182; Elghuweel et al., Citation2017).

6.4. Islamic business ethics and Islamic work ethics

The results of testing Hypothesis 4 reinforced the fact that to make Islamic Work Ethics effective enough to maintain business continuity, it is essential to strengthening Islamic Business Ethics. In organizational behavior theory, employees’ actions or outcomes are based not only on their personal background but also on interventions and directions from groups and ecosystems created by the organization (Akhmadi et al., Citation2023, pp. 3–5; Robbins & Judge, 21 C.E.). Therefore, it is important for companies to encourage employees to apply ethics in accordance with their standards i.e. Islamic business ethics of Islamic companies. By having self-belonging in employees, the performance of employees would improve (Marina & Imam Wahjono, Citation2017; Mohammad et al., Citation2018). For an organization, managing human resources to form commitment and loyalty of employees is a long term investment that could uphold business continuity (Gymnastiar, Citation2006, p. 78) (Ghoniyah, Citation2010), especially if the employees apply the Islamic work ethic.

The empirical result emphasizes the role of Islamic Business Ethics in moderate Islamic Work Ethics of employees. As previous research had proved that Islamic Work Ethics was moderated by the managers or leaders support (De Clercq et al., Citation2018, p. 13). The result also support empirically toward previous researchers such as (Asifudin, Citation2004; Ghoniyah, Citation2010; Rizk, Citation2008). They stated that ethics at the corporate level become the reference to its decisions that impact others including individual within an entity.

The purpose of humans is to become caliphs on earth and to worship God (ï·² سبحانه و تعالى). This goal is in line with human responsibility to maintain ecosystem sustainability. However, the goal of business continuity is different matter. Capitalism company goals may not be in line with employees’ goals. Thus, with the same vision (sustainability goals), employees can have a significant sway on a company.

Commonly, the institution that implement Islamic business ethics well could establishes a workplace that is viable with Islamic values (Asifudin, Citation2004; Ghoniyah, Citation2010). Islamic business ethics as the foundation can encourage employees to implement Islamic work ethics as well, in line with the company’s vision and values. Thus, employee can more freely apply Islamic work behavior when the company provides support. Because as individual, employees basically are supposed to stick to Islamic guidance at every activities including working.

It is the organization’s duty to integrate Islamic values into every facet of its operations. A company’s rewards and punishments system should be integrated with its corporate ethics program, which should start at the top of the corporate hierarchy (Rizk, Citation2008, p. 248). It would be worthwhile to pursue empirical research that aims to ascertain the extent to which business affairs in Muslim majority societies align with the prescribed model, as it may yield insightful findings (Rizk, Citation2008).

Achieving global sustainability through working is in line with their role as caliph. Individual decisions will be guided by Islamic ethical principles and will be based on maximizing social welfare as well as profit (Rizk, Citation2008, p. 251). The way one approaches work is known as the Islamic work ethic, or IWE. It suggests that labor is a virtue in light of human needs and a requirement to achieve balance in one’s social and personal life. The IWE places the utmost value on business motives while standing for life fulfillment rather than life denial. The idea originated with the Qur’an, the teachings and deeds of Prophet Muhammad, who taught that righteousness was gained through labor and that sins could be forgiven. It also came from the legacy of the four rightly guided Caliphs who ruled the Islamic nation following the prophet’s death (Rizk, Citation2008, p. 251).

7. Summary and conclusion

In summary, sustainability awareness can affect business sustainability; Islamic Work Ethics can affect business sustainability through sustainability awareness; Islamic Business Ethics can affect business sustainability directly and through sustainability awareness; and Islamic Business Ethics can moderate Islamic Work Ethics on Business Sustainability either directly or through sustainability awareness. Thus, it can be concluded that the four research hypotheses were received.

The contribution of this study is that sustainability objectives within the scope of a business can be described as action or sustainability awareness. The relationship between business sustainability and sustainability could be described by two separate factors. Therefore, there will be no confusion in the future between a company’s goals to be sustainable and the global goals of sustainability. The study also used primary data, which could become another way of completing research using secondary data, as has been done by previous researchers.

Sustainability orientation and the proper business strategy using Islamic ethics are essential in achieving business sustainability. The orientation of sustainability is aligned with the aims of humankind as caliph on earth. In contrast, Islamic ethics in business and work is aligned with the comprehensive method of an entity in achieving goals. This research proved that sustainability goal awareness is required to achieve business sustainability, and holistic ethics (Islamic business and work ethics) must be applied. Finally, the application of business ethics and sustainability awareness goals can help maintain, and even increase, business sustainability. In other words, corporate especially Islamic corporations/institutions should be confident to express their worship and caring among others, and not afraid of being bankrupt because of it.

7.1. Future research agenda

This study focuses on Islamic institutions, both profit-oriented and non-profit-oriented. Therefore, the Business Sustainability Performance indicator does not involve indicators such as profit for three consecutive years, market share development, or sales development (Hassan et al., Citation2021, p. 1610; Li et al., Citation2020). This study develops existing theories, including indicators and business sustainability perspectives. Therefore, future research could use secondary data to gain a more thorough understanding of business sustainability.

This study only used foundation factors (Islamic Ethics) in achieving sustainability awareness and business sustainability. In fact, reforming business strategy is well known in keeping the corporation stay long. Thus, future quantitative research involving business strategic, intellectual capital, and innovation (Antwi-Boateng et al., Citation2023, p. 14; Mannan et al., Citation2016) as important factor in achieving business sustainability, perhaps towards sustainability awareness also.

Author contributions

Here we stated that all the author were involved in providing the article on all progress and to be accountable for all aspects of the work. The concept and design proposed by First Author with Third Author, moreover business sustainability has been the concern in 2018. The Islamic ethics also has been studied by First Author since dissertation research conducted in 2008. The indicators that reflect each variable were discussed intensively together by the three authors. Then, the Second Author obliged to coordinate with targeted Islamic Institution, deciding the method design, distribute and collecting the data, and running it. The result were discussed to get proper and comprehensive interpretation. In conclusion, all the authors give the final approval of the version to be published.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Nunung Ghoniyah

Nunung Ghoniyah is a professor in Faculty of Economics, Universitas Islam Sultan Agung (UNISSULA), also an assessor of the National Accreditation Board for Higher Education in Indonesia. Actively teaching undergraduate, postgraduate, and PhD students. Every year join community services in Indonesia and Malaysia for Micro, Small and Medium Enterprises (MSME). As for the research interests are in business management for SMEs, finance, economics, Islamic banking, and Islamic Business Ethics. Sustainable Development Goals (SDGs) are the current issue that must be encouraged by Islamic institutions. The current study found that achieving the Global Sustainable Goals must be seen by the proper ethic. Morover, concerning global goals should be balanced by the capability to sustain the business.

Farikha Amilahaq

Farikha Amilahaq is an assistant Professor. Active as lecturer and research assistant at the Universitas Islam Sultan Agung (UNISSULA) since 2019. As for the interest in writing and researching with the themes of Islamic Finance, Islamic Financial Planning, Islamic Financial Management, also islamic non profit organization.

Sri Hartono

Sri Hartono is an associate professor at the Economics Faculty, UNISSULA. He also an assessor of the Independent Accreditation Institute for Economics Business Management and Accounting in Indonesia. Interest in financial management, business feasibility studies, business budgeting, and management accounting. His current research is the effectiveness of corporate governance in increasing the Maqashid Shariah index of Islamic Banking.

References

- Abdelnaeim, S. M., & El-Bassiouny, N. (2021). The relationship between entrepreneurial cognitions and sustainability orientation: The case of an emerging market. Journal of Entrepreneurship in Emerging Economies, 13(5), 1–23. https://doi.org/10.1108/JEEE-03-2020-0069/FULL/XML

- Abuznaid, S. A. (2009). Business ethics in Islam: The glaring gap in practice. International Journal of Islamic and Middle Eastern Finance and Management, 2(4), 278–288. https://doi.org/10.1108/17538390911006340

- Akhavan, P., Ramezan, M., Yazdi Moghaddam, J., & Mehralian, G. (2014). Exploring the relationship between ethics, knowledge creation and organizational performance. VINE, 44(1), 42–58. https://doi.org/10.1108/VINE-02-2013-0009

- Akhmadi, A., Hendryadi, Suryani, Sumail, L. O., & Pujiwati, A. (2023). Islamic work ethics and employees’ prosocial voice behavior: The multi-role of organizational identification. Cogent Social Sciences, 9(1), 1–13. https://doi.org/10.1080/23311886.2023.2174064

- Al-Abbadi, L. H., & Abu Rumman, A. R. (2023). Sustainable performance based on entrepreneurship, innovation, and green HRM in e-business firms. Cogent Business & Management, 10(1), 1–15. https://doi.org/10.1080/23311975.2023.2189998

- Al-Faouri, A. H. (2023). Green knowledge management and technology for organizational sustainability: The mediating role of knowledge-based leadership. Cogent Business & Management, 10(3), 1–15. https://doi.org/10.1080/23311975.2023.2262694

- Albassam, W. M., & Ntim, C. G. (2017). The effect of Islamic values on voluntary corporate governance disclosure: The case of Saudi-listed firms. Journal of Islamic Accounting and Business Research, 8(2), 182–202. https://doi.org/10.1108/JIABR-09-2015-0046/FULL/XML

- Ali, A. J., & Al-Kazemi, A. A. (2007). Islamic work ethic in Kuwait. Cross Cultural Management, 14(2), 93–104. https://doi.org/10.1108/13527600710745714

- Ali, A. J., & Al---Owaihan, A. (2008). Islamic work ethic: a critical review. Cross Cultural Management, 15(1), 5–19. https://doi.org/10.1108/13527600810848791

- Amilahaq, F., & Ghoniyah, N. (2019). Compliance behavior model of paying Zakat on income through Zakat management. Share: Jurnal Ekonomi Dan Keuangan Islam, 8(1), 114–141. https://doi.org/10.22373/share.v8i1.3655

- Antwi-Boateng, C., Mensah, H. K., & Asumah, S. (2023). Eco-intellectual capital and sustainability performance of SMEs: The moderating effect of eco-dynamic capability. Cogent Business & Management, 10(3), 1–18. https://doi.org/10.1080/23311975.2023.2258614

- Arianpoor, A., & Salehi, M. (2021). A framework for business sustainability performance using meta-synthesis. Management of Environmental Quality, 32(2), 175–192. https://doi.org/10.1108/MEQ-03-2020-0040/FULL/PDF

- Arvidsson, S. (2022). CEO talk of sustainability in CEO letters: towards the inclusion of a sustainability embeddedness and value-creation perspective. Sustainability Accounting, Management and Policy Journal, 14(7), 26–61. https://doi.org/10.1108/SAMPJ-07-2021-0260/FULL/PDF

- Asifudin, A. J. (2004). Etos Kerja Islami. Muhammadiyah University Press.

- Asriati, N., Syamsuri, S., Thoharudin, M., Fitria Wardani, S., & Halim Perdana Kusuma Putra, A. (2022). Analysis of business behavior and HRM perspectives on post-COVID-19 SME business sustainability. Cogent Business & Management, 9(1), 1–21. https://doi.org/10.1080/23311975.2022.2115621

- Balkis Binti Mohd Yusof. Q., Saadah Binti Md Yusof, N., & Bin Abbas, R. (2017). the Effect of Islamic work ethics on job satisfaction in organization; a study in Sekolah Rendah Islam Indera Mahkota (Sri Abim), Kuantan. Journal of Global Business and Social Entrepreneurship, 1(3), 46–61.