Abstract

The purpose of this study was to investigate the mediation effect of organizational innovation in the relationship between total quality management and business financial performance. The study used a quantitative approach with descriptive and explanatory design. The coffee processing industries were selected based on the type of coffee that they are processing. 334 respondents were involved in the survey using a systematic simple random sampling technique. Descriptive statistical tools frequency distribution, percent, mean and standard deviation were used for analyzing demographic variables. Similarly, the structural equation model was utilized for confirmatory and path analysis. The findings of the study revealed that total quality management has significant and positive effects on business financial performance. Similarly, the results affirmed that organizational innovation partially mediates the relationship between total quality management and business financial performance. The study was limited to the coffee processing industries. Therefore, generalizing the result to other sectors may be questionable and thus, future studies might include other organizations. Similarly, the study was conducted using quantitative data only and further study needs triangulation of results with qualitative data. Overall, the study provided crucial empirical evidence to coffee processing industries, for researchers, academicians and firm managers.

Reviewing Editor:

1. Introduction

Currently, in the business arena, there is a shift from the quality concept to the quality management approach called Total Quality Management (Aigbavboa, Citation2019). Quality is the perceived characteristics that can express the ranks and degrees of the superiority of a given object (Bagga & Haque, Citation2020) whereas Total Quality Management (TQM) is a holistic management approach that helps to ensure business performance in every aspect (Addis, Citation2020; Jimoh et al., Citation2019).

Total quality management (TQM) is a strategic management (Shafiq et al., Citation2019) that has been given a top priority in business and research. TQM ensures the pattern of competition in the business by improving overall firm performance (Othman, Citation2020). It is the central and effective strategy to ensure the firm’s productivity and profitability (Ahaotu, Citation2019; Nazar et al., Citation2018). Besides, TQM strengthens the link between business performance and management philosophy and plays an important role in keeping the business competitive (Muhammad Zakki, Citation2021).

The study by Yusliza et al. (Citation2019) stated that organizations can meet their goals if TQM practices and innovation are implemented appropriately. According to the evidence of various previous studies (Ahmad et al., Citation2018; Esiaba, Citation2016; Ganapavarapu & Prathigadapa, Citation2015; Hamdan & Alheet, Citation2021), the proper implementation of TQM can improve the quality of the product and service performance to give a guarantee to the financial performance which helps to be ahead of the competitors.

However, many business organizations in developing countries including Ethiopia are facing challenges in implementing TQM due to low awareness levels regarding its concept (Gebregergs, Citation2019; Pengaruh et al., Citation2020). Although, organizations in developing countries are facing challenges in properly implementing TQM, its role in increasing business performance received more attention and thus, several business sectors in a developing country, in particular Ethiopia had shown their interest to implement TQM, especially manufacturing, service and educations sectors (Ahaotu, Citation2019; Gebregergs, Citation2019; Keinan & Karugu, Citation2018, Worlu & Obi, Citation2019; Chen et al., Citation2020). Conversely, in Ethiopia, only scanty literature was reported on TQM implementation in the coffee industry (Gezahegn Tegegne, Citation2020).

Similarly, innovation is another driver to ensure business performance in particular when incorporated with TQM (Bazrkar et al., Citation2022). Innovation refers to doing business with different procedures or methods aiming to increase efficiency, effectiveness and competitiveness (Antunes et al., Citation2017; Lian et al., Citation2020; Suleiman Abu-Mahfouz, Citation2019). Besides, it is the process of introducing new ideas, services or products to customers and markets to dominate the market (Antunes et al., Citation2017). Innovation ensures the performance and competitive advantage of the business (Othman, Citation2020).

Currently, due to the rapid increase of competition in the market, organizations need to produce their product in innovative ways. In this way, the coffee processing industry needs to ensure the quality of their product that meets the satisfaction level of the customers. Therefore, the coffee industry should apply innovation in line with TQM to improve performance (Antunes et al., Citation2017). Among many types of innovative practices (such as product/service, process, organizational and technological), this study focuses on organizational innovation because its central role is linked to management issues who are responsible for managing the overall performance of the firm (Suleiman Abu-Mahfouz, Citation2019).

Organizational innovation was introduced as a management core, and it pertains to organizational structure, administrative systems and human resources (Andrade de Oliveira et al., Citation2020). It involves procedures, rules, roles and structures that are related to the overall organizational structures. Organizational innovation works on improving organizational structure or management that can improve the entire performance of the firm rather than being involved in a routine activity (Antunes et al., Citation2021).

Ethiopia has different factors that drive investments in the coffee sector (which are the large coffee-producing potential, the presence of organic coffee and the interest of the international market in buying organic coffee (Howard, Citation2018; Jalata, Citation2021; USDA, Citation2020). For example, the recent report by Hundie and Biratu (Citation2022) indicates the demand for Ethiopian coffee in the world market has risen. These opportunities are the driving engine for Ethiopia to produce and supply a sufficient amount of coffee products to the world market (Hundie & Biratu, Citation2022). However, the disposition of competing and performing competitively is low because organizations still traditionally doing business (El-Daghar, Citation2018). To ensure the performance of the coffee sector there is a need to apply the newly emerged concept called organizational innovation in alignment with TQM to secure the business in all aspects (Ababa, Citation2020).

Although studies have been conducted on the relationship between TQM and business financial performance, there were inconsistent results on the relationships. The Study by (Kebede Adem & Virdi, Citation2021; Alzeaideen, Citation2019) reported that some of the TQM practices have no significant effect while the studies conducted by (Do et al., Citation2020; Nguyen et al., Citation2016; Suleiman Abu-Mahfouz, Citation2019) reported positive relationship. The contradictory literature evidence leads the researcher to examine the relationship between TQM practices and business financial performance. Similarly, this study has incorporated the third variable; organizational innovation that can strengthen the relationship between TQM and financial performance as well as their effects on the performance of the coffee industry. Therefore, this study aimed to examine the relationship between TQM and business performance through organizational innovation referencing the coffee processing industries in Guji Zone, Ethiopia. This study contributes to bringing consistent results and enhances the academic understanding of the relationships among TQM, organizational innovation, and firm performance by bridging the gaps in the existing literature, theory, and practice, and providing empirical evidence and practical recommendations to the coffee processing industry in Ethiopia.

2. Related literature review

2.1. Theoretical background

The researchers have applied the resource-based theory to link business performance with the application of TQM in the coffee processing industry.

2.1.1. Resource-Based view theory

Nowadays, business organizations are showing their interest in implementing TQM practices. The application of TQM practices can improve a company’s competitiveness and business benefits by increasing a firm’s financial performance (Chen et al., Citation2020; Culture, Citation2019; Karyamsetty, Citation2021; Saad et al., Citation2020).

Resource-based theory evaluates the firm’s capability against competitors focusing on better resource utilization and maximization of the level of competitive advantage (Birger, Citation1982; View, Citation2022). A resource-based theory is an approach that helps the business to strategically identify the strengths and weaknesses in and outside the organization, and the ability to fill the identified gaps within the market (Lockett et al., Citation2009; Kozlenkova et al., Citation2014). For the firm to be ahead of the competitors and get a competitive advantage over them there is the need to improve overall business activities such as financial, operational and workforce performance (Nyaribo, Citation2022).

The resource-based theory works on effective resource management to meet customer needs and supports strategic analysis of business strengths and weaknesses by improving business processes and services (View, Citation2022; Kor & Mahoney, Citation2000; Barney et al., Citation2001) while the implementation of TQM has a linear relationship with business performance (Liu et al., Citation2021; Suleiman Abu-Mahfouz, Citation2019).

Based on the literature reviewed the resource-based theory is about gaining more competitive advantage through the proper implementation of TQM practices which improve the overall organizational performance (View, Citation2022). Besides, RBV and TQM support each other in improving the performance of the firm. Therefore, this study will link the concept of TQM to the resource-based theory (RBV) to examine the effect of TQM practices on business performance within the coffee processing industry in Guji Zone, Ethiopia.

2.2. Empirical study evidence

2.2.1. Total quality management (TQM)

TQM is an enabling factor in the organization that integrates the roles and sets up the operations procedures of the business (Othman, Citation2020). The implementation of TQM ensures the business’s competitive advantage by enhancing the performance of the organization (Aigbavboa, Citation2019). Besides, Zou and Fan (Citation2022) contended that TQM is the business’s internal and external cultural phenomenon of perceived quality-based guidelines and principles that are rooted within the values, mission and vision of the business.

To get the maximum benefits of TQM, companies should determine the practices that have been identified and theorized by quality gurus. Identifying the exact TQM constructs is a complex phenomenon that requires a rigorous literature review to agree on the best-fit practices. Yet, no agreements were reached on which TQM constructs and how many of them are applicable for which organization still needs investigation.

Several constructs were applied by researchers to analyze the implementation of TQM. Some researchers consider more or fewer constructs than others depending on their contexts of studies. For example, (Suleiman Abu-Mahfouz, Citation2019; Yas et al., Citation2021) conducted their study using three (3) constructs whereas the study by Ukab (Citation2021) and Keinan and Karugu (Citation2018) used four (4) constructs.

Moreover, authors such as (Essel, Citation2020; Zakuan et al.,Citation2010; Nguyen et al., Citation2016; Baidoun et al., Citation2018; Ooi, Citation2009; Suleiman Abu-Mahfouz, Citation2019; Puthanveettil et al., Citation2021; Agus et al., Citation2010; Kebede Adem & Virdi, Citation2021) have implemented different constructs in various aspects where constructs used differed from one another in number depending on the nature of the study. Several TQM literature that have been reviewed have applied at least three or more constructs. Based on this literature evidence, the authors of the present study agreed that the number of constructs parse does not matter as such and thus, the focus should depend on the objective and nature of the study. For this study, the researchers have chosen the constructs that are commonly used in many studies and those which were very relevant to the nature of the study’s context.

Therefore, among other accepted TQM constructs, the four (top management commitment, customer focus, communication and information analysis, and continuous improvement) are frequently used in the literature. With this in mind, the researchers decided to apply them believing that they can explain the TQM implementation and best work with the nature of the study and research objectives.

2.2.2. Top management commitment

One of the main success factors for enhancing the performance of the business is management commitment. Top management commitment was well documented in the European Foundation for Quality Management (EFQM) and Malcolm Baldrige National Quality Model (MBNQA) as the best success factors of TQM implementation (Nyeadi et al., Citation2021). TQM studies indicate that top managers can motivate people to make voluntary commitments to achieve or exceed organizational goals, and continuously improve the work processes and product or service quality (Ilyas et al., Citation2020). TQM encourages collaboration among top management commitment and subordinates to fulfil the organizational mission (Najm et al., Citation2017; Jimoh et al., Citation2019). Overall, the assumption about having strong management in the organizations is used as an agent to promote a high-quality culture that helps to improve customer satisfaction (Zou & Fan, Citation2022).

2.2.3. Customer focus

Customer focus is the priority of the TQM organization (Nasim et al., Citation2020). Ukab (Citation2021) stated that quality is not determined by the organization or manufacturer of the product; it is determined by the customer whether the organization strives to control or produce the quality product (Nyeadi et al., Citation2021; Othman, Citation2020; Ahmad et al., Citation2018). With the rapid increase of competition in the competitive business environment, customer focus and customer relationships determine how a business concentrates on customer satisfaction which gives the business a competitive advantage (Suleiman Abu-Mahfouz, Citation2019; Yusufu, Citation2018).

In the TQM process, the customer is the superior stakeholder of the organization (Nyaribo, Citation2022). Organizations must adjust their strategies and plans to the expectations and needs of the customer using their feedback and suggestions as input (Sciarelli et. al, 2020). In general, customer focus increases customer satisfaction which can contribute to the performance of the business. Thus, the organization’s customer satisfaction can be measured by listening to the organization’s feedback and complaints and providing immediate responses to their queries (Khaled Alharbi & Al-Matari, Citation2016).

2.2.4. Communication and information analysis

In the business context, communication is the process of exchanging information about the business between stakeholders inside and outside the company (Chauke et al., Citation2019). Communication is one of the basic skills needed by managers (Karyamsetty, Citation2021). Effective business communication is about how employees and management interact to improve business practices through reducing errors (El-Daghar, Citation2018; Karyamsetty, Citation2021). Overall, effective communication and information analysis is the tool that helps the management to teach, discuss and explain the overall information about the organization including the existing situation and plans of their business (Khalid Alharbi et al., Citation2016). Thus, firms need to obtain important and relevant information to make the right decision for their business to secure long-term success (Khalid Alharbi et al., Citation2016).

2.2.5. Continuous improvement

Continuous improvement is a planned, organized and systematic process that continuously, gradually and extensively changes current practices of business to be improved (Alaoun & Faculty, Citation2018). The main focus of continuous improvement is to advance productivity and business performance (Menza & Rugami, Citation2021). Continuous improvement needs to be made at the top management, middle, operational and individual levels of the organization (Shafiq et al., Citation2019). The effect of continuous improvement at the management level is embedded in the organizations for strategy establishment (Saud, Citation2019). Continuous improvement should take part at every stage of Deming’s cycle i.e. planning; doing, controlling and action levels (Gómez et al., Citation2017). Finally, to achieve organizational goals, industries must conduct a series of continuous improvements on human and non-human activities, production processes and service delivery of their business (Worlu & Obi, Citation2019).

In summary, the above-discussed four TQM constructs have been widely recognized, frequently used in several literatures and proven to be the key to successful TQM implementation across various industries (Puthanveettil et al., Citation2021; Agus et al., Citation2010; Antunes et al., Citation2021; Chaudhry & Bilal, Citation2018). Therefore, by emphasizing the TQM practices, the coffee processing industry can foster a culture of quality, empower employees, enhance customer satisfaction, and achieve sustainable performance excellence. Accordingly,

H1: Total Quality Management (TQM) significantly affects business financial performance.

2.2.6. TQM and organizational innovative practice

Innovation encompasses the redesigning, creation, and implementation of novel organizational structures that add value to firm performance (Nyaribo, Citation2022). It involves costs that can be considered investments by the organization since innovation allows the creation of new and advanced products, enhancing the company’s competitiveness (Menza & Rugami, Citation2021). The goal of innovation is to bring about significant improvements within the firm, which is why this study focuses on organizational innovative practice.

Organizational innovative practice refers to the adoption of new and improved ways of doing things, as well as generating ideas and fostering creativity to enhance business performance (El-Daghar, Citation2018). Previous research has examined the relationship between Total Quality Management (TQM) and business performance, highlighting its significance (Suleiman Abu-Mahfouz, Citation2019). In particular, a study conducted by Sciarelli et al. (Citation2020) reported a direct and significant effect of TQM on business financial performance, prompting further investigation into the indirect relationship between TQM and business financial performance through the inclusion of a third variable. Therefore, the present study aims to explore the role of organizational innovative practices as a mediator in the relationship between TQM and business financial performance. Thus,

H2: TQM has a significant effect on organizational innovative practice (OIP).

2.2.7. Organizational innovative practice and business financial performance

An organization is an entity established for a common goal that consists of human elements, and physical and capital resources (Suleiman Abu-Mahfouz, Citation2019). What constitutes an effective business depends on how the business measures its performance (Do et al., Citation2020; Nguyen et al., Citation2016). Bazrkar et al. (Citation2022) pointed out that different measures are suitable for different business performances. These measures include effectiveness, efficiency, financial viability and relevance to stakeholders (Ahaotu, Citation2019). According to Herzallah et al. (Citation2014) organization performance should encompass three specific areas financial performance, product market performance and shareholder return. For this study, the focus is on the financial performance of the business.

Financial performance is a well-known measurement of the business (Nguyen et al., Citation2016). Many scholars have agreed that to evaluate firm performance, the organization should focus on financial performance which is about measuring the profits, return on assets, return on investment and so on (Alzeaideen, Citation2019). Different researchers (Karyamsetty, Citation2021) supported the notion of the measurement of financial performance basically as profit, sales, growth, and market results. Moreover, others advocated for some specific measures, for instance: return on investment, return on assets and cash flow (Anggadini et al., Citation2021; Lassala et al., Citation2017; Albuhisi & Abdallah, Citation2018).

Positioning the innovative practice in the coffee processing industry increases the business financial performance of the firm (Zafer Acar, Citation2020). This study assesses the effect of organizational innovative practice in line with business activities and events that contribute to customer value and the long-term success of coffee processing companies in the Guji zone. Therefore,

H3: Organizational innovation has a significant effect on business financial performance

2.2.8. The relationship between TQM practices, organizational innovation and business financial performance

In today’s highly competitive business landscape, organizations strive to gain a competitive advantage over their rivals (Bazrkar et al., Citation2022). Improving performance is crucial for businesses to ensure their long-term survival in the market (Menza & Rugami, Citation2021). Two key factors underlying business performance are Total Quality Management (TQM) and organizational innovation (Ali Raza et al., Citation2020). TQM is a widely recognized approach that establishes standardized processes to enhance business profitability and financial performance (Anggadini et al., Citation2021). Implementing TQM within an organization has been shown to improve business performance (Chaudhry & Bilal, Citation2018).

Similarly, organizational innovation enables companies to swiftly adapt to changes in the competitive environment, discover new products and markets, and shield themselves from unstable situations (Albuhisi & Abdallah, Citation2018). To enhance performance, organizations are advised to implement both organizational innovation and TQM practices in harmony (Zafer Acar, Citation2020). Furthermore, Kim (Citation2016) asserts that the purpose of implementing TQM and organizational innovation in the business sector is to assess an organization’s successful performance over a specific period and to enable the achievement of desired goals through the correct approach.

Considering these points, it is crucial for coffee processing companies to effectively implement TQM practices and incorporate organizational innovation to improve business financial performance and ensure their long-term viability in the market. Thus, this study emphasizes the mediating role of organizational innovation in the relationship between TQM and business financial performance. Accordingly,

H4: Organizational innovation mediates the relationship between TQM and business financial performance.

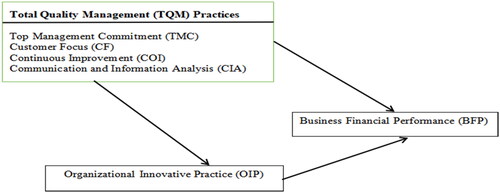

Overall, the conceptual framework for the study is presented in .

Figure 1. The conceptual framework for the study.

3. Research methodology

The study followed a quantitative approach that applied descriptive and explanatory research design. The population for the study was a coffee processing industry found in the Guji zone, Ethiopia. The sample frame for the study is owners, general managers, department heads and operation managers. The industry was clustered based on the nature of the coffee products they are processing as wet and dry processing.

In total, 365 representative samples were drawn from both clusters using systematic simple random sampling. A systematic simple random sampling technique was used because of the homogeneity of the population. The questionnaire was distributed to 365 respondents and only 342 questionnaires were collected back. Out of the 342 questionnaires, 8 (eight) copies of the questionnaire were filled wrongly and thus, excluded from analysis following the data validation process. Therefore, a total of 334 (91.5%) questionnaires were active for data analysis.

Data were gathered through the survey questionnaire. A survey questionnaire was adapted (Azam et al., Citation2023; Anastasiadou, Citation2015; Antunes et al., Citation2021; Baidoun et al., Citation2018; Sciarelli et al., Citation2020; Khalfallah et al., Citation2021). below shows the details of item descriptions and their sources where they were adapted from.

Table 1. The description of the constructs’ and its sources.

A pilot test was conducted before the final data collection to make questions suitable for respondents and the coffee processing industry nature. Based on the feedback of the pilot test, some adjustments were made to the survey questionnaire. For example, some texts were paraphrased to make them clearer.

Researchers handled the issues of common method bias (respondent and non-respondent bias) using different strategies. To ensure representatives of the population, a sample size determination formula with a proportional rate was used. Besides, random probability sampling was applied to select respondents from the selected sampling frame where every member was given equal chances to participate in the study. Moreover, the researchers analyzed the backgrounds of the non-respondents. They were scattered among different categories of respondents. Indeed, because of the researchers’ close supervision, the ratio of non-respondents was few compared to those who gave responses to the survey. Given the few number of non-respondents and their spread, the researchers are convinced non-response could not have made much difference to the overall study results or findings. Therefore, researchers have concluded that potential bias was handled and there is no concern in this regard.

The background information of the respondents was analyzed using means, standard deviations, frequency distributions and percentages. Similarly, structural equation modelling (SEM) was utilized for confirmatory and path analysis through stata 14 versions of statistical application software. In the study, TQM practices were measured using 20 items while each organizational innovation and business financial performance was assessed using 3 items. A five-point Likert scale was used to mark the respondents’ level of agreement. Respondents were asked to rate their level of agreement with the statements provided on the scale, which ranged from 1 (strongly disagree) to 5 (strongly agree).

4. Data analysis and interpretations

4.1. Demographic characteristics of the respondents

Descriptive statistics in a research study give brief descriptions of the study. This study presents the description of basic background information of the respondents such as gender, age, level of education, position they have in the company, length of time they worked for the company and type of the company they are working for.

The industry was classified as wet and dry coffee processing based on the type of coffee they process. The respondents who took part in this study were taken from both wet and dry categories. A total of 334 active respondents 221 (66.17%) and 113 (33.83%) from wet and dry coffee processing firms respectively participated in the study as shown in below.

Table 2. Descriptions of respondents’ background information.

The background information of the respondents such as gender, level of education, the position they had in the company and the type of the company the respondents worked for was analyzed using frequency distribution and percent while the age and experiences of the respondents were described through mean and standard deviation. The details of the respondents’ backgrounds are shown in below.

The results in above show that, out of the 334 sampled respondents, 138 (41.32%) were female and 196 (58.68%) were male. The report shows that men were more involved in the coffee processing industry in the Guji zone than female respondents. With regards to the highest level of education that the respondents count, the majority of respondents were diploma/level with the frequency of 130 (38.92%) followed by bachelor’s degree holders which are 124 (37.13%) while grades 1 to 12 accounted for 70 (20.96%) and master’s degree holders were only 10 (2.99%). From these results, it is concluded that the majority of the employees working in the coffee processing industry in the Guji zone are professionals those certified diploma/level which is about 130 (38.92%) while the master’s degree holders were the least with only 10 (2.99%). Therefore, coffee processing industries in the Guji zone were predominantly occupied by diploma/level certified professionals while master’s degree holders’ involvement was the lowest. Similarly, comparing respondents from wet and dry-type coffee processing sub-industries, 230 (66.7%) and 115 (33.3%) were from wet and dry-type sub-industries respectively.

Similarly, in the study, there were 38 (11.38%) owners out of which 3 and 35 individuals were female and male respectively, and 36 (10.78%) general managers were 12 females and 24 males. Additionally, 104 (31.14%) heads from departments of (quality management, production team, sales and marketing, finance and HR directors) 43 and 61 females and males respectively) and 156 (46.71%) operational workers out of which 80 were females and 76 were males) were reached.

On average, the workers working in the coffee processing companies in the Guji zone had a mean age of 34.32036 and a standard deviation of 7.093693. There was a difference in age group. The minimum age of the respondent was 22 and the maximum was 56. On the other hand, as presented in above, the length of work experiences of the respondents in the coffee processing companies included a minimum of 1 year and a maximum of 20 years of working experience. The average work experience accounted for about 6.296407 years while the standard deviation was 3.171597 which suggested that most employees in the coffee processing firms in the Guji zone had about an average of 6 years of work experience.

4.2. Confirmatory factor analysis (CFA)

A CFA confirms the validation of the convergent (AVE) and discriminant validity and similarly tests the composite reliability of the measurement model before the inferential analysis (Wagimin et al., Citation2019).

Convergent validity indicates the average of variance extracted (AVE) among the group of variables concerning the variance shared with errors from measurement. It is calculated from standardized loadings and measures to what extent the given items have explained the given concepts (Wagimin et al., Citation2019). When the value of AVE is equal to 0.5 or greater, these sets of items have an adequate convergence in measuring the concerned construct (Awang, Citation2014). The AVE results of this study, as shown in below, ranged from 0.54 to 0.61 while the discriminant validity ranged from 0.73 to 0.78.

Table 3. Test of validity and reliability of measurement model for TQM constructs, OIP and BFP.

Reliability is another concern to be confirmed whenever using a structural equation model. below presents the composite reliability and Cronbach’s alpha values of the measurement model. The alpha values for all measured items fall between the ranges of 0.82 and 0.87 while the composite reliability ranged from 0.81 to 0.90. Similarly, for the discriminant validity, all the covariance among each corresponding construct did not exceed the square root of AVE which indicates no discriminant validity issue within the constructs used. Therefore, it fulfilled the discriminant validity criteria. below shows the details of the validity and reliability of the data.

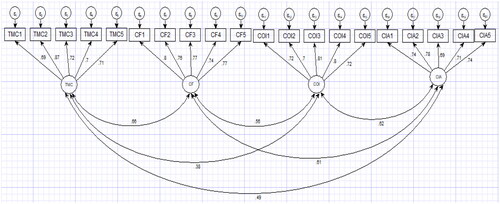

below shows the factor loadings for each item measuring TQM constructs. Results show that all measured items explaining TQM constructs have factor loadings equal to and greater than 0.69.

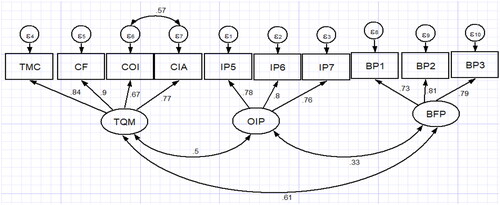

Figure 2. Measurement model for measuring TQM constructs.

Based on the evidence of results shown in and , and , it was seen that the validity and reliability of the data were affirmed where the smallest threshold values are 0.5 for AVE and 0.7 for alpha values (Wagimin et al., Citation2019). Furthermore, below shows that all factor loadings are greater than 0.75 which is greater than the critical cut value of 0.6 (Awang, Citation2014).

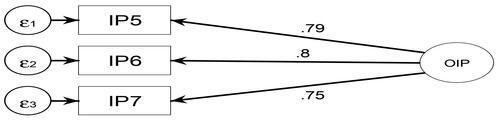

Figure 3. Measurement model for measuring organizational innovation practice.

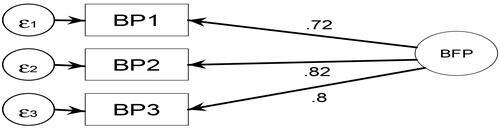

indicates the factor loadings of BFP, having loadings equal to or greater than 72 which is above the cut point.

Figure 4. Measurement model for measuring business performance.

Overall, depending on the results of , there is no violation of the validity and reliability of the data. Therefore, it was concluded that the data was valid and reliable.

4.2.1. The combined latent variables confirmatory factor analysis

Researchers have analyzed the CFA for every measurement model in this study separately. However, the suggestion by Wagimin et al. (Citation2019) claims that authors should confirm the pooled analysis of the constructs to reduce the errors that may occur during model fitness evaluation if calculated from a single construct. In the combined CFA model, all constructs are combined and evaluated for fitness in below.

Figure 5. Measurement model of combined cfa for all latent constructs.

Upon using combined CFA, researchers can easily manage model specification since there is a chance to increase the degrees of freedom for the model. For the measurement model to meet the convergent validity and composite reliability, the loadings factor of each construct > 0.6 (Wagimin et al., Citation2019) is recommendable. The results in show that all items combined have factor loadings greater than 0.67 that exceed the minimum threshold value. below shows the combined CFA for all latent constructs included in the study.

Table 4. Analysis of CFA for combined latent variables of the study.

For the AVE of the construct, the acceptable value is 0.5 where the alpha value equals to or greater than 0.7 shows internal consistency (Hafiz et al., Citation2013). The combined CFA results for all study constructs shown in the table have no violation of validity and reliability criteria. Hence, they are valid and reliable.

4.3. The evaluation of measurement model fitness and summary

For this study, among several models, the goodness of fit for CMIN/DF, RMSEA, CFI, TLI and SRMR were checked which are the basic Models. According to (Phakiti et al., Citation2018), RMSEA values ≤ 0.05 can be considered a good fit, values between 0.05 and 0.08 is an adequate fit, and values between 0.08 and 0.10 as a mediocre fit, whereas values > 0.10 are not acceptable. Comparative fit index (CFI) and Trucker-Lewis Index (TLI) are indices that determine the fitness of the model. For the values of CFI and TLI greater than 0.95, the model is said to be a good fit and values 0.90 or above are considered an acceptable fit (Wongsansukcharoen & Thaweepaiboonwong, Citation2023). Similarly, standardized root mean squared residuals (SRMR) having a value less than 0.05 indicate a good fit, for the values falling between 0.05 and 0.08 suggested an acceptable fit (Wagimin et al., Citation2019). below shows the result and decision made.

Table 5. The evaluation of measurement model goodness of fit.

The chi-square value (X2) and degree of freedom (DF) for the model are 91.51 and 31 respectively and then CMIN/DF 2.95 which is less than the critical value in the table. Similarly, the RMSEA was seen at 0.076 showing adequate fit. All the values of CFI, TLI and SRMR seen in have fulfilled the minimum required model fitness assumptions (Phakiti et al., Citation2018). Therefore, from these results, it was concluded that the model is fitted for good.

4.4. Path analysis and hypothesis testing

A structural model is a path estimate measuring to which extent the structural relationships between variables in a study are significant (Wagimin et al., Citation2019). The test of the structural model can be carried out after checking the validity of the measurement models (Awang, Citation2014). Accordingly, the overall validity of variables and model fitness was tested and has shown valid results and fit for proceeding to the structural model analysis. shows the path model of the study.

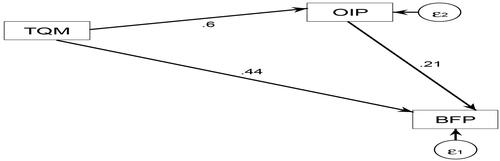

Figure 6. Path/structural model.

The standardized regression weight estimation seen in shows the causal effects among variables. Therefore, from the results of the path analysis model, it was concluded that there exists a relationship between TQM, organizational innovation and financial business performance where all the regression weights among variables were positive. The detailed analysis of the standardized effect is presented in .

Table 6. Test for mediation effect.

4.5. Mediation analysis

The mediation analysis was done by treating TQM as independent, financial business performance as dependent, and organizational innovation as mediator variables. The mediation analysis is based on the analysis of indirect effects based on the guideline by Baron and Kenny (Citation1986) applying SEM using stata 14 versions statistical software. The results are presented in below:

In the Table above, the direct effect of TQM on business financial performance was significant (β = .441, p < 0.001). Therefore, H1 was supported. Similarly, the direct effect of TQM on organizational innovation was significant (β = .599, p < 0.001). Therefore, H 2 was supported.

The direct effect of organizational innovation on business financial performance was significant (β = .212, p < 0.001). Therefore, H3 is supported. Finally, the last hypothesis of the study the mediation effect of organizational innovation in the relationship between TQM and business financial performance was significant (β = .127, p < 0.001). Therefore, H4 was supported.

In summary, the empirical evidence of this study shown in gives support to accept all hypotheses proposed in the study.

4.6. Discussion of results

The study aimed to examine the relationship and effects of TQM on business financial performance through a mediation role of organizational innovation. This study has proposed four hypotheses having three direct effects and one with a mediation role. H1, H2 and H3 are assumed to have a direct effect among the stated causal relationships shown in the conceptual framework in whereas H4 shows the mediation role of organizational innovation in the relationship between TQM and BFP. The details of the hypothesis and results found are presented in .

The first hypothesis tested in this study was ‘H1: Total Quality Management (TQM) significantly affects business financial performance’. The findings of the study show that TQM has a significant and positive effect on business financial performance (BFP) (β=.441, p <.001). This result proves that there is a statistically significant effect between TQM and financial performance. The Study by (Kebede Adem & Virdi, Citation2021; Alzeaideen, Citation2019) claimed that some of the TQM practices have no significant effect on performance. However, the findings of this study were consistent with those (Do et al., Citation2020; Nguyen et al., Citation2016; Liu et al., Citation2021; Suleiman Abu-Mahfouz, Citation2019) that supported the positive and significant effect of TQM on performance. Therefore, hypothesis (H1) was supported.

The second hypothesis was ‘H2: TQM has a significant effect on organizational innovative practice (OIP)’.

The results show that TQM has a significant positive effect on organizational innovation (β=.599, p <.001). These results agreed with the findings of (Nasim et al., Citation2020; Culture, Citation2019; Zandhessami & Jalili, Citation2013; Horng, 2017) which confirm the positive and significant effect of TQM on organizational innovation. Thus, hypothesis (H2) was supported.

The third hypothesis was ‘H3: Organizational innovation has a significant effect on business financial performance’. Organizational innovation was tested in several contexts toward firm performance since innovation creates different benefits for business organizations. Among these benefits, and one of the most important ones, was the improvement of firm performance (Anggadini et al., Citation2021; Chaudhry & Bilal, Citation2018). Furthermore, it was confirmed that firms that practice innovation can generate higher firm performance (Theresa, Citation2018).

The survey results of this study show that organizational innovation has a positive and significant effect on the coffee processing industry’s financial performance (β=.212, p <.001). This result was consistent with (Sotirelis & Grigoroudis, Citation2021; Andrade de Oliveira et al., Citation2020; Zafer Acar, Citation2020) which reported the significant role of organizational innovation in improving business performance. Accordingly, H3 was accepted.

The fourth hypothesis (H4) stated that ‘Organizational innovation mediates the relationship between TQM and business financial performance’. This study demonstrated that TQM and organizational innovation play a vital role in firms’ financial performance.

The results of this study reveal that organizational innovation mediates the relationship between TQM and business financial performance positively and significantly (β=.127, p <.001). This result agreed with the findings of (Aljuboori et al., Citation2021; Antunes et al., Citation2021; Toga, Citation2017). Similarly, the TQM practices (top management commitment, customer focus, continuous improvement, and communication and information analysis) and organizational innovation were sighted in this study and seen as the important factors that significantly affect financial performance. The empirical evidence at hand shows that the cumulative effect of TQM on the coffee processing industry through innovative practice was significant (β=.569, p <.001) and that TQM and organizational innovation together can affect the firm performance. Hence, H4 was supported.

In summary, this study found that organizational innovation practices play a mediation role between TQM and the financial performance of the coffee processing industry working in the Guji zone, Ethiopia where organizational innovation partially mediated the relationships. The considerations were based on the assumption of resource-based view (RBV) theory. The findings of this study were aligned with the RBV which focuses on internal resources performance improvement and capabilities through strategic management to maintain a competitive advantage and business long-term performance (View, Citation2022; Barney et al., Citation2001).

The findings, therefore, contribute to the existing literature on TQM and innovation by providing empirical evidence that shows the mediation role of innovation in the relationship between total quality management and business financial performance. Finally, to the knowledge of the authors, such study in the context of coffee processing particularly in the Guji zone, Ethiopia is the first and will help the future researchers as the source of literature evidence and empirical study.

5. Conclusions, implications and future research directions

5.1. Conclusion

The end goal of every business organization is to maximize profit and be competent in the business by securing performance. Performance is improved through the implementation of a holistic management approach called total quality management (TQM) as well as practising innovation. Therefore, this study assessed the role of organizational innovation practice (OIP) in the relationship between TQM and business financial performance; and found promising results that the application of TQM and innovation has a significant positive causal effect to improve business performance and long-term success without failing. After all, TQM has a fundamental role in improving the performance of the firm and the empirical evidence of this study shows that the implementation of TQM has a positive influence on the coffee quality and performance of the coffee processing industry operating in the Guji zone, Ethiopia.

The business financial performance of the coffee processing industry in Ethiopia, in particular in the Guji zone can be affected by TQM directly and indirectly. A survey result of this study demonstrated the TQM’s direct effect on the coffee processing industry’s financial performance. Similarly, the result shows that TQM has an indirect significant effect on business financial performance through organizational innovation. The cumulative effect of TQM on business financial performance shows a significant difference when organizational innovation is involved in the relationship. Therefore, organizational innovation mediates the relationship between TQM and business financial performance.

The relationship between TQM, organizational innovation and business financial performance were positive and statistically significant whereas organizational innovation plays a partial mediation in the relationship between TQM and business financial performance. Indeed, the hypotheses proposed were evaluated and all were accepted. Overall, the findings of this study were supported by literature evidence as presented in the discussions section. Finally, this study has contributed to filling the gaps among the existing literature, theory, and practice, and provided empirical evidence and practical recommendations to the coffee processing industry in Ethiopia.

5.2. Implications

The study has the following implications:

Theoretical Implications: This study gives support to the validation of the theories. The empirical evidence of the study supports and strengthens existing theories related to TQM and innovation, and their effect on business performance. The findings provide empirical support for the proposition that the implementation of TQM has a significant effect on improving the performance of the coffee processing industry. This validation contributes to the theoretical foundation of the relationship among TQM, innovation and performance.

Practical Implications:

The importance of TQM and innovation in the firm: The study highlights the significance of TQM and organizational innovation for achieving better business performance in the coffee processing industry. This insight has practical implications for the coffee processing industry and managers, emphasizing the need to prioritize and enhance TQM as a strategic focus. Practitioners can recognize the role of TQM and innovation and take action to foster a culture of quality within the firm.

To conclude, the study’s implications have contributed to theoretical, practical, and managerial perspectives. The findings help to validate the existing theories, provide practical insights for coffee processing firms, and offer guidance for managerial decision-making. TQM implementation has social implications that go beyond organizational boundaries. By implementing TQM practices organizations show a strong commitment to social responsibility and ethical practices, and firms can contribute to a more positive and sustainable society.

5.3. Limitations and suggestions for future researchers

This study acknowledges several limitations that future researchers should address. This study was cross-sectional research where the data was collected using a survey questionnaire from the primary source. The future researchers were directed to compile a longitudinal approach with secondary data. The study utilized a quantitative approach excluding the qualitative approach and hence, the next researchers were recommended to triangulate their findings with qualitative data to compare any variations in the results.

Moreover, the study covered only how the implementations of the TQM practices affect the financial performance of the coffee processing industry via organizational innovative practices whereas other performance indicators such as workforce and operational performances are not included. The authors recommended future researchers include those performance indicators.

Among many other TQM practices the study used only (top management commitment, customer focus, continuous improvement, and communication and information analysis) to check their relationship with business financial performance. Future researchers should consider other TQM practices based on the nature of their study. Similarly, only organizational innovation was seen as a mediator among other innovative practices. The index of mediation from the present study indicated that business financial performance received only 56.9% of the direct and indirect effect from TQM through organizational innovation, leaving 43.1% unaccounted for. From this, it can be presumed that the balance of 43.1% may be accounted for by other factors not considered in this study that necessitate further investigation. Therefore, future researchers should incorporate other TQM and innovation practices to strengthen the relationship with business financial performance.

Moreover, this study has assessed only the effect of TQM to business financial performance. However, there is literature that shows top management’s ethical leadership behaviour can affect organizational performance (Williams & Seaman, Citation2016). Therefore, this study recommended that future researchers examine how ethical leadership behaviour plays a role in the relationship between TQM and business performance.

Lastly, this study focuses on the coffee processing industry, which may raise concerns about generalizing the results to other sectors. To enhance the generalizability of research results, future studies should consider including a diverse range of industries, allowing for a broader understanding of the effect of TQM and innovation in different contexts.

Authors’ contributions

The manuscript was designed, analyzed and interpreted by Gemechu Hotessa Warie, a corresponding author. Dr. Admassu Tesso Huluka (PhD, Associate Professor) is a supervisor who critically revised the manuscript for intellectual integrity whereas; Dr. Elfneh Udessa Bariso (PhD, Associate Professor) is a supervisor and editor of the finally approved version of the manuscript intended for publication. All authors engaged in discussions regarding the results and made contributions to the final manuscript.

Acknowledgement

We, all authors collectively agreed to take responsibility for any errors in the results and findings.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data that support the findings of this study will be openly available upon request.

Additional information

Funding

Notes on contributors

Gemechu Hotessa Warie

Mr. Gemechu Hotessa Warie (Ph.D. candidate) is studying Ph.D in management at Bule Hora University, Ethiopia. He has achieved his BSc and MBA from Adama Science and Technology University and Leadstar University, Ethiopia respectively. He used to serve in different positions in several public and religious institutions and NGOs in Ethiopia.

Admassu Tesso Huluka

Admassu Tesso Huluka (PhD) is an associate professor at Ethiopian Civil Service University, specializing in development studies. He conducted postdoctoral research at the University of Boon, Germany. He has authored numerous articles in respected journals, serves on editorial boards, and focuses on development management, agriculture, project management, gender, poverty, and environmental studies.

Elfneh Udessa Bariso

Dr Elfneh Udessa Bariso is an interdisciplinary researcher at Bule Hora University, Ethiopia. He has a BA, MA, MSc, PhD in various subjects. He has published several research papers and book chapters. He is the editor-in-chief of the Bule Hora University Journal of Indigenous Knowledge and Development Studies (BHUJIKDS). Correspondence: [email protected]

References

- Ababa, A. (2020). Quality Management Practice And Performance Of Coffee Processing And Exporting Firms In Ethiopia SGS/0629/2011A (May).

- Addis, S. (2020). An exploration of quality management practices in the manufacturing industry of Ethiopia. The TQM Journal, 32(1), 1–19. https://doi.org/10.1108/TQM-01-2019-0031

- Agus, A., Krishnan, S. K., & Kadir, S. L. S. A. (2010). The structural impact of total quality management on financial performance relative to competitors through customer satisfaction : A study of Malaysian manufacturing companies. Total Quality Management, 11(4-6), 808–819. (September 2014), https://doi.org/10.1080/09544120050008255

- Ahaotu, S. M. (2019). Effective implementation of total quality management within the Nigerian construction industry [Ph. D.,]. Univeristy of Salford.

- Ahmad, M. F., Yin, J. C. S., Nor, N. H. M., Wei, C. S., Hassan, M. F., Hamid, N. A., & Ahmad, A. N. A. (2018 The relationship between TQM tools and organisation performance in small and medium enterprise (SMEs) [Paper presentation]. AIP Conference Proceedings, https://doi.org/10.1063/1.5055419

- Aigbavboa, C. O. (2019 Identifying barriers to total quality management implementation in the construction industry using the Delphi technique [Paper presentation]. (pp. 658–668). https://doi.org/10.33796/waberconference2019.46

- Alaoun, N. Y., & Faculty, B. (2018). The Effect of Total Quality Management Practices on Competitive Priorities of Telecommunication Companies in Qatar.

- Albuhisi, A. M., & Abdallah, A. B. (2018). The impact of soft TQM on financial performance. International Journal of Quality & Reliability Management, 35(7), 1360–1379. https://doi.org/10.1108/IJQRM-03-2017-0036

- Alharbi, K., & Al-Matari, E. M. (2016). The Impact of Total Quality Management (TQM) on organisational sustainability : The case of the hotel industry in Saudi Arabia : Empirical study. https://doi.org/10.3923/sscience.2016.3468.3473

- Alharbi, K., Al-Matari, E. M., & Yusoff, R. Z. (2016). The Impact of Total Quality Management (TQM) on organisational sustainability: The case of the hotel industry in Saudi Arabia: Empirical study. Social Sciences (Pakistan), 11(14), 3468–3473. https://doi.org/10.3923/sscience.2016.3468.3473

- Ali Raza, S., Hassan Naqvi, A., Ali Gill, S., & Professor, A. (2020). An investigation of the corporate TQM practices and corresponding results in Pakistani perspective. Implications for Business Education, 42(3), 51–77.

- Aljuboori, Z. M., Singh, H., Haddad, H., Al-Ramahi, N. M., & Ali, M. A. (2021). Intellectual capital and firm performance correlation: The mediation role of innovation capability in malaysian manufacturing SMEs perspective. Sustainability (Switzerland), 14(1), 154. https://doi.org/10.3390/su14010154

- Alzeaideen, K. (2019). The effect of total quality management on university performance in Jordan. International Journal of Financial Research, 10(6), 283–292. https://doi.org/10.5430/ijfr.v10n6p283

- Anastasiadou, S. D. (2015). The roadmaps of total quality management in the Greek education system according to Deming, Juran, and crosby in light of the EFQM Model. Procedia Economics and Finance, 33(15), 562–572. https://doi.org/10.1016/s2212-5671(15)01738-4

- Andrade de Oliveira, J. L., Franca, V., & De Araújo Barros, J. F. (2020). Relationship among quality management practices, innovation and competitive advantage in manufacturing companies certified with ISO 9001 in Brazil. International Journal for Innovation Education and Research, 8(7), 279–299. https://doi.org/10.31686/ijier.vol8.iss7.2476

- Anggadini, S. D., Surtikanti, S., Saepudin, A., & Saleh, D. S. (2021). Business performance and implementation of total quality management : A case study in Indonesia *. Journal of Asian Finance Economics and Business, 8(5), 1039–1046. https://doi.org/10.13106/jafeb.2021.vol8.no5.1039

- Antunes, M. G., Mucharreira, P. R., Justino, M. R. T., & Texeira-Quirós, J. (2021). Effects of total quality management (Tqm) dimensions on innovation—evidence from smes. Sustainability (Switzerland), 13(18), 10095. https://doi.org/10.3390/su131810095

- Antunes, M. G., Quirós, J. T., & Justino, M. d R. F. (2017). The relationship between innovation and total quality management and the innovation effects on organizational performance. International Journal of Quality & Reliability Management, 34(9), 1474–1492. https://doi.org/10.1108/IJQRM-02-2016-0025

- Awang, Z. (2014). Validating the Measurement Model : Cfa. Structural Equation Modelling Using Amos Grafic, 54–73.

- Azam, T., Songjiang, W., Jamil, K., Naseem, S., & Mohsin, M. (2023). Measuring green innovation through total quality management and corporate social responsibility within SMEs: green theory under the lens. The TQM Journal, 35(7), 1935–1959. https://doi.org/10.1108/TQM-05-2022-0160

- Bagga, S. K., & Haque, S. N. (2020). Total quality management as a change driver for influencing affective commitment to change: An empirical study in it organizations of Delhi-NCR region. Journal of Critical Reviews, 7(5), 971–980. https://doi.org/10.31838/jcr.07.05.198

- Baidoun, S. D., Salem, M. Z., & Omran, O. A. (2018). Assessment of TQM implementation level in Palestinian healthcare organizations: The case of Gaza Strip hospitals. The TQM Journal, 30(2), 98–115. https://doi.org/10.1108/TQM-03-2017-0034

- Barney, J., Wright, M., & Ketchen, D. J. (2001). The resource-based view of the firm: Ten years after 1991. Journal of Management, 27(6), 625–641. https://doi.org/10.1016/S0149-2063(01)00114-3

- Baron, R. M., & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research. conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Bazrkar, A., Aramoon, E., Hajimohammadi, M., & Aramoon, V. (2022). Improve organizational performance by implementing the dimensions of total quality management with respect to the mediating role oforganizational innovation capability. Studia Universitatis “Vasile Goldis” Arad – Economics Series, 32(4), 38–57. https://doi.org/10.2478/sues-2022-0018

- Birger, W. (1982). A resource based view of the firm. Strategic Management Journal, 5, 171–180.

- Chandrashekar, D., & Subrahmanya, M. H. B. (2019). E ® ect of innovation on firm performance. The Case of a Technology Intensive Manufacturing, 16(7), 1–31. https://doi.org/10.1142/S0219877019500524

- Chaudhry, N. I., & Bilal, A. (2018). Impact of TQM on organizational performance : The mediating role of business innovativeness and learning capability. Journal of Quality and Technology Management, 15(June), 01–36.

- Chauke, S. S., Edoun, E. I., & Mbohwa, C. (2019). The effectiveness of total quality management and operations performance at a bakery firm in the City of Tshwane, Pretoria South Africa [Paper presentation]. Proceedings of the International Conference on Industrial Engineering and Operations Management (pp. 2896–2907).

- Chen, R., Lee, Y. D., & Wang, C. H. (2020). Total quality management and sustainable competitive advantage: serial mediation of transformational leadership and executive ability. Total Quality Management & Business Excellence, 31(5-6), 451–468. https://doi.org/10.1080/14783363.2018.1476132

- Culture, O. (2019). Total Quality Management and Organizational Performance : A Possible Role of Total Quality Management and Organizational Performance : A Possible Role of Organizational Culture. https://doi.org/10.5430/ijba.v9n4p186

- Do, M. H., Huang, Y. F., & Do, T. N. (2020). The effect of total quality management-enabling factors on corporate social responsibility and business performance: evidence from Vietnamese coffee firms. Benchmarking: An International Journal, 28(4), 1296–1318. https://doi.org/10.1108/BIJ-09-2020-0469

- El-Daghar, K. (2018). Performance improvement plan in building process according to quality leaders and quality improvement tools and techniques. Architecture and Planning Journal, 24(1), 67–82. https://digitalcommons.bau.edu.lb/cgi/viewcontent.cgi?article=1020&context=apj

- Esiaba, L. A. (2016). Total Quality Management Practices and Competitive.

- Essel, R. E. (2020). Assessing Total Quality Management (TQM) effect on hospital performance in ghana using a non-probabilistic approach: The case of Greater Accra Regional Hospital (GARH). Metamorphosis: A Journal of Management Research, 19(1), 29–41. https://doi.org/10.1177/0972622520949091

- Ganapavarapu, L. K., & Prathigadapa, S. (2015). Study on total quality management for competitive advantage in international business. Arabian Journal of Business and Management Review, 5(3), 3–6.

- Gebregergs, A. (2019). Challenges of implementing quality management system in BGI-Ethiopia.

- Gezahegn Tegegne, B. (2020). Quality Management Practice and Performance of Coffee Processing and Exporting Firms in Ethiopia.

- Gómez, J. G., Martínez Costa, M., & Martínez Lorente, Á. R. (2017). EFQM Excellence Model and TQM: an empirical comparison. Total Quality Management & Business Excellence, 28(1-2), 88–103. https://doi.org/10.1080/14783363.2015.1050167

- Hafiz, B., Abdul, J., & Shaari, N. (2013). Confirmatory Factor Analysis (CFA) of first order factor measurement model-ICT empowerment in Nigeria. 2(May), 81–88.

- Hamdan, Y., & Alheet, A. F. (2021). Toward sustainability: The role of tqm and corporate green performance in the manufacturing sector. International Journal of Entrepreneurship, 25(3), 1–15.

- Herzallah, A. M., Gutiérrez-Gutiérrez, L., & Munoz Rosas, J. F. (2014). Total quality management practices, competitive strategies and financial performance: The case of the Palestinian industrial SMEs. Total Quality Management & Business Excellence, 25(5-6), 635–649. https://doi.org/10.1080/14783363.2013.824714

- Howard, S. (2018). Coffee and the state in rural Ethiopia. 18(1), 1–22.

- Hundie, S. K., & Biratu, B. (2022). Response of Ethiopian coffee price to the world coffee price: Evidence from dynamic ARDL simulations and nonlinear ARDL cointegration. Cogent Economics & Finance, 10(1), 2114168. https://doi.org/10.1080/23322039.2022.2114168

- Ilyas, S., Hu, Z., & Wiwattanakornwong, K. (2020). Unleashing the role of top management and government support in green supply chain management and sustainable development goals. Environmental Science and Pollution Research International, 27(8), 8210–8223. https://doi.org/10.1007/s11356-019-07268-3

- Jalata, D. H. (2021). Competitiveness and determinants of coffee export in Ethiopia : An analysis of revealed comparative advantage and autoregressive distributed lag model. Journal of Economics and Sustainable Development, 12(5), 43–62. https://doi.org/10.7176/JESD/12-5-0

- Jimoh, R., Oyewobi, L., Isa, R., & Waziri, I. (2019). Total quality management practices and organizational performance: the mediating roles of strategies for continuous improvement. International Journal of Construction Management, 19(2), 162–177. https://doi.org/10.1080/15623599.2017.1411456

- Kalay, F. (2015). The impact of strategic innovation management practices on firm innovation performance. Pressacademia, 2(3), 412–412. https://doi.org/10.17261/Pressacademia.2015312989

- Karyamsetty, H. J. (2021). Organizational sustainability and TQM in SMEs : A proposed model. European Journal of Business and Management, 13(4), 88–97. https://doi.org/10.7176/EJBM/13-4-09

- Kebede Adem, M., & Virdi, S. S. (2021). The effect of TQM practices on operational performance: an empirical analysis of ISO 9001: 2008 certified manufacturing organizations in Ethiopia. The TQM Journal, 33(2), 407–440. https://doi.org/10.1108/TQM-03-2019-0076

- Keinan, A. S., & Karugu, J. (2018). Total quality management practices and performance of manufacturing firms in Kenya : Case of Bamburi cement limited. International Academic Journal of Human Resource and Business Administration, 3(1), 81–99.

- Khalfallah, M., Ben Salem, A., Zorgati, H., & Lakhal, L. (2021). Innovation mediating relationship between TQM and performance: cases of industrial certified companies. The TQM Journal, 34(3), 552–575. https://doi.org/10.1108/TQM-01-2021-0019

- Kim, D. Y. (2016). The Impact of Quality Management Practices on Innovation [Ph. D.,] Sprott School of Business.

- Kor, Y. Y., & Mahoney, J. T. (2000). Penrose’s resource-based approach: The process and product of research creativity. Journal of Management Studies, 37(1) https://doi.org/10.1111/1467-6486.00174

- Kozlenkova, I. V., Samaha, S., & Palmatier, R. (2014). Resource-Based Theory in Marketing Resource-based theory in marketing. Journal of the Academy of Marketing Science, 42(1), 1–21. https://doi.org/10.1007/s11747-013-0336-7

- Lassala, C., Apetrei, A., & Sapena, J. (2017). Sustainability matter and financial performance of companies. Sustainability (Switzerland), 9(9), 1498. https://doi.org/10.3390/su9091498

- Lian, Z., Liu, Q., Guo, Y., & Innovation, T. (2020). Analysis and measure of process coupling between TQM and technological innovation. 107–115. https://doi.org/10.23977/ferm.2020.030116

- Liu, H. et al. (2021). ‘An empirical exploration of quality management practices and firm performance from Chinese manufacturing industry’. Total Quality Management and Business Excellence, 32(15–16), 1694–1712. https://doi.org/10.1080/14783363.20201769474.

- Lockett, A., Thompson, S., & Morgenstern, U. (2009). The development of the resource-based view of the firm: A critical appraisal. International Journal of Management Reviews, 11(1), 9–28. https://doi.org/10.1111/j.1468-2370.2008.00252.x

- Menza, G. K., & Rugami, J. M. (2021). Total quality management practices and performance of deposit taking savings and credit cooperatives in Mombasa County, Kenya. International Journal of Business Management, Entrepreneurship and Innovation, 3(1), 65–77. https://doi.org/10.35942/jbmed.v3i1.165

- Muhammad Zakki. (2021). Total quality management: a study of processing the quality of 99 brand coffee product. Journal of Islamic Economics Perspectives 3(1), 32–44. https://doi.org/10.35719/jiep.v3i1.37

- Najm, N., Yousif, A. S., & Al-Ensour, J. (2017). Total quality management (TQM), organizational characteristics and competitive advantage. Journal of Economic & Financial Studies, 5(04), 12–23. https://doi.org/10.18533/jefs.v5i04.293

- Nasim, K., Sikander, A., & Tian, X. (2020). Twenty years of research on total quality management in Higher Education: A systematic literature review. Higher Education Quarterly, 74(1), 75–97. https://doi.org/10.1111/hequ.12227

- Nazar, N., Ramzani, S. R., Anjum, T., & Shahzad, I. A. (2018). Organizational performance: The role of TQM practices in banking sector of Pakistan. European Scientific Journal, ESJ, 14(31), 278. https://doi.org/10.19044/esj.2018.v14n31p278

- Nguyen, A. D., Pham, C. H., & Pham, L. (2016). Total quality management and financial performance of construction companies in Ha Noi. International Journal of Financial Research, 7(3), 41–53. https://doi.org/10.5430/ijfr.v7n3p41

- Nyaribo, J. S. (2022). Influence of total quality management on competitive advantage of tea processing companies in Kenya. International Academic Journal of Human Resource and Business Administration, 4(1), 430–447.

- Nyeadi, J. D., Kamasa, K., & Kpinpuo, S. (2021). Female in top management and firm performance nexus: Empirical evidence from Ghana. Cogent Economics & Finance, 9(1), 1921323. https://doi.org/10.1080/23322039.2021.1921323

- Ooi, K. (2009). TQM and knowledge management: Literature review and proposed framework. African Journal of Business Management, 3(11), 633–643. https://doi.org/10.5897/AJBM09.196

- Othman, B. (2020). The influence of total quality management on competitive advantage towards bank organizations: Evidence from Erbil/Iraq. International Journal of Psychosocial Rehabilitation, 24(5), 3427–3439. https://doi.org/10.37200/IJPR/V24I5/PR202053

- Pengaruh, P. M. A., Pmdn., & Tk, d I. (2020). Quality management practices and challenges in Ethiopian telecommunication. 2507(February), 1–9.

- Phakiti, A., De Costa, P., Plonsky, L., & Starfield, S. (2018). The palgrave handbook of applied linguistics research methodology. In The Palgrave Handbook of Applied Linguistics Research Methodology. Springer. https://doi.org/10.1057/978-1-137-59900-1

- Psomas, E. L., & Jaca, C. (2016). The impact of total quality management on service company performance: evidence from Spain. International Journal of Quality and Reliability Management, 33(3), 380–398. https://doi.org/10.1108/IJQRM-07-2014-0090

- Puthanveettil, B. A., Vijayan, S., Raj, A., & Mp, S. (2021). TQM implementation practices and performance outcome of Indian hospitals: exploratory findings. The TQM Journal, 33(6), 1325–1346. https://doi.org/10.1108/TQM-07-2020-0171

- Saad, Z. A., Banking, I., Banking, I., Sharofiddin, A., Banking, I., March, R., & May, A. (2020). Effect of applying total quality management in improving the performance of Al-Waqf of Albr societies in Saudi Arabia : A theoretical framework for " Deming ‘ s model. International Journal of Business Ethics and Governance, 3(2), 12–32. https://doi.org/10.51325/ijbeg.v3i2.24

- Saud, T. R. (2019). Total quality management system and organisation performance: mediating effect of organisational learning in Nepali service sector. Journal of Business and Social Sciences Research, 4(1), 39–60. https://doi.org/10.3126/jbssr.v4i1.28997

- Sciarelli, M., Gheith, M. H., & Tani, M. (2020). The relationship between soft and hard quality management practices, innovation and organizational performance in higher education. The TQM Journal, 32(6), 1349–1372. https://doi.org/10.1108/TQM-01-2020-0014

- Shafiq, M., Lasrado, F., & Hafeez, K. (2019). The effect of TQM on organisational performance: empirical evidence from the textile sector of a developing country using SEM. Total Quality Management & Business Excellence, 30(1-2), 31–52. https://doi.org/10.1080/14783363.2017.1283211

- Singh, V., Kumar, A., & Singh, T. (2018). Impact of T QM on organisational performance: The case of Indian manufacturing and service industry. Operations Research Perspectives, 5, 199–217. https://doi.org/10.1016/j.orp.2018.07.004

- Sotirelis, P., & Grigoroudis, E. (2021). Total Quality Management and Innovation: Linkages and Evidence from the Agro-food Industry. Journal of the Knowledge Economy, 12(4), 1553–1573. https://doi.org/10.1007/s13132-020-00683-9

- Suleiman Abu-Mahfouz, S. (2019). TQM Practices and Organizational Performance in the Manufacturing Sector in Jordan mediating role of HRM Practices and Innovation. NO 22 Journal of Management and Operation Research, 1(22), 1.

- Theresa, W. (2018). The Relationship Between Innovation And Total Quality Management And The Innovation Effects On Organizational Performance. The Eletronic Library, 34(1), 1–5.

- Toga, M. (2017). The relationship between total quality management and innovation in the South African foundry/steel industry Mainford Toga. University of the Witwatersrand.

- Ukab, M. M. (2021). Total quality management practices to enhance organizational performance by competitive advantage as mediating in SMES in Iraq. Psychology and Education Journal, 58(2), 5471–5481. https://doi.org/10.17762/pae.v58i2.2961

- USDA. (2020). Coffee Annual - Ethiopia. Et2020-0004.

- View, K. (2022). Resource-Based Theory.

- Wagimin, K. E., Ali, J., & Helia, V. N. Asia e University, Sultan Sulaiman Street, Kampung Attap, Kuala Lumpur, MALAYSIA. (2019). The effect of leadership on employee performance with Total Quality Management (TQM) as a mediating variable in Indonesian petroleum companies: A case study. International Journal of Integrated Engineering, 11(5), 180–188. https://doi.org/10.30880/ijie.2019.11.05.023

- Williams, J. J., & Seaman, A. E. (2016). The influence of ethical leadership on managerial performance: Mediating effects of mindfulness and corporate social responsibility. Journal of Applied Business Research (JABR), 32(3), 815–828. https://doi.org/10.19030/jabr.v32i3.9659

- Wongsansukcharoen, J., & Thaweepaiboonwong, J. (2023). Effect of innovations in human resource practices, innovation capabilities, and competitive advantage on small and medium enterprises’ performance in Thailand. European Research on Management and Business Economics, 29(1), 100210. https://doi.org/10.1016/j.iedeen.2022.100210

- Worlu, R., & Obi, J. (2019). Total quality management practices and organizational performance. Covenant Journal of Business and Social Sciences, 10(1), 4–11.

- Yas, H., Alsaud, A. B., Almaghrabi, H. A., Almaghrabi, A. A., & Othman, B. (2021). The effects of TQM practices on performance of organizations: A case of selected manufacturing industries in Saudi Arabia. Management Science Letters, 11, 503–510. https://doi.org/10.5267/j.msl.2020.9.017

- Yusliza, M. Y., Norazmi, N. A., Jabbour, C. J. C., Fernando, Y., Fawehinmi, O., & Seles, B. M. R. P. (2019). Top management commitment, corporate social responsibility and green human resource management: A Malaysian study. Benchmarking: An International Journal, 26(6), 2051–2078. https://doi.org/10.1108/BIJ-09-2018-0283

- Yusufu, S. O. (2018). Effect of Total Quality Management on Organizational Performance Of West African Ceramic Company.

- Zafer Acar, A. (2020). The mediating role of value innovation between market orientation and business performance: Evidence from the logistics industry. International Journal of Business Innovation and Research, 21(4), 540–563. https://doi.org/10.1504/IJBIR.2020.106012

- Zakuan, N. M., Yusof, S. M., Laosirihongthong, T., Tun, U., Onn, H., Raja, P., & Pahat, B. (2010). Proposed relationship of TQM and organisational performance. Total Quality Management & Business Excellence, 21(2), 185–203. https://doi.org/10.1080/14783360903550020

- Zandhessami, H., & Jalili, A. (2013). The Impact of Total Quality Management on Organizational Innovation. International Journal of Research in Industrial Engineering Journal Homepage, 2(1), 1–11. www.nvlscience.com/index.php/ijrie

- Zou, Y., & Fan, P. (2022). How top management commitment on diversity leads to organizational innovation: The evidence from China. Journal of Human Resource and Sustainability Studies, 10(02), 246–261. https://doi.org/10.4236/jhrss.2022.102016